Digital X-Ray Systems Market 2026: Strategic Intelligence Brief — PW Consulting

As health systems, device manufacturers, and investors prepare their 2026 playbooks, the Digital X-Ray Systems market poses a distinct blend of steady expansion and tactical complexity. PW Consulting’s new market study — anchored on a 2025 base year and tracking historical performance from 2020–2025 with forecasts through 2032 — synthesizes the quantitative trajectory and practical, executable guidance leaders need to make confident decisions in the year ahead.

Digital X-Ray Systems Market

Market snapshot: measured growth with implications for scale and scope

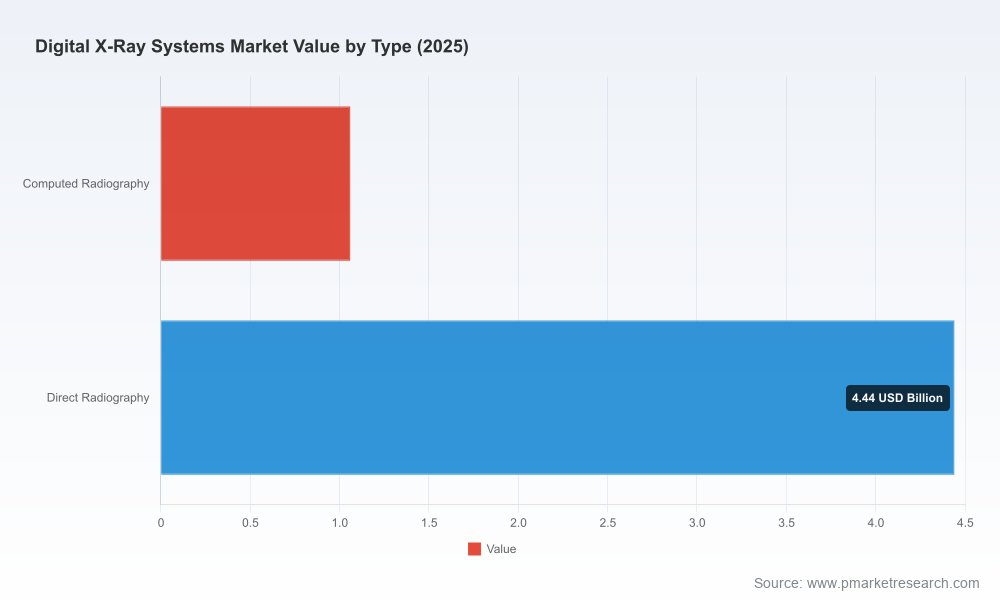

The Digital X-Ray Systems market has demonstrated resilience across a turbulent macro cycle: our time-series sizing shows recovery and steady expansion from 4.52 Billion USD in 2020 to an estimated 5.50 Billion USD in 2025, with trajectory continuing to roughly 6.86 Billion USD by 2032 under current assumptions. The modeled compound annual growth rate (CAGR) for the forecast window is 4.5% — a pace that signals reliable topline growth but not runaway disruption. Put simply: the market rewards disciplined scale, selective innovation, and regulatory navigation more than speculative product bets.

Digital X-Ray Systems Market

Equally instructive is market structure. Our concentration analysis (CR3 at ~24.6% and CR5 at ~26.2%) highlights a fragmented vendor landscape with no single dominant supplier — a fact that shapes pricing dynamics, channel strategies, and M&A calculus. Fragmentation creates opportunities for differentiated entrants, but it also increases the importance of repeatable go-to-market motions and service-led differentiation.

Digital X-Ray Systems Market

Why this matters for enterprise strategy in 2026

- Capital allocation and portfolio prioritization: With mid-single-digit CAGR and predictable adoption curves, capital deployment should prioritize modular upgrades (detectors, software, mobile integration) and recurring-revenue services over large, low-turnover hardware bets.

- M&A and partnership playbooks: Given the fragmented supplier base, bolt-on acquisitions that close capability gaps (wireless detectors, AI-enabled workflow, OEM-to-OEM interoperability) can accelerate time-to-market at a lower risk than greenfield investment.

- Procurement and contracting: Health systems should negotiate for lifecycle services and pathway-based bundles rather than one-off equipment purchase discounts. The economics of detector replacement and software updates will increasingly drive total cost of ownership.

- Regulatory and reimbursement alignment: Recent coding and policy updates alter revenue capture for advanced imaging and AI-enabled interpretation. Embedding compliance and reimbursement scenario-planning into product roadmaps is no longer optional.

Report deliverables: what leaders will use on Day 1

PW Consulting’s Digital X-Ray Systems Market report is designed as an operational toolset, not an academic monograph. Key, actionable components include:

- Proprietary market model (2020–2032) with scenario toggles for adoption rates, price erosion, and replacement cycles — presented at a consolidated level and available for licensed users to interrogate.

- Decision frameworks for capital budgeting, vendor selection, and service model transformation — including ROI templates calibrated to regionally adjusted utilization assumptions.

- Vendor assessment dossiers that map product portfolios, technology differentiators (detectors, mobile platforms, software), distribution strategies, and recent inorganic activity.

- Channel and installation playbooks for health systems and distributors that reduce deployment friction for mobile and fixed solutions — plus migration templates for CR-to-DR upgrades.

- Regulatory and reimbursement impact matrix, with concrete actions to optimize coding capture and to fast-track coverage for AI-enabled features.

- Executive briefings and slide-ready materials for board and investment committees, enabling rapid, evidence-based approvals.

To honor the “trailer” principle and protect the report’s proprietary subsegment analysis, our public brief demonstrates methodology and key conclusions while intentionally omitting the granular subregional, application, and pricing tables that subscribers receive in full.

Competitive landscape: positioning and strategic moves to watch

The vendor field combines global industrial majors, specialist detector manufacturers, and agile regional players. Our analysis profiles the firms shaping near-term competition, summarized by capability focus and strategic posture:

- Siemens Healthineers (Forchheim, Germany) — a systems integrator with emphasis on advanced digital X-ray platforms and detector integration. Their regulatory momentum around mobile systems positions them well for hospital fleet modernization.

- GE HealthCare (Chicago, United States) — continues to push high-throughput floor-mounted systems and integrated wireless detectors into high-volume imaging environments; recent commercial launches expand choice for busy radiology departments.

- Canon Medical Systems (Otawara, Japan) — combines detector innovation with hybrid system form factors to address both fixed and mobile use cases; targeted launches in key markets reflect a push into higher-margin detector-enabled systems.

- Konica Minolta Healthcare (Tokyo, Japan) — focuses on wireless detector technology and mobile radiography scenarios, targeting settings where flexibility and rapid imaging are critical.

- Carestream Health (Rochester, NY, United States) — balances wireless and fixed detector portfolios with mobile X-ray systems; regulatory clearances have recently expanded their European market options.

- Agfa HealthCare, Varex Imaging, Shimadzu, DMS Imaging — each occupies distinct niches from CR-to-DR conversion solutions to high-resolution detectors, collectively contributing to the market’s fragmented character and a rich supplier marketplace for procurement teams.

Recent, market-moving events underscore strategic priorities:

- Mid-2025 saw a new floor-mounted offering with integrated wireless detectors reach commercial availability, signaling supplier focus on throughput and ergonomics for large imaging centers.

- Early 2025 regulatory clearances expanded mobile and detector portfolios for multiple vendors, lowering barriers for fleet upgrades in Europe and North America.

- Product introductions in 2025 also emphasized hybrid detector formats, reflecting demand for solutions that bridge fixed rooms and portable workflows.

Regulation, reimbursement, and operational dynamics

The operating environment for digital radiography is increasingly shaped by coding and policy shifts that directly affect revenue capture and investment returns. Notable context for 2026 decision-makers includes:

- The 2026 CPT code set introduced a substantive number of codes that reflect digital health and AI-enabled diagnostic workflows; this change creates both opportunity and complexity for reimbursement optimization.

- U.S. and EU regulatory developments have continued to clarify safety and interoperability expectations for mobile systems with integrated wireless detectors, reducing time-to-adoption risk for hospital purchasers.

- Medicare coding policy updates address specificity for digital X-ray procedures, which can materially influence billing practices and the prioritization of technology upgrades in public-payor contexts.

For vendors and health systems, the net effect is clear: product roadmaps, clinical validation efforts, and sales propositions must explicitly map to reimbursement pathways and regulatory compliance timelines if commercial targets are to be met.

How leaders should use this intelligence in 2026

- CEOs and CFOs: Use the report’s market model to stress-test investment scenarios across conservative, base, and accelerated adoption cases. Our templates convert market share moves into P&L and working capital effects.

- Heads of Product and R&D: Prioritize detector modularity, workflow automation, and AI integrations that are likely to be reimbursable and that lower the total cost of imaging delivery.

- Commercial leaders: Build bundled service offerings and outcome-linked pricing where possible; the fragmented supply base amplifies the commercial advantages of end-to-end service commitments.

- Procurement and clinical engineering: Leverage the vendor dossiers to craft tender specifications that favor lifecycle economics and interoperability rather than lowest upfront price.

Subscription, access, and next steps

This public brief surfaces the strategic conclusions and operational levers that matter for 2026 planning while preserving the report’s proprietary subsegment matrices, regional roll-ups, and supplier financial benchmarks for subscribers. Organizations seeking the granular datasets, interactive model access, and tailored executive briefings can license the full Digital X-Ray Systems Market report from PW Consulting. Our subscriber package includes model files, vendor scorecards, and a one-hour analyst briefing to translate insights into your 2026 action plan.

In a market characterized by steady growth, technological modularity, and regulatory-national nuances, the winners in 2026 will be those who align product architecture with reimbursement realities, who build repeatable service economics, and who selectively consolidate capability to accelerate time-to-market. PW Consulting’s research is built to make those choices less risky and more predictable.

For detailed analysis of this topic, please visit the official page:Digital X-Ray Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com