Carrying the Passion – Growth Dynamics in the Hitch Trunk Bike Racks Market

Other |

2026-05-25 12:00:11

PW Consulting’s latest Vegetable Protein Market research (base year 2025; forecast 2026–2032) maps a market that has more than doubled in momentum since 2020 and is projected to continue a robust expansion through the next decade. Our topline modelling shows the global market growing from roughly USD 120 million in 2020 to an estimated USD 291 million by 2032, reflecting a compound annual growth rate of 7.9% across the forecast horizon. Market concentration remains moderate: the three largest players control under half of the market, and the top five just over half — a structure that supports both competitive scale plays and value-creation opportunities for agile challengers.

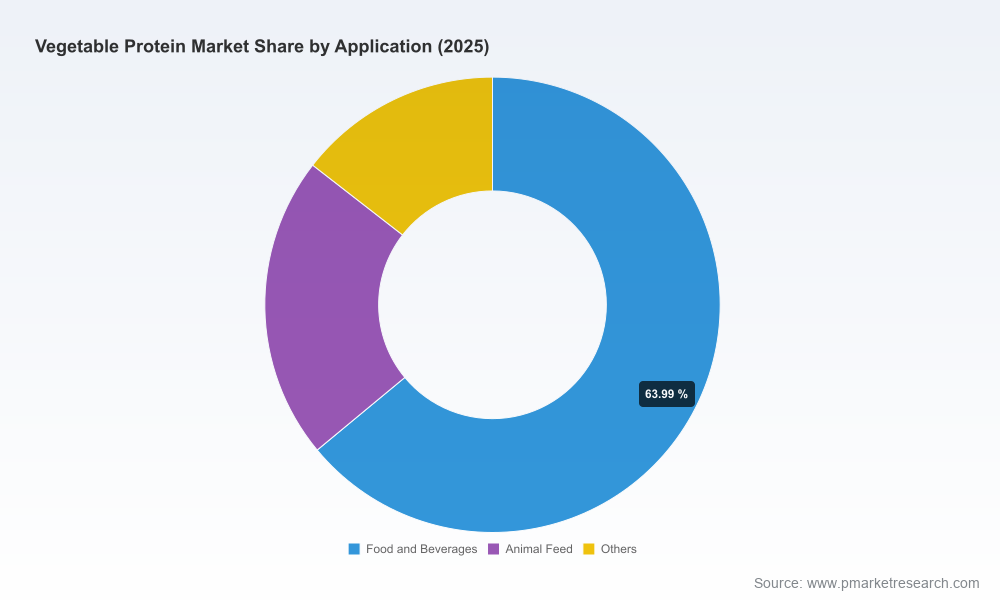

Vegetable Protein Market

This briefing explains the practical strategic value embedded in our full report for corporate decision-makers planning capital allocation, commercialization, and risk management in 2026. It highlights the dynamics shaping near-term supply, demand and regulation without disclosing the granular subsegment economics reserved for report subscribers.

Vegetable Protein Market

Growth tempo: A mid-single-digit-to-high-single-digit CAGR over the forecast period signals a market transitioning from niche to mainstream. For manufacturers and ingredient formulators, this implies a sustained window to scale production lines and invest in texture- and flavor-enabling technologies while securing raw-material feedstocks.

Vegetable Protein Market

Concentration and competition: With the top three firms holding a plurality (but not dominance) and the top five representing a little over half the market, there is room for strategic consolidation as well as for differentiated, premium offerings from specialists who can claim clean-label, regionally sourced, or functional differentiation.

Structural resilience: The market trajectory is fueled by simultaneous demand drivers—consumer health trends, dietary guidance shifts, and product innovation—creating a more resilient long-term demand base that reduces single-customer risk for ingredient suppliers.

Our report is designed as a decision-support toolkit for 2026 planning cycles. Its core deliverables include:

Interactive financial model with base, conservative and upside scenarios calibrated to input costs, raw-material availability and end-market adoption curves.

Supply‑chain heatmaps and tiered supplier scorecards that assess capacity, geographic exposure, and sustainability credentials — enabling precise sourcing decisions and contingency planning.

Product roadmaps and formulation playbooks that translate ingredient functionality into target use-cases (e.g., meat analogues, dairy alternatives, nutritional beverages), along with estimated cost-in-use and margin impact ranges.

Regulatory tracker and naming/allergen advisory tailored to key jurisdictions, including the latest guidance trends and probable near-term outcomes affecting labelling and market access.

M&A and partnership screening matrix that prioritizes targets by capability gaps (texturization, isolates, seed-to-extract integration), and includes a pre‑qualified list of candidates with indicative valuation bands.

Commercial playbooks for private-label food manufacturers, ingredient traders, and branded consumer goods companies focused on route-to-market choices, retailer engagement strategies, and co-manufacturing economics.

The vegetable protein ecosystem in 2026 is shaped by an interplay of policy, investment and product innovation. Several developments stand out as high-impact drivers for corporate strategies:

Policy and dietary guidance: New national dietary guidance and regulatory drafts that elevate plant-based proteins into mainstream protein categories are altering consumer expectations and procurement policies. Expect regulatory language around naming and allergen disclosure to influence product labelling, retailer assortment decisions and cross-border trade considerations.

Raw-material flows: Significant upstream investments and national crop strategies (including major policy initiatives to boost pulse cultivation) are changing feedstock availability and price correlations. These shifts present opportunities for integrated players and for companies that can secure long-term offtake or cultivate strategic sourcing partnerships.

Industrial capacity: Large-scale facility investments and network optimizations are altering production geographies and cost curves. New integrated facilities coming online and existing players consolidating operations will reshape logistics and fill-rate dynamics over the next 12–24 months.

R&D and product innovation: Advances in texturization, flavor masking, and seed-to-extract agronomy are making higher-protein, better-tasting applications commercially viable. Firms that combine ingredient science with sensory and regulatory know-how will be able to command premium positioning.

The competitive tableau is a mix of diversified agribusiness incumbents, ingredient-specialist firms, and nimble category disruptors. Key strategic archetypes observed in the market include integrated commodity suppliers, high-margin specialty ingredient innovators, and seed-to-extract technology providers. Representative examples and strategic moves observed through 2025–2026:

Roquette Frères: Leveraging a broad plant-protein portfolio, Roquette is pushing textured protein innovation to serve meat analogue and hearty application segments while emphasizing sustainable sourcing and EU-compatible supply chains. Recent product introductions underscore a playbook that pairs formulation-ready textures with low organoleptic impact.

Archer Daniels Midland (ADM): A classic scale player that is rationalizing its production footprint to drive utilization and lower unit costs. Strategic network consolidation and integration into downstream texturization capabilities indicate a focus on operational efficiency and customer service economics.

Cargill: Competing on ingredient breadth and application development, Cargill blends commodity processing strengths with targeted functional solutions for food, beverage and animal nutrition markets.

PURIS: A specialist pea-protein player emphasizing clean-label, non‑GMO credentials and innovation variants optimized for beverages and milk alternatives — a classic premium specialist strategy that targets formulators seeking superior sensory outcomes.

Protealis and seed-tech innovators: The emergence of seed-variety and biological-solution providers is creating vertical leverage opportunities for Europe-focused processors and extracting players seeking climate-resilient feedstocks and higher protein yield per hectare.

Diversified ingredient houses (Beneo, Ingredion, IFF, LDC): These groups are playing complementary roles — supplying functional oat- and starch-based protein concentrates, flavor and texture systems, and channel reach that supports rapid commercialization.

New textured and isolate launches from leading ingredient firms point to an arms race in sensorial performance and use-case fit — important for product teams looking to accelerate time-to-market for meat and dairy alternatives.

Large-scale greenfield and brownfield facility investments have expanded capacity in strategic geographies, compressing lead times but also creating potential overhang risk for suppliers that scale prematurely.

Regulatory draft guidance and national dietary shifts are making it easier for brands to market plant-based options — but they also introduce compliance complexity that requires active monitoring and scenario-based mitigation.

Procurement and sourcing: Lock in multi-year contracts with flexible volume triggers; diversify suppliers by crop and geography to hedge against localized weather, policy shifts, or export controls.

CapEx and footprint planning: Model both mid-case demand growth (supported by the projected CAGR) and downside scenarios driven by raw-material shocks. Prioritize modular, debottleneckable capacity investments that preserve optionality.

Product and R&D: Invest in texture and flavor platforms that lower sensory trade-offs—this is the fastest route to premiumization and higher price realization in competitive categories.

M&A and partnerships: Target bolt-on acquisitions that fill ingredient-function gaps (texturization, isolates, seed tech) or bring channel access; form offtake partnerships with upstream growers and seed innovators to secure differentiated feedstock economics.

Regulatory readiness: Integrate labeling and allergen advisory into product development lifecycles; build an internal regulatory watch that maps draft guidance to go-to-market decisions.

Our deep-dive is constructed to serve three critical decision needs in 2026: evidence-based capital allocation, commercially actionable product roadmaps, and mitigated regulatory risk. The full report delivers the granular, segment-level economics, competitive scorecards, and supplier-specific intelligence necessary to convert strategic options into executable plans. In keeping with our "trailer" approach, this public brief demonstrates the analytical depth and strategic framing you should expect — the actionable subsegment figures, supplier-level profiles and transaction‑ready valuation ranges are available in the full PW Consulting dossier.

Use the topline growth trajectory and concentration signals presented here to stress-test your 2026 budgets and investment approvals.

Prioritize a 90-day supplier and formulation audit to identify immediate low-cost wins in sourcing and product optimization.

Engage PW Consulting for a tailored workshop: we convert the report’s scenario outputs into an implementation roadmap — from capex sequencing to channel piloting and regulatory contingency plans.

For supply, demand, regulatory and competitive detail — including the segmented market economics and company-level playbooks not disclosed in this preview — consult the full Vegetable Protein Market report and modeling suite from PW Consulting. Our analysts are ready to support tailored strategic planning and transaction advisory work as you prepare to capture the growth window beginning in 2026.

For detailed analysis of this topic, please visit the official page:Vegetable Protein Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com