Understanding the Adiponitrile Chemical Value Chain: From Butadiene to Nylon 6,6 and Beyond

Art |

2026-04-23 12:22:50

PW Consulting’s latest PLGA Market report (base year 2025; forecast period 2026–2032) offers a practical, boardroom-ready intelligence package designed to influence executive decisions in 2026 and beyond. Our modeling shows the PLGA market roughly doubling from its mid‑decade baseline and progressing at a compound annual growth rate of approximately 13.5% through 2032. With total market value established in 2025 and a compelling trajectory toward 2032, this report translates macro momentum into prioritized actions across sourcing, product development, regulatory strategy, and commercial partnerships.

PLGA Market

PLGA (poly(lactic-co-glycolic acid)) has matured from a niche biomedical polymer to a platform material used in long-acting injectables, implantables, tissue scaffolds and next‑generation drug‑delivery matrices. For 2026 planning cycles—capex approvals, supplier selection, R&D roadmaps and M&A screening—leadership teams need more than headline growth rates. They need scenario-tested implications for supply chains, cost pass-through risk, regulatory timelines and partner ecosystems. Our report provides that bridge: it combines an independent, data‑driven market forecast with actionable, operational playbooks that can be executed within 12–18 months.

PLGA Market

Key macro takeaways from the report:

PLGA Market

PW Consulting designed the report to be immediately operational for strategy teams. Highlights include:

The PLGA ecosystem remains fragmented, with a mix of specialized polymer producers, large chemical players, and regional manufacturers. The report includes detailed profiles and strategic analysis of the principal suppliers market participants, including:

Corbion’s PURASORB® line positions it as a key supplier of GMP‑grade PLGA and PLA copolymers for controlled‑release drug delivery. Our assessment highlights Corbion’s vertical integration into lactic acid production and its role in supplying large‑scale PLA producers—a structural advantage when global feedstock shifts occur.

Evonik’s RESOMER® and LACTEL® product families are prominent in parenteral and implantable applications. Evonik’s distribution partnerships in Europe and investments in regulatory support services make it a preferred partner for firms seeking established product dossiers and supply continuity in regulated jurisdictions.

Akina supplies research and specialty PLGA grades (PolySciTech®/PolyVivo®) targeting R&D labs and early clinical development. Their niche is agility and tailored polymerization options—valuable for formulation teams pursuing customized degradation profiles.

Merck’s distribution reach and reputation for research‑grade and GMP‑compliant polymers make them a logical partner for developers balancing quality, traceability and global regulatory acceptance.

Regional producers like Nomisma offer cost‑competitive sourcing and local capacity for Asia‑focused projects. The strategic choice between premium global suppliers and competitive regional manufacturers requires careful assessment of regulatory and supply‑risk tradeoffs.

Across these profiles, our competitive intelligence emphasizes supplier strengths in GMP compliance, R&D collaboration, geographic reach and the ability to support scale‑up pathways for clinical and commercial volumes.

Executives need to factor in a handful of rapid developments that materially affect 2026 decisions:

We distill the report’s findings into five priority actions for executives preparing 2026 plans:

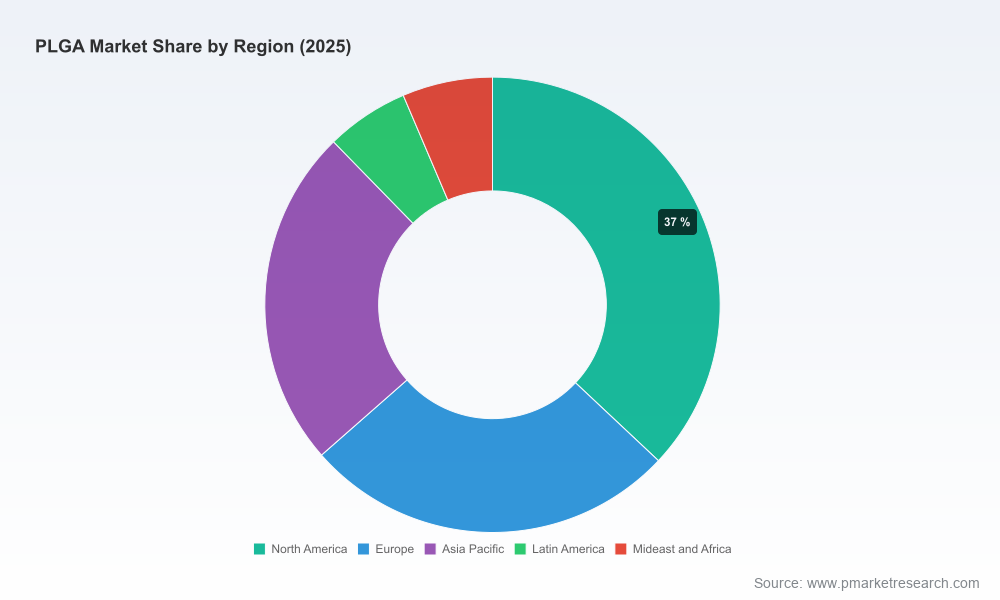

This article is a concise briefing of the strategic insights contained in PW Consulting’s full PLGA Market report. The complete dossier includes granular forecasts, supplier scorecards, regional capacity maps, contract templates, and an Excel model you can adapt to your portfolio. We intentionally withhold detailed sub‑segment tables and regional shares here to preserve the utility of the full dataset; those elements are available in the report and through our consultancy engagements.

For procurement directors, R&D heads, M&A teams and strategy officers preparing 2026 budgets and roadmaps, the report provides both the quantitative foundation and the practical playbooks needed to convert market growth into competitive advantage. To access the full report and data toolkit, or to commission a tailored workshop that applies the findings to your pipeline, please visit PW Consulting’s PLGA Market page or contact our industry team directly.

PLGA is at an inflection point: scientific validation, regulatory acceptance and commercial demand are aligned, but supply and policy headwinds require targeted managerial action. With market value projected to expand meaningfully through 2032, organizations that implement the operational safeguards and strategic partnerships outlined in our report will convert market growth into durable competitive advantage. PW Consulting’s PLGA Market report is designed to be that executional bridge—turning forecasted opportunity into a prioritized 12–24 month action plan.

For detailed analysis of this topic, please visit the official page:PLGA Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com