Dive into Puzzle Bliss: A Beginner's Guide to Block Blast

Games |

2026-05-08 03:23:20

PW Consulting today releases a strategic preview of our forthcoming Sausage/Hotdog Casings Market report — a decision-focused briefing designed to arm C-suite and business-unit leaders with the situational awareness required to sharpen 2026 investment, sourcing and product strategies. Grounded in a detailed historical baseline (2020–2025) and a robust forecast framework (2026–2032), the study synthesizes market dynamics, regulatory shifts, raw-material pressures and competitive moves into a practical playbook. Key macro facts at a glance: the global market is sized at USD 3,900 Million in the 2025 base year and the outlook embeds a 4.7% CAGR over the forecast horizon, reaching roughly USD 5,350 Million by 2032.

Sausage/Hotdog Casings Market

Size and trajectory. The market’s mid-single-digit CAGR reflects steady end-demand from processed meat manufacturers combined with structural change in supplier economics and regulatory frameworks. For 2026 planning cycles, the headline numbers indicate a market that is expanding but also shifting in composition — creating both scale opportunities and margin pressure.

Sausage/Hotdog Casings Market

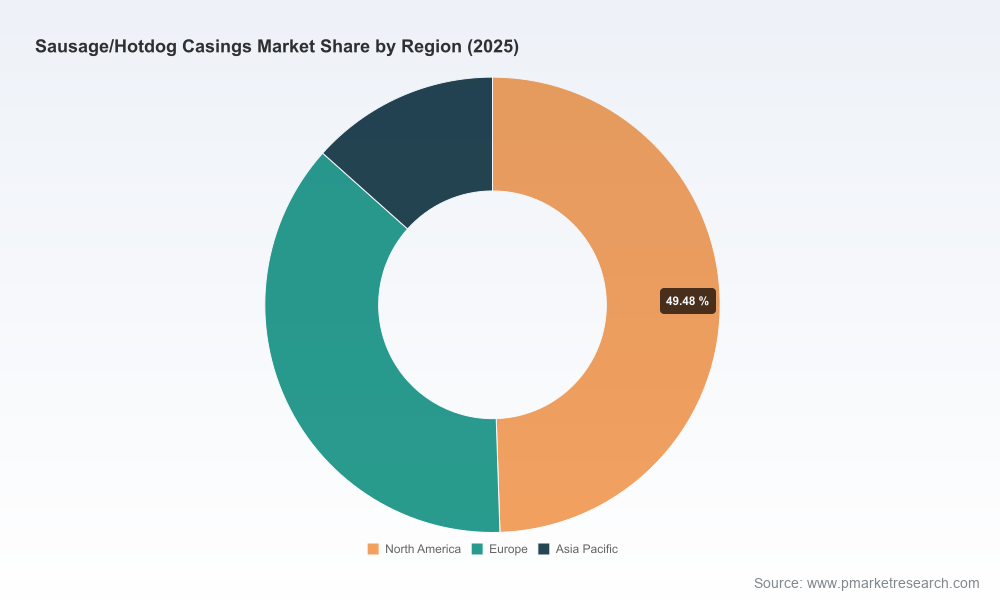

Concentration. Market concentration is meaningful: the top three suppliers account for roughly half of market share, with the top five covering a clear majority. This architecture drives both competitive intensity and opportunities for focused challengers to win niches through innovation or channel control.

Sausage/Hotdog Casings Market

Timing. With regulatory updates and raw-material cost inflation accelerating in 2024–2025, 2026 becomes a hinge year: firms that invest early in traceability, alternative feedstocks and compliance-ready formulations will capture outsized share as buyers re-contract supply.

Executive dashboard: market size, growth drivers, scenario-ready forecasts (historical 2020–2025; forecast 2026–2032) presented with sensitivity to price and input-cost trajectories.

Regulatory tracker: rolling summaries of national and supranational actions with compliance implications, plus an “action checklist” for formulation, labeling and testing.

Supply-chain and raw-material analysis: cost-pressure mapping, supplier concentration mapping, and supplier scorecards for bovine/porcine collagen, cellulose, fibrous and emerging alternatives.

Competitive intelligence: strategic profiles of leading vendors, comparative capability matrices, go-to-market footprints and recent deal and alliance activity.

Innovation landscape: technology readiness assessments for plant-based, marine- and lab-grown alternatives, and R&D commercialization timelines.

Commercial playbook: route-to-market strategies, pricing templates, procurement negotiation levers, and prioritised use cases for premiumisation or cost-optimization.

Scenario planning module: three scenarios (baseline, regulatory-tight, substitution-accelerated) with quantified P&L and working-capital implications for 2026–2028 planning cycles.

Regulatory tightening. Recent regulatory activity in major markets — including updates to food-contact recommendations and proposals to delist certain color additives — is already influencing formulation choices and testing burdens. These actions increase the cost of non-compliance and shorten lead times for product approval cycles.

Traceability and sustainability costs. Collagen supply chains have faced sustained compliance-driven cost increases in recent years, with traceability and sustainability requirements adding a recurring cost burden. Buyers and producers are increasingly pricing-in these costs and seeking long-term supplier commitments.

Material innovation and substitution pressure. Growing scrutiny of livestock-sector emissions, coupled with brand- and retailer-level sustainability targets, is prompting accelerated R&D into marine, plant-based and cultured alternatives. These alternatives remain emergent but are moving from lab to pilot commercialisation.

Consolidation and co-branding. The market shows a pattern of strategic partnerships and selective brand launches oriented around combined value propositions — a recent example being a joint customer-facing brand to deliver integrated natural + collagen solutions. Such moves signal an emphasis on bundled offers and single-source convenience for processors.

Market leaders. Large incumbent suppliers maintain strengths in scale manufacturing, global distribution and regulatory know-how — attributes that support volume contracts with multinational processors and that enable elevated R&D investments into higher-performance casings.

Specialist challengers. Mid-market and regional specialists compete on niche attributes: premium natural casings for artisanal producers, highly engineered collagen for smoked and cooked applications, and fibrous/cellulose formats for skinless and hot-dog production.

Channel and service plays. Several players differentiate via vertical relationships — offering integrated packaging, filling equipment compatibility or technical service teams that reduce customer switching costs and justify price premia.

Recent corporate activity. Brand co-launches, supplier-level regulatory advisories and national guidance revisions are compressing the runway for firms that lack compliance and innovation capacity.

Priority 1 — Regulatory-first product roadmaps. Make regulatory intelligence a gating criterion for 2026 R&D and commercialization. Update formulations, retest legacy SKUs and secure pre-approval letters where possible.

Priority 2 — Traceability investments as a commercial lever. Invest in visible provenance systems and supplier auditing; buyers increasingly prefer pay-for-trace models that reduce procurement friction.

Priority 3 — Diversify raw-material exposure. Hedge bovine/porcine sourcing risk by accelerating validated alternatives (marine/plant/cultured) and by securing multi-year supply contracts for critical inputs.

Priority 4 — Product-tiering and premiumization. For processors targeting retail or foodservice premium segments, differentiate via functional benefits (smoke adhesion, bite, cooking yield) and sustainability credentials that support higher ASPs.

Priority 5 — M&A and strategic partnerships. Given the market’s concentration, acquisitive moves or alliances can fast-track capability building (e.g., plant-based casing tech) and extend channel reach.

Priority 6 — Operational resilience. Revisit manufacturing footprint and inventory policies to manage compliance-driven retooling and to de-risk single-source inputs.

Priority 7 — Commercial contracting and pricing discipline. Re-model contracts to include escalators for compliance costs and input inflation; consider indexation clauses to protect margins.

Priority 8 — Customer-centered innovation. Co-develop SKUs with anchor customers to lock-in share and accelerate adoption of alternative casings via joint marketing and supply commitments.

Regulatory shock: If major jurisdictions accelerate prohibitions or reclassifications, firms without rapid re-formulation capability face product delisting and lost contracts. Mitigation: parallel certification tracks and contingency inventories.

Input-cost escalation: Continued compliance-driven increases could compress margins within 12–24 months. Mitigation: contract re-pricing, vertical integration and alternative feedstock pilots.

Substitution acceleration: Faster-than-expected adoption of plant-based or cultured options would re-segment demand. Mitigation: invest selectively in strategic options and secure IP or partnerships.

Portfolio prioritisation. Use the report’s scenario outputs to classify product lines into invest/maintain/exit buckets for 2026 CAPEX planning.

Procurement strategy. Leverage the supplier scorecards and concentration analysis to negotiate multi-year terms or to qualify second-source suppliers.

Innovation roadmap. Align R&D milestones with regulatory timelines and pilot customers identified in the report to reduce commercialization cycle time.

M&A playbook. The intelligence package provides target profiles and valuation primers to accelerate diligence for bolt-on acquisitions or capability partnerships.

PW Consulting’s full Sausage/Hotdog Casings Market report contains the comprehensive datasets, segmented analyses and vendor-level benchmarking that underpin these strategic recommendations. This preview is designed to surface the levers that will matter most in 2026; the complete report provides the granular segmentation and supporting exhibits required to execute with precision.

To access the full dataset, vendor profiles and scenario models — or to request a tailored executive briefing for your leadership team — contact PW Consulting. Our analysts will walk you through the decision-ready materials and translate findings into a bespoke 90‑day action plan aligned to your 2026 objectives.

For detailed analysis of this topic, please visit the official page:Sausage/Hotdog Casings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com