North America Automotive Electrical Connectors Growth Driven by EV Adoption

Other |

2026-06-23 09:50:59

Between 2020 and 2025 the global fiber optic preform market more than doubled, rising from approximately USD 4.0 billion to about USD 8.2 billion. Our base-year analysis (2025) and forward-looking projection show an accelerated trajectory into 2026 and beyond — the market is forecast to exceed USD 10.2 billion in 2026 and to approach USD 30.0 billion by 2032 under a compound annual growth rate of roughly 20.39%. For corporate leaders making capital-allocation, sourcing and M&A decisions in 2026, this report provides the operational playbooks, risk scenarios and competitive intelligence needed to convert momentum into durable advantage.

Fiber Optic Preform Market

Supply-side shocks and material scarcity: A rapid and sustained increase in key dopant prices (notably germanium dioxide) and abrupt changes to export regimes have created a structurally tighter upstream market. These shifts have lengthened lead times, compressed available supply and materially altered unit cost structures for preform producers.

Fiber Optic Preform Market

Pricing normalization and margin pressure: After a period of historic lows, optical fiber pricing has rebounded materially. This recovery helps revenue trajectories but transfers pressure to manufacturers’ input cost management and contract re-pricing strategies.

Fiber Optic Preform Market

Trade and tariff overlay: Recent customs rulings and Section 301-like tariff applications continue to change cross-border economics for cable and component supply chains. Companies with global footprints face differentiated impacts by production and final assembly location.

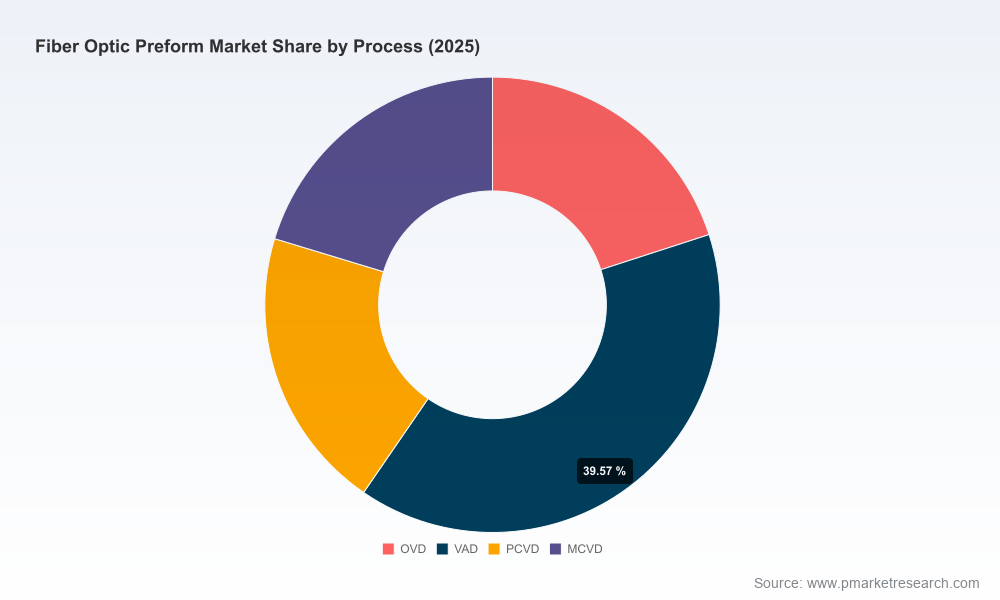

Technology and process diversification: VAD, OVD, PCVD and MCVD routes all remain relevant — but their capital intensity, scalability and material-sensitivity differ. Firms that align process investments with realistic raw-material scenarios and customer demand profiles will capture outsized returns.

PW Consulting’s Fiber Optic Preform Market Report is designed as an executable toolkit for 2026 decision-making rather than an academic survey. Key deliverables include:

Dynamic scenario models that map unit-cost curves against three raw-material price paths and two tariff regimes, enabling CFOs to stress-test profitability and pricing levers.

Supplier risk heatmaps and contingency playbooks that distinguish single-source exposures, captive integration options, and lead-time alleviation tactics (including on-shore buffer strategies and strategic inventory).

Capital allocation frameworks that translate process choices (VAD/MCVD/OVD/PCVD) into phased capex, expected throughput, break-even timelines and sensitivity to dopant pricing.

M&A and JV scorecards prioritizing targets by technology fit, production scale, geographic footprint and regulatory risk — with a practical 90/180/360-day integration checklist for rapid captures.

Commercial playbooks for contract design: recommended pass-through clauses, indexation mechanics, volume-flex options and escrow models to share material-price volatility with customers while protecting margin.

Regulatory-monitoring matrix and advocacy plan that aligns trade, export control and procurement strategies with evolving policy exposures.

The preform ecosystem is dominated by established optics and materials firms with vertically integrated capabilities, legacy process know-how and global customer relationships. Strategic implications for market participants include:

Incumbent manufacturers with process leadership (e.g., vapor-deposition specialists) hold the shortest path to scale but are most exposed to dopant price swings. Their advantages are speed-to-market and existing offtake agreements; their vulnerabilities are concentrated supplier networks and capital-cycle exposure.

Materials and specialty-chem firms with large-diameter preform capabilities offer differentiated product sets for specialty fiber markets. For companies seeking to move up the value chain or secure premium margins, these players are logical partners or acquisition targets.

Integrated cable manufacturers with captive preform capacity create pressure on independent suppliers through internal transfer pricing and preferential allocation in constrained periods. Customers and investors should read integration moves as defensive strategies to protect downstream margins.

Within the report we provide individual strategic profiles of major global participants — highlighting manufacturing footprint, dominant process routes, technology specializations and partnership posture. These organization-level dossiers equip corporate development teams to prioritize counterparty engagement, vendor audits and potential alliances.

Two themes dominate the near-term external environment:

Material-price volatility: Benchmarks and delivered prices for critical dopants have moved sharply higher over the last 24 months. This has made unit-cost predictability a core commercial risk and has elevated the value of upstream hedges, strategic inventories and supplier development programs.

Regulatory fragmentation: Export licensing and prohibition actions from major producing countries, alongside customs and tariff rulings in importing markets, are raising transaction costs and making reshoring or regionalization a pragmatic alternative for many buyers. Regulatory risk must be modeled as a first-order input into plant siting and long-term contracts.

De-risk the supply stack: Implement dual-sourcing for critical dopants, establish strategic safety stock levels and negotiate material-linked pricing formulas. For high-volume applications, consider equity stakes or long-term take-or-pay offtakes with upstream producers.

Invest in process optionality: Prioritize capacity additions and retrofits that allow switching between deposition techniques or that reduce dopant intensity per meter of fiber, allowing flexible production mixes as product demand and material economics evolve.

Pursue targeted consolidation and partnerships: Use M&A and alliances to secure midstream capability, accelerate new-process commercialization and lock in regional supply for regulated geographies. Focus on targets that materially shorten time-to-market or materially lower per-unit capital requirements.

Commercial agility and contract innovation: Adopt indexing clauses tied to transparent input-price benchmarks, create hybrid fixed/variable contracts and deploy conditional volume releases that protect both supplier and buyer in volatile cycles.

We designed the report to move clients from insight to action within 60–120 days. Deliverables include:

Operational templates: supplier RFPs, vendor audit checklists, capex decision matrices and integration playbooks for roll-ups.

Financial tools: downloadable cost-build spreadsheets and scenario drivers that plug directly into corporate planning systems for rolling forecasts.

Commercial materials: recommended contract language, pricing-index models and customer-retention scripts tailored to fiber and preform supply agreements.

Decision-support dashboards: interactive visualizations that allow executives to see the sensitivity of margins, utilization and ROIC to material-price, tariff and demand scenarios.

CEOs and COOs of fiber and cable manufacturers planning capacity upgrades or regionalization strategies.

CFOs and procurement leaders who must reconcile revenue growth with escalating input price volatility and tariff exposure.

Corporate development and private-equity teams evaluating M&A targets, roll-up plays or minority investments in midstream assets.

Technology and operations leaders deciding process investments and R&D prioritization between deposition routes.

90 days: Complete supplier exposure mapping, insert material-index clauses into new quotes, and run a two-scenario unit-cost sensitivity to current dopant prices.

180 days: Negotiate strategic offtake or inventory agreements, approve phased capex for process optionality, and launch technical due diligence on one high-priority acquisition target.

360 days: Commission at least one de-risking initiative (regional capacity, captive supply stake or joint-venture), finalize long-term contracts using indexed frameworks and implement an executive dashboard for rolling scenario analysis.

The fiber optic preform market is entering a phase where demand growth and input constraints are simultaneously intensifying commercial opportunity and operational risk. Our 2026-focused report converts high-level trends into actionable plans: it quantifies how different raw-material, tariff and process choices affect unit economics; it prescribes procurement and commercial clauses that preserve margin under volatility; and it evaluates competitive targets and partners against a pragmatic, execution-oriented rubric. For any executive or investor needing to make binding capital, sourcing or M&A commitments in 2026, this report is designed to be the single most practical briefing you will read.

To access the full set of models, company dossiers and operational playbooks, visit PW Consulting’s report page for the Fiber Optic Preform Market and request the executive data package and scenario workbooks.

For detailed analysis of this topic, please visit the official page:Fiber Optic Preform Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com