Liposomal Doxorubicin Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-16 07:46:50

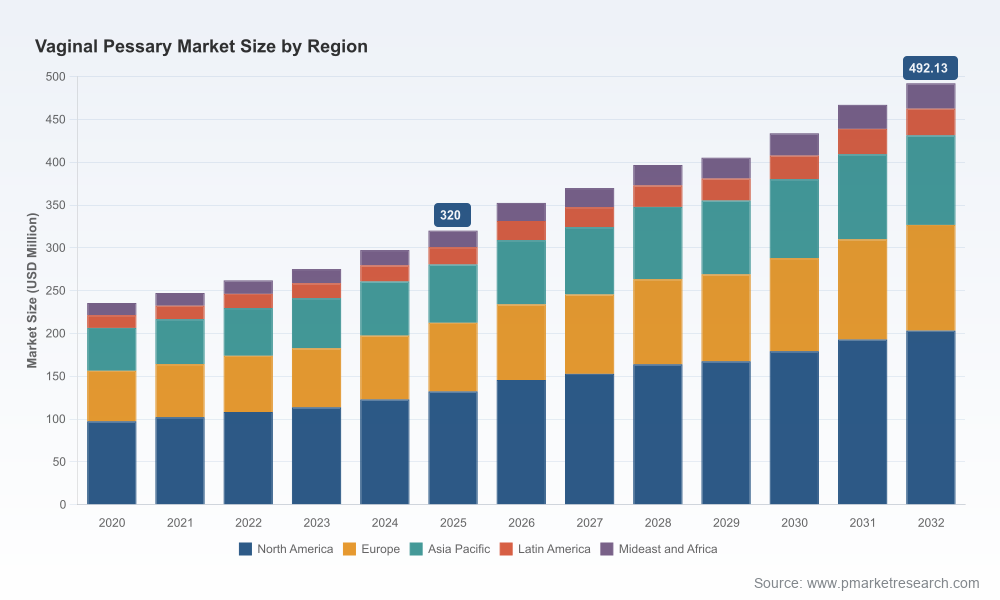

As health systems and device manufacturers plan for the medium term, our latest Vaginal Pessary Market report (base year 2025) frames a clear, data-driven roadmap for corporate decision‑makers preparing investments, go‑to‑market pivots, and M&A activity in 2026. The global market reached USD 320.0 Million in 2025 and, under a central-case trajectory, is projected to grow at a compound annual growth rate (CAGR) of 6.5% through the 2026–2032 forecast window. By 2032, the market is expected to approach roughly half a billion dollars, reflecting a stable, clinically essential device category that is evolving through product innovation, changing care settings, and payer dynamics.

Vaginal Pessary Market

Clinical continuity with compelling commercial upside: Vaginal pessaries remain a frontline non‑surgical option for pelvic organ prolapse (POP) and some forms of urinary incontinence. The combination of an aging population, rising preference for conservative management, and renewed product innovation creates a predictable, investible demand base.

Vaginal Pessary Market

Manageable scale with consolidation potential: Market concentration metrics indicate a middle‑market structure — leading firms capture a notable share but room exists for consolidation, adjacent diversification, and challenger strategies that add service layers around the device.

Vaginal Pessary Market

Regulatory and reimbursement tailwinds that can be shaped: Pessaries are regulated as Class II medical devices in key markets and are reimbursed through established HCPCS/CPT pathways. Companies that neutralize regulatory friction and align commercial models to reimbursement codes can accelerate adoption and margin expansion.

Product portfolio strategy: The market now supports a spectrum from classic reusable designs to single‑use, patient‑self‑administered systems. Commercial winners will define clear portfolio rules (when to prioritize disposables vs long‑lived devices), optimize SKU rationalization, and bundle clinical support to reduce fitting failures and churn.

Care pathway and channel reconfiguration: The rise of at‑home insertion devices and partnerships supporting community rollout signal an inflection in care pathways. Manufacturers must rethink clinic stocking models, telehealth-enabled fitting support, and distribution agreements with specialty device suppliers and retail/consumer health channels.

Reimbursement intelligence as a competitive moat: Understanding HCPCS Level II and relevant CPT codes — and how payer policies treat materials (e.g., rubber vs silicone) and fitting services — materially affects pricing power and acceptance in private and public systems.

Material & lifecycle economics: Raw material choices (PVC vs silicone) drive unit economics, clinician preference, and life‑cycle claims (e.g., washable reusable devices). Cost models that internalize washing, reuse, and end‑of‑life handling separate winners from laggards.

Evidence generation & claims architecture: A pragmatic clinical evidence strategy (real‑world outcomes, QoL endpoints, and cost‑offset analyses vs surgical pathways) shortens sales cycles to key hospital systems and supports value‑based contracting.

Actionable market-sizing and scenario models: Multi‑scenario forecasts (base, conservative, and upside) aligned to clinical adoption levers and reimbursement sensitivity; downloadable model inputs to stress‑test investment cases.

Commercial playbooks: Territory planning templates, clinic stocking playbook, and bundled service proposals (training, fitting support, patient education) to accelerate point‑of‑care uptake.

Pricing and reimbursement matrix: Benchmarks and negotiation tactics mapped to payer archetypes and codes, including guidance on positioning silicone vs rubber devices to capture premium reimbursement where justified.

Regulatory & quality checklist: Streamlined 510(k) pathways, device labeling considerations, and GMP elements tailored to firms scaling manufacturing or entering new markets.

M&A and partnership screening: Acquisition targets scored by capability gaps (distribution, digital enablement, disposable manufacturing) and integration playbooks to protect commercial momentum post‑close.

The competitive scene is populated by established gynecologic device suppliers and focused niche innovators. Several incumbent manufacturers supply broad portfolios and channel presence that support integrated clinic programs; newer entrants have introduced single‑use and patient‑centric designs that shift care models.

Incumbent manufacturers with broad clinical reach and wide device portfolios continue to sustain clinic relationships and capture routine fitting demand. Their strategic advantage is distribution scale, clinical education networks, and product breadth that supports same‑day fitting workflows.

Specialist device firms and agile start‑ups are reshaping at‑home care. The commercial launch and rollouts of user‑centric disposable devices have accelerated physician prescribing pathways and opened consumer channels, particularly when combined with commercialization partners that bring payer and patient engagement expertise.

Manufacturers offering integrated fitting sets and clinical kits remain critical to diagnostic and short‑term management markets; these products are central to practice workflows and represent a high‑value touchpoint for cross‑selling training and services.

Examples of the supplier archetypes profiled in the report include established medical device distributors focused on pessary portfolios, specialized manufacturers of silicone and disposable devices, and several newer entrants gaining regulatory clearances and commercial partnerships. Our company profiles summarize product strategy, commercial strengths, regulatory posture, and partnership activity, providing a pragmatic lens for partnership or competitive response planning.

Commercial launches of at‑home disposable pessaries have proven demand outside traditional outpatient clinics, prompting a rethink of distribution and patient education investments.

Strategic commercialization partnerships that bundle market access, patient support, and distribution have shortened time‑to‑prescription for some innovative products.

Regulatory clearances for new device designs validate clinical acceptability and lower market entry barriers for credible challengers.

Regulatory framework: Vaginal pessaries are treated as Class II devices in major markets and typically require 510(k) clearance plus compliant quality systems. Timely regulatory strategy and post‑market vigilance planning are non‑negotiable for 2026 market entry or product enhancements.

Reimbursement nuance: Billing codes exist for both the devices and the fitting/insertion procedures. Devices classified as non‑rubber (often silicone) generally align to higher reimbursement bands and reduced allergen liability — an important consideration for formulary positioning.

Material economics: PVC remains attractive for cost‑sensitive channels due to a long clinical history and lower unit cost, while silicone’s longevity and patient safety profile support premium pricing models, particularly where payers recognize reuse value.

Prioritize at‑home and disposable solutions where clinical evidence supports equivalent outcomes and where payer pathways can be secured. Early mover advantage exists for well‑executed commercialization partnerships that combine distribution with patient engagement services.

Optimize SKU portfolios to reduce clinician complexity and balance clinic stocking with patient‑direct options; use data from pilot rollouts to refine sizing and assortment rules before scaling.

Invest in reimbursement and economics teams that can translate device characteristics into billable value (e.g., positioning silicone pessaries for favorable HCPCS classification) and negotiate with payers.

Consider bolt‑on M&A to access disposable manufacturing, digital patient support platforms, or regional distribution to accelerate market expansion without diluting core R&D efforts.

Build evidence that resonates with purchasers: health‑economic models showing OR avoidance or deferred surgery, quality‑of‑life improvements, and service‑level outcomes that reduce clinic labor intensity.

Our study couples an empirically grounded macro forecast with operational playbooks and competitor intelligence, giving strategy, commercial, and regulatory teams the tools needed to make executable decisions in 2026. The market’s steady expansion and the mixture of incumbents and nimble entrants create multiple pathways to growth — but only companies that align product design, reimbursement strategy, and channel execution will capture disproportionate share as the category evolves.

PW Consulting’s Vaginal Pessary Market report delivers the synthesis and tactical guidance required to convert market insight into competitive advantage while deliberately withholding granular segment tables that are reserved for full subscribers. To access our complete segmentation, provider channel models, and downloadable financial scenarios, please visit our report landing page and download the executive package.

For detailed analysis of this topic, please visit the official page:Vaginal Pessary Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com