CVD Silicon Carbide Market — Strategic Briefing for 2026 Decisions

PW Consulting today publishes a strategic briefing drawn from our forthcoming CVD Silicon Carbide Market research report (base year 2025, forecast 2026–2032). As supply chains and capital allocation decisions crystallize for 2026, this briefing highlights the report’s near-term relevance and the practical levers management teams should consider. The global CVD Silicon Carbide market shows sustained expansion: our model traces a rise from USD 180.5 Million in 2020 to USD 246.8 Million in 2025, with a projected acceleration to USD 263.28 Million in 2026 and a long‑term outlook to USD 432.0 Million by 2032 at a compound annual growth rate (CAGR) of 8.45% (USD, revenue units: Million). These macro dynamics create distinct strategic inflection points for OEMs, component manufacturers, materials suppliers and investors entering 2026.

CVD Silicon Carbide Market

What the report delivers — practical, decision-ready intelligence

- Actionable market sizing and forecasting calibrated to 2025 (base year) and stress‑tested across 2026–2032 scenarios, including upside/downside demand curves and sensitivity to key inputs.

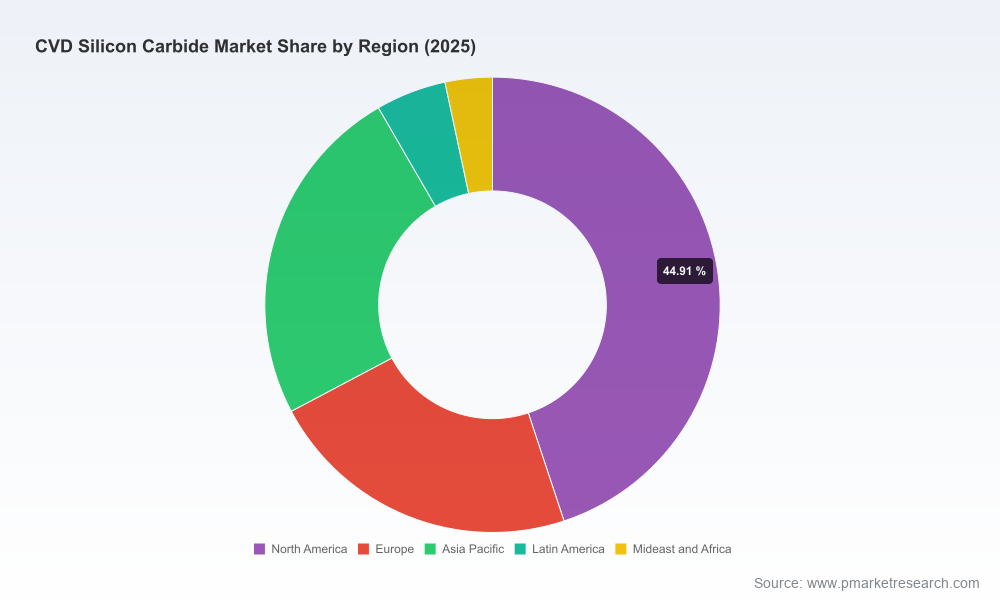

- End‑use and technology pathways mapping that link CVD SiC product families to OEM purchasing cycles and factory tool roadmaps (we purposely withhold detailed segment tables in this briefing to preserve the report’s proprietary value).

- Supply‑chain diagnostic with supplier tiering, feedstock exposure analysis, transporter and logistics risk scoring, and recommended mitigation tactics such as dual sourcing and strategic inventory buffering.

- Regulatory and environmental risk matrix covering chemical processing compliance, emissions controls, and how tightening standards translate into effective cost inflation for producers and buyers.

- Competitive benchmarking and capability heat maps for leading suppliers, plus a curated set of M&A and partnership targets screened by technical fit, scale, and regional footprint.

- Commercial playbooks: price negotiation templates, long‑term supply contracting clauses, product qualification roadmaps, and CapEx/Opex modelling tools tailored for producers and end users.

Why this matters for 2026 — three strategic imperatives

The macro trajectory — steady growth to 2026 and beyond — reframes choices that executives must make now. From our scenario analyses, three imperatives stand out for 2026 planning cycles.

CVD Silicon Carbide Market

- Secure feedstock and manage margin pressure: Upstream dynamics are becoming a determinative factor. A measured rise in silicon tetrachloride pricing and episodic regional shortages have already compressed manufacturers’ margins. Procurement teams should adopt layered defenses (longer lead agreements, indexed pricing floors, and regional diversification). The report includes cost-to-price translation models that quantify margin sensitivity to feedstock moves and regulatory compliance cost pass‑through.

- Align capacity expansion with differentiated technology bets: Given mid-single digit to low‑double digit growth rates captured in our forecasts, capital investments must be selective. 2026 is a year for modular expansion and partnerships rather than large greenfield commitments unless a supplier can demonstrate structurally advantaged feedstock, regulatory clearance, or exclusive OEM relationships. The report’s scenario maps help decision-makers decide where to allocate incremental capital to maximize IRR while minimizing stranded‑asset risk.

- Prioritize product and process resilience over short‑term share gains: Process robustness (particle control, plasma endurance, thermal stability) is increasingly the gating criterion for sub‑5 nm and advanced process nodes. Buyers will pay premiums for demonstrable durability and low contamination risk; suppliers without these credentials face accelerated commoditization. Our competitor dossiers and technical scorecards identify leading capabilities and the gaps newer entrants must close to compete effectively.

Supply‑chain signals to act upon in 2026

Trending input cost and regulatory pressures are not hypothetical: industry monitoring shows notable movement in Q1 2026. A price‑index uptick for silicon tetrachloride in that quarter flagged constrained availability and higher energy costs across producing regions. Electronic‑grade feedstock pricing observed in early 2025 also points to persistent regional spreads, with Asian suppliers offering materially different cost bases versus North American alternatives. In practice, these dynamics produce three immediate actions we recommend for 2026:

CVD Silicon Carbide Market

- Institute quarterly feedstock reviews with immediate escalation thresholds tied to procurement KPIs.

- Pursue blended sourcing strategies — short, medium and long‑term contracts — to smooth price volatility and preserve negotiating leverage.

- Quantify regulatory pass‑throughs and embed them in customer contracts and internal forecasting so product pricing and profit planning remain aligned.

Competitive landscape — who matters and why

The CVD SiC landscape is concentrated and characterized by technically sophisticated suppliers that combine materials science, high‑precision machining and semiconductor equipment know‑how. Our market concentration analysis indicates that a small group of firms controls a meaningful share of the market, underscoring both entry barriers and consolidation opportunity.

- CoorsTek (Golden, Colorado, USA) — Known for PureSiC® CVD SiC products, CoorsTek competes on ultra‑high purity and tailored coatings for semiconductor processing. Their strength is an end‑to‑end manufacturing mindset and customer qualification experience for wafer carriers and high‑temperature components.

- Morgan Advanced Materials (Woking, UK) — Offers Performance SiC grades with emphasis on chemical and erosion resistance, low coefficient of thermal expansion and thermal shock performance. They are a strategic choice where process stability and longevity reduce total cost of ownership for fabs.

- Ferrotec (Tokyo, Japan; US operations) — Markets ADMAP SiC with an emphasis on ultra‑high purity and wear/corrosion resistance. Ferrotec’s cross‑border footprint makes them a supplier of choice for multi‑national fabs seeking consistent global specifications.

- Tokai Carbon (Tokyo, Japan) — A leading global supplier of solid CVD SiC, with recent product innovations focused on low‑particle focus rings and plasma‑resistant shields engineered for extreme endurance. Their strategic partnership activity, such as co‑development with wafer substrate players, signals a move to capture more value upstream and into wafer supply chains.

- PremaTech Advanced Ceramics (Worcester, Massachusetts, USA) — Focused on OMNI SiC™ product lines and recent capacity expansion in the U.S. prepositions them for North American demand growth. Their machining and finishing capabilities reduce integration cost for customers.

Recent developments — facility expansions, product innovations and strategic partnerships — show incumbents are protecting OEM relationships and extending technical moats. For buyers and investors, the competitive implication is clear: partnering or consolidating with established, qualified suppliers will often outperform attempting to vertically integrate from scratch unless the company can justify scale economics or proprietary feedstock access.

Regulatory and cost risks — how they will shape deals and sourcing

Regulatory tightening on chemical processing and emissions has increased complexity for both suppliers and buyers. Higher local compliance costs — particularly in developed markets with stringent standards — create a divergence in effective production economics. The consequence is threefold: localized cost inflation, incentive for regional supply concentration where regulatory regimes are more permissive, and a rising value for compliance‑savvy partners. The report contains a regulatory exposure matrix that ranks production locations and proposes mitigation pathways including investment in abatement, certification roadmaps, and insurer‑friendly environmental disclosures.

How executives should use this briefing (and the full report) in 2026 planning

- Use the report’s forecasting scenarios to stress‑test capital plans and to set contractual flexibility and renewal cadences for 2026 purchase orders.

- Embed supplier scoring and feedstock sensitivity outputs into procurement RFPs — the report provides templates and red‑flag thresholds that shorten negotiation cycles.

- Accelerate partnerships with qualified suppliers for co‑development or tolling arrangements to de‑risk product qualification timelines for aggressive fab ramp schedules.

- Consider selective M&A or minority investments to secure strategic capabilities (e.g., low‑particle processing, plasma endurance solutions) rather than funding organic development when time‑to‑market is a gating factor.

Delivering measurable outcomes — what PW Consulting clients receive

Clients who commission the full report receive quantitative assets and operational templates designed for immediate use in boardroom and procurement cycles: a proprietary financial model for cash‑flow and CapEx planning; supplier and plant‑level risk heat maps; a prioritized M&A target list with integration risk scoring; regulatory compliance playbooks; and commercial negotiation attachments for long‑term supply agreements. These tools convert the high‑level market trajectory and supplier intelligence into executable 90‑, 180‑ and 360‑day plans.

In a market expanding through 2026 and into the next decade, decisions taken this year about supplier commitments, capacity posture and technology partnerships will disproportionately determine competitive positioning. The PW Consulting CVD Silicon Carbide Market report pairs rigorous forecasting (base year 2025, 2026–2032 outlook at 8.45% CAGR) with hands‑on commercial tools to convert insights into outcomes.

Next steps

For executives evaluating capital allocation, supply contracts or M&A in 2026, the full PW Consulting report provides the granular segment analyses, plant‑level capacity maps and supplier economics that are intentionally excluded from this public briefing. To review the complete dataset, competitor scorecards, and scenario models, visit the PW Consulting report page or contact our industry practice to schedule a briefing and model walk‑through.

For detailed analysis of this topic, please visit the official page:CVD Silicon Carbide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com