Europe Microfluidics Market Overview: Key Drivers and Challenges 2025 –2032

Health |

2026-06-25 08:52:23

PW Consulting’s latest market report on Asphalt Mixing Plants provides a strategic compass for companies making high-stakes capital, product and market-entry decisions in 2026. Building on a rigorous historical base (2020–2025) and a forward-looking forecast horizon (2026–2032), the study projects a steady expansion of the global market—from an assessed base in 2025 to a projected market trajectory that reflects a compound annual growth rate (CAGR) of 3.4% through the forecast period. With market dynamics shaped by sustainability mandates, feedstock volatility and modularization of production, this briefing highlights the practical implications executives must weigh before committing resources this year.

Asphalt Mixing Plants Market

Clarity on momentum: The market shows resilient growth following post‑pandemic recovery, with the 2025 market serving as the analytical pivot for scenario planning in 2026. PW Consulting’s top-line projections equip leaders with reliable macro baselines for budgeting and capital allocation.

Asphalt Mixing Plants Market

Regulation-led product roadmaps: Tightening air-quality standards and state permitting practices are accelerating demand for low-emission, high-recycling solutions. Manufacturers and plant operators need to prioritize compliance-ready technologies when specifying new assets.

Asphalt Mixing Plants Market

Operational resilience under input-price stress: Raw material and commodity price volatility necessitate flexible procurement strategies and design choices that reduce exposure to single-source inputs.

Historical continuity and trajectory: The study uses 2020–2025 as the historical window, enabling trend decomposition across demand cycles, technology adoption and policy inflection points.

Base and forecast framing: The report’s base-year is 2025 and it models market outcomes over 2026–2032, applying a 3.4% CAGR across the forecast interval. These aggregated figures are calibrated to observable macrodrivers—infrastructure spend patterns, regulatory tightening and equipment lifecycle replacement rates.

Market structure: Competitive intensity is moderate; top-tier supplier concentration (CR3 and CR5) suggests a fragmented market with room for regional champions and niche technology leaders. This structure creates differentiated routes to scale—strategic M&A, partnership-led distribution and technology licensing are all viable plays.

Decarbonization and recycling: There is an accelerating shift toward high-RAP (reclaimed asphalt pavement) integration and alternative-fuel capability. The early adopters of 100% RAP-capable processing and hydrogen-capable burners have moved from demonstration to commercial showcases at major trade expos, making these technologies procurement priorities for forward-looking operators.

Regulatory compliance as a product differentiator: Federal and state permitting frameworks are more prescriptive on particulate and opacity controls. For example, recent references to particulate limits and opacity standards are forcing plant owners to consider advanced emission-control modules as baseline equipment, not optional extras.

Modularity and mobility: Demand is bifurcating between large stationary installations and mobile/modular plants that support fast-turn regional projects. Suppliers that offer a portfolio spanning mobile, modular and stationary platforms are better positioned to capture lifecycle spend from construction contractors through to municipal operators.

Input-cost pressure and margin management: Binder and steel prices have moved materially on market signals, prompting buyers to stress-test total cost of ownership models across equipment life cycles. Procurement teams should incorporate sensitivity runs for raw-material price swings into capital approvals.

The competitive review in the report synthesizes company-level strategy, product road maps and trade-show disclosures to judge who is likely to lead adoption of next‑generation plant technologies.

Ammann Group — A leader in integrated plant solutions, Ammann has showcased systems capable of very high RAP integration and alternative-fuel support, including hydrogen. Their recent product unveilings signal a deliberate push to own the sustainability narrative in plant design, placing them in contention for large public and private projects that attach emission targets to contracts.

ASTEC Industries — With a portfolio that spans portable to stationary systems and notable moves toward hydrogen-capable burners, ASTEC’s emphasis is on retrofitability and field-ready adaptability. Their product highlights suggest a focus on operators that require rapid deployment without compromising on modified asphalt capabilities.

Benninghoven (Wirtgen Group) — Positioning around flexibility and economy, Benninghoven’s CORE-system messaging centers on balancing throughput with environmental performance—an attractive combination for contractors operating under tight margins and permit constraints.

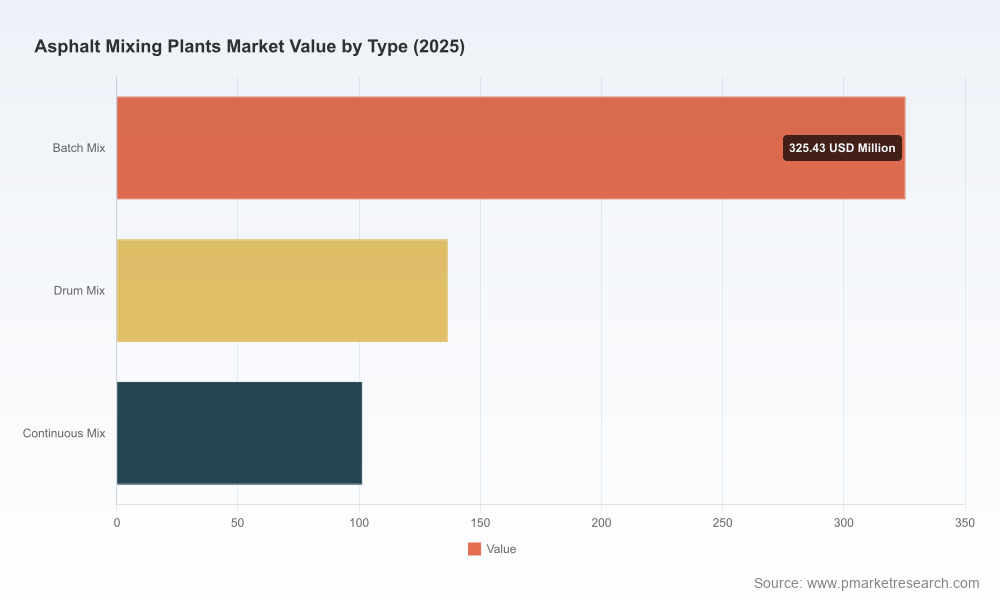

Marini — With a traditional strength in continuous mix systems and road-maintenance equipment, Marini remains an important player in markets where operational continuity and integration with roadworks fleets are prioritized.

Parker Plant (Phoenix Transworld portfolio) — Focused on mobile and modular solutions, Parker Plant targets project-based buyers and rental operators who prize fast ramp-up and redeployment economics.

Recent trade-show activity in 2026—including major showcases with hundreds of exhibitors—has validated that technological differentiation is increasingly defined by recyclability, emission control, and fuel flexibility rather than pure throughput. In short: product road maps now signal environmental compliance and modular economics as commercial must-haves.

Air-quality compliance: Recent references to particulate limits and opacity thresholds highlight an operational requirement: plants must demonstrate continuous compliance with particulate and opacity metrics using accepted measurement methodologies during permitting. These requirements raise the floor on equipment specifications and influence capex calculations.

Environmental management systems: ISO 14001 is emerging as a de facto expectation among large infrastructure contractors and public owners. Certification can be a procurement differentiator and may accelerate project approval timelines in many jurisdictions.

Raw-material price signals: Terminal binder and structural material price levels are relevant inputs into lifecycle and replacement-cost models. Procurement teams should model multiple price scenarios when evaluating new plant purchases or retrofits to ensure resilience under commodity volatility.

Decision-grade market sizing and trends: A clear macro trajectory with an analytical backbone that supports capital planning and strategic business cases for FY 2026 investments.

Scenario modeling framework: Tailored scenarios that stress-test demand against regulatory tightening, recycling adoption rates and infrastructure spend shocks—complete with sensitivity matrices for capital-intensity, fuel mix and throughput.

Competitive intelligence dossiers: Vendor profiles, product positioning maps and capability checklists that allow procurement and product teams to accelerate vendor due diligence.

Regulatory playbook and compliance checklist: A practical guide to the air-permit landscape, measurement standards and ISO adoption pathways to shorten permitting timelines and reduce approval risk.

Operator’s toolkit: Total cost of ownership templates, retrofit decision matrices and a retrofit vs. replacement calculator designed for CFOs and plant managers assessing 2026 capex options.

Prioritize retrofitable solutions: Where permitting or budget constraints exist, retrofit options that enable higher RAP integration and low-emission burners yield faster ROI and reduced permitting hurdles compared to greenfield builds.

Lock in flexible fuel pathways: Require suppliers to demonstrate alternative-fuel readiness—hydrogen-capable burners and alternative fuel mixing capability should be evaluated as part of the primary technical spec.

Use scenario economics in approvals: Adopt PW Consulting’s scenario templates to stress-test projects across a range of binder and steel price outcomes to avoid downside surprise in capital-cost planning.

Leverage trade-show intelligence: Recent exhibitions have become a rapid prototyping ground for adoption signals. Procurement teams should use vendor demonstrations at industry shows as a shortlist filter before issuing RFQs.

Consider M&A or partnerships to capture technology gaps: Given moderate market concentration and the need for rapid capability acquisition (emissions control, RAP integration), strategic partnerships or tuck-in acquisitions can accelerate time-to-market for differentiated offerings.

This preview outlines the strategic contours that will matter in 2026, from regulation and input-cost pressure to the supplier moves that will shape competitive advantage. PW Consulting’s full Asphalt Mixing Plants Market report contains the granular scenario matrices, the complete set of vendor scorecards, and the detailed segmentation and regional analyses needed for definitive board-level decisions. To access the comprehensive datasets and actionable appendices that operationalize the insights summarized here, please visit our report page and download the full briefing.

For detailed analysis of this topic, please visit the official page:Asphalt Mixing Plants Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com