Why Professional CV Formatting Matters for Career Growth

Other |

2026-05-20 14:54:12

Healthcare facilities are undergoing an operational rethink: maximizing clinical throughput while minimizing risks and physical clutter. Ceiling-mounted supply pendants with columns have become central to that transformation. PW Consulting’s latest market study uses a 2025 base year and a seven-year forecast window to deliver decision-grade intelligence. The overall market has expanded meaningfully from the beginning of the decade and closed 2025 at roughly USD 568.5 Million. Our forward view projects continued expansion through 2032, with a conservative compound annual growth rate of 1.88% for the forecast period — reaching an anticipated market level in the low-to-mid six hundreds of millions of dollars by 2032.

Ceiling-mounted Supply Pendants with Column Market

For executives and capital planners preparing 2026 budgets, that combination of steady baseline demand and modest forecast growth creates a specific set of strategic choices: prioritize retrofit vs. new-build, weigh modularity and aftermarket services, and structure procurement to capture lifecycle value rather than one-time equipment cost savings. This briefing outlines the report’s strategic value and how it converts macro intelligence into immediate actions for buyers, OEMs, hospital planners and investors.

Ceiling-mounted Supply Pendants with Column Market

Market sizing & trajectory: A reproducible topline model from historical data (2020–2025) through a scenario-based 2026–2032 forecast. Readers get both base and downside scenarios calibrated to regulatory and material-cost shocks.

Ceiling-mounted Supply Pendants with Column Market

Risk and opportunity heatmaps: Supplier concentration, procurement dependency, material-cost exposure (notably aluminum alloy and corrosion-resistant components), and regulatory vectors such as NFPA 99:2024.

Procurement playbook: A practical checklist for tenders, vendor evaluation criteria, scoring templates, and negotiation levers that align with hospital capex cycles and reimbursement norms.

Technical and compliance toolkit: Installation checklists, interface requirements for medical gas systems, fixtures interoperability, and an NFPA 99 compliance map tailored for ceiling-mounted systems.

Commercial due diligence: A vendor short-listing framework, total cost of ownership (TCO) templates, service-level benchmarking, and a maintenance & spare-parts roadmap.

Implementation case studies and pilot designs: Example specifications and layouts for acute care, operating theatres, and space-constrained facilities to accelerate decision making.

Below are the issue areas where the report provides immediate, implementable guidance for 2026 decisions.

Capital allocation and timing: Given the market’s steady base and modest forecast growth, our modelling favors staged investment for most systems: prioritize critical zones (e.g., major ORs and ICUs) and deploy modular pendants that preserve flexibility for future upgrades. This approach reduces immediate capex while creating upgrade pathways aligned with evolving clinical requirements.

Procurement design: Procurement documents should codify retrofit complexity, integration with existing medical gas infrastructure, and lifecycle service obligations. Our vendor-scoring template scores not only list price but also interoperability, spare-parts lead time, and engineering support — factors proven to dominate lifecycle costs.

Regulatory & engineering alignment: Updated NFPA 99:2024 standards will be a gating factor in many jurisdictions for installation approvals. The report includes a compliance matrix mapping standards to typical installation pitfalls so project managers can avoid schedule slippages and rework.

Supply chain resilience: Aluminum alloys and corrosion-resistant parts are core inputs. Procurement teams should establish risk buffers and multiple-sourcing strategies for critical components to insulate projects from raw-material price swings and single-source supplier failures.

Service and aftermarket as a competitive battleground: With a concentrated vendor topology and higher share of lifecycle cost attributable to maintenance, service agreements, spare parts availability and remote diagnostics become powerful differentiators. Hospitals can use these levers to extract value and reduce downtime risk.

Modularity and workflow integration: The operational benefits of ceiling-mounted units — reduced floor clutter and improved staff mobility — are quantifiable. The report provides a method to translate these workflow improvements into bed-turnover and staff-time savings, enabling ROI calculations that go beyond equipment line-item costs.

The market exhibits measured concentration: our concentration metrics indicate a moderate degree of aggregation among the top suppliers. The top three providers account for a meaningful share of market activity, and the top five increase that concentration further — an important consideration when negotiating for competitive pricing, support commitments and long-term parts availability.

Key players profiled in the report include established medical-technology and specialist OEMs with distinctive strengths:

Drägerwerk AG & Co. KGaA — recognized for modular ceiling-mounted units designed for acute care and surgical workstations that emphasize integrated medical-gas and electrical delivery in clutter-reducing configurations.

Tedisel Medical S.L. — a notable innovator in motorized and non-motorized column solutions for ICU and OR environments, with recent product initiatives targeted at modular ICU setups.

Starkstrom — focused on clinical-grade pendants offering pneumatic braking and clinically-oriented column geometries for critical care theatres.

Novair Medical — offers multiple configurations aimed at space-constrained facilities and robust medical-gas management integration.

Brandon Medical — positions itself around theatre systems and power platforms, increasingly integrating sensors and digital monitoring into supply pendants.

KLS Martin SE & Co. KG — provides high-flexibility ceiling supply units with notable room-positioning adaptability for operating rooms.

Maquet (Getinge AB) — integrates ceiling supply units with broader surgical workstation systems, including lighting and workflow integration.

Recent vendor moves — a product launch from one supplier and a high-profile project supply by another — underline how new offerings and turnkey projects can shift competitive dynamics in the near term. The report dissects these moves and assesses their implications for procurement and partnership strategies.

Buyers (hospitals, health systems): Run a 90-day procurement readiness sprint using our tender template, compliance checklist and TCO model to convert strategic intent into an actionable RFP that vendors can respond to consistently.

OEMs and integrators: Use the report’s feature-importance matrix and service-bundle economics to adjust product roadmaps and aftermarket offerings — focus investment on remote diagnostics, modularity and installation engineering.

Private equity and corporate development: The report provides a quick-reference consolidation playbook and valuation sensitivities tied to service revenues and spare-parts margins, useful for transaction screening and integration planning.

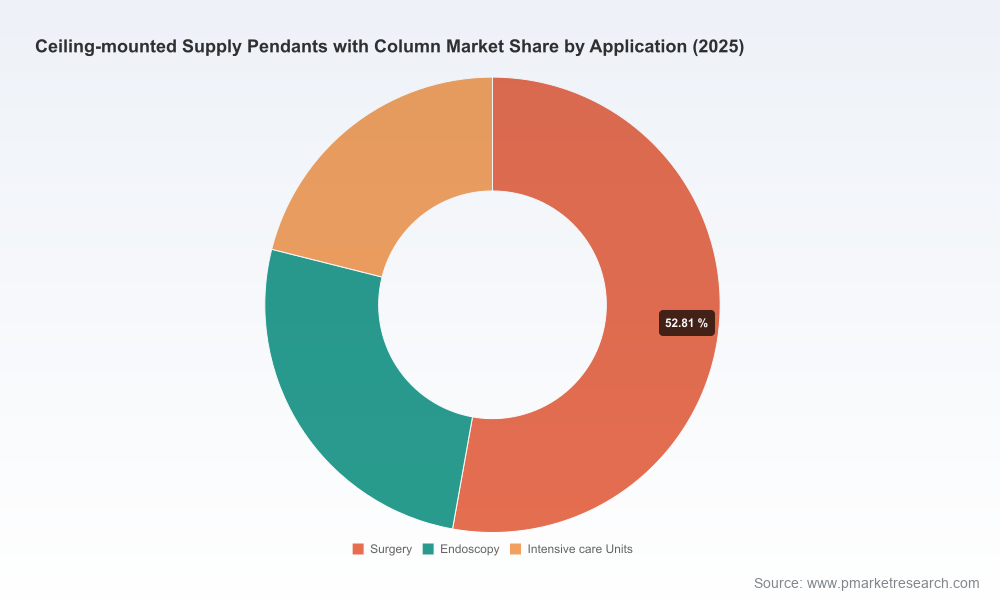

In line with PW Consulting’s “trailer” approach, this briefing intentionally demonstrates analytical depth while withholding specific segmented revenue slices and regional/application share tables that are part of the full intelligence product. Those granular splits — which drive detailed sourcing strategies, localized product mixes and precise price benchmarking — are included in the full report and associated data workbook. For procurement teams and investors seeking the exact regional and application-level figures, supplier share matrices and downloadable vendor scorecards, the complete dataset and appendices are available through the report webpage.

For executive teams preparing 2026 capital plans, the immediate priorities are clear: align procurement cycles with clinical modernization timelines, embed NFPA 99 compliance into project scopes, and structure vendor agreements that prioritize lifecycle value. PW Consulting’s full report supplies the segmented market intelligence, vendor benchmarking, and procurement tools to turn those priorities into executable programs. Visit our report page to access the complete dataset, downloadable templates and a schedule for our upcoming webinar series where our analysts will walk through the models and answer implementation questions.

For detailed analysis of this topic, please visit the official page:Ceiling-mounted Supply Pendants with Column Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com