What Is Xtreme HD IPTV and Is It Worth Your Time? A Real Look at the Service

Networking |

2026-06-27 06:55:09

As the bio-based chemicals agenda shifts from laboratory curiosity to commercial reality, 5-hydroxymethylfurfural (5-HMF, CAS 67-47-0) is emerging as a small-but-strategically-important node in multiple value chains — from specialty flavors and fragrances to pharmaceutical intermediates and platform chemicals. PW Consulting’s forthcoming full market study (base year 2025; historical coverage 2020–2025; forecast horizon 2026–2032) quantifies that transition and translates it into actionable strategic guidance. Our analysis shows the global 5-HMF market advancing from approximately USD 50.0 Million in 2020 to USD 61.6 Million in 2025, with a projected rise to roughly USD 80.0 Million by 2032 under a compound annual growth rate (CAGR) of 3.8% across the 2026–2032 forecast window.

5-hydroxymethylfurfural (5-HMF) (CAS 67-47-0) Market

Timing investment and capacity decisions: With steady but moderate growth projected, the market rewards targeted, quality-driven capacity expansions and strategic partnerships rather than broad-brush greenfield builds. The report equips leaders with the scenario sensitivities they need to justify near-term capital deployment or deferment.

5-hydroxymethylfurfural (5-HMF) (CAS 67-47-0) Market

Managing feedstock and supplier risk: Our supply-chain mapping highlights concentration points and practical hedges to insulate upstream sugar/glucose feedstock exposure — essential given the Q4 2025 price stabilization observed in the HMF spot market due to balanced glucose supply and moderate food demand.

5-hydroxymethylfurfural (5-HMF) (CAS 67-47-0) Market

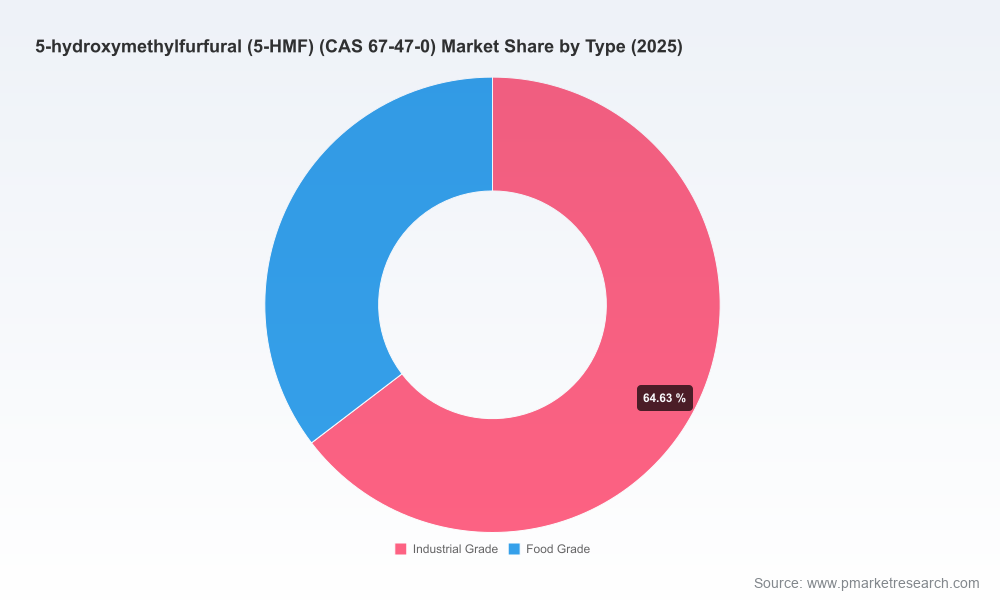

Commercial segmentation and margin optimization: We translate market growth into prioritized application routes (chemical intermediates, flavors & fragrances, pharmaceuticals, and others) and identify where premium quality and certifications unlock outsized margins.

Regulatory & trade monitoring for near-term moves: The product is not singled out in the reciprocal tariffs listed by U.S. Customs and Border Protection through late 2025 — a window of relative regulatory predictability that firms can leverage for cross-border sourcing and inventory planning.

Robust market sizing and growth model — base year 2025 with a detailed historical reconstruction (2020–2025) and transparent forecast mechanics (2026–2032) that you can stress-test with your own assumptions.

Supply-chain and raw-material intelligence — mapping of feedstock origin, conversion technologies, cost buckets, and interruption risk. Includes a buyer-supplier heatmap and procurement playbook for midstream buyers.

Competitive profiling and capability benchmarking — in-depth company dossiers with technology assessments, capacity signals, margin proxies, and strategic options (licensing, JV, tolling, vertical integration).

Commercial segmentation framework — demand drivers, differential pricing dynamics by product grade (industrial, food/food-adjacent, research/pharma), and go-to-market archetypes for premium vs. volume plays.

Regulatory & standards tracker — compliance matrices, likely certification roadmaps (food, pharma, Halal/Kosher where relevant), and customs/tariff intelligence linked to trade corridors.

Practical decision tools — investment case templates, M&A screening filters, due-diligence checklists, 18–24 month procurement action plans, and scenario-based cash-flow sensitivities.

Price and margin dashboard — historical price behavior, key value-driver elasticities, and short-term price scenario outputs for 2026 planning.

The 5-HMF competitive environment is characterized by a small number of specialist producers and a broader set of regional suppliers that together shape availability, quality segmentation, and pricing dynamics. The market displays material concentration among established specialists while leaving tactical space for new technology entrants and contract manufacturers.

AVA Biochem AG (Muttenz, Switzerland) — A technology-led, bio-based producer differentiating on renewable feedstocks and hydrothermal proprietary processes. Companies with this asset profile are best positioned to capture sustainability-driven premium demand, particularly where traceability and low-carbon credentials are required. Their scale-approach to high-purity 5-HMF (technical and research grades) makes them a strategic partner for downstream formulators seeking consistent, certified inputs.

Robinson Brothers Limited (UK) — Specialty fine-chemical supplier with strengths in custom synthesis for flavor & fragrance and pharmaceutical niches. Suppliers offering tailored synthesis and high-purity grades provide flexible, application-driven value propositions — especially valuable where product specifications are bespoke and time-to-market matters.

Penta Manufacturing Company (USA) — A North American manufacturer serving industrial and specialty chemical markets. Regional manufacturing capability is an advantage for customers minimizing logistics and tariff exposure; domestic producers also provide faster iterative development with industrial users.

Sigma-Aldrich / Merck KGaA (St. Louis HQ for distribution) — Research-grade supply with robust quality assurances and certifications (including Halal/Kosher where applicable). Established lab-supply channels often seed downstream R&D cycles, converting early technical adoption into later commercial demand.

Chinese producers (e.g., Beijing Lys Chemicals, Shanghai Starsky) — Cost-competitive bulk suppliers and exporters. These companies are important tactical sources for volume buyers and play a central role in global availability, though buyers must reconcile quality control, lead times, and certification demands for high-value end uses.

Specialty/reserach suppliers (AstaTech, Toronto Research Chemicals) — Niche suppliers that facilitate R&D and small-batch specialized applications, often acting as innovation conduits into pharma and advanced-materials pathways.

Market concentration is meaningful: top-tier specialists capture a significant share of available commercial demand, creating a dynamics where scale, process robustness, and certification capability materially influence supplier selection and pricing power.

Feedstock balance and alternative sugar sources — even modest volatility in glucose/sugar markets can compress margins for non-integrated producers; our models identify breakpoints where tolling or vertical integration materially improves returns.

Certification and quality premium adoption — demand segments that require food-grade or pharmaceutical-grade 5-HMF will continue to deliver higher margins, but also require investments in QA/QC, documentation, and third-party certification.

Regulatory stability — at present (late 2025), 5-HMF is not specifically targeted in reciprocal tariff lists, enabling a strategic window to optimize cross-border procurement and inventory placement. Future regulatory changes (e.g., new food safety guidance or trade measures) would be a primary downside risk in our scenarios.

Technology disruption events — breakthroughs in catalytic routes, yield improvements, or low-cost bio-refinery integration could materially change competitive economics; conversely, technical scale-up failures would favor established players with proven processes.

Buyers (formulators, pharma intermediates): secure dual-sourcing contracts with clear acceptance criteria, lock in short-term volumes where certificate-backed suppliers are available, and pilot qualifying programs with bio-based producers to support sustainability claims.

Producers: prioritize yield and impurity profile improvements, invest in certifications that unlock high-value end markets, and evaluate tolling/joint-venture structures to accelerate capacity without committing full capex.

Investors and M&A teams: use PW Consulting’s M&A screening toolkit to identify targets that close capability gaps (feedstock access, downstream offtake, IP in conversion technology), and model outcomes under the report’s base, upside, and downside scenarios.

Policy & trade teams: maintain active monitoring of tariff and regulatory announcements; a short window of predictability exists through late 2025 but proactive engagement with customs advisors will reduce exposure to sudden trade policy shifts.

This preview highlights why 2026 is a decisive planning year: the 5-HMF market is maturing into a place where selective investments, supplier specialization, and certification-based differentiation create clear winners. PW Consulting’s full report contains the granular segment tables, supplier scorecards, and Excel-based model that corporate strategists and commercial teams will need to finalize budgets, procurement commitments, and M&A screens.

To transform this strategic preview into executable plans, PW Consulting recommends immediate access to the full dossier (market-level and segment-level forecasts, supplier dossiers, and decision tools). Our team stands ready to run tailored workshops that apply the report’s scenarios to your asset base and commercial roadmap.

Contact PW Consulting for subscription access, custom briefings, and proprietary modeling support — and use the next 90 days of regulatory and feedstock predictability to convert insight into competitive positioning.

For detailed analysis of this topic, please visit the official page:5-hydroxymethylfurfural (5-HMF) (CAS 67-47-0) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com