Diamond Saw Blades Market — Strategic Outlook for 2026 Decision‑Makers

As capital allocation cycles, procurement contracts, and product roadmaps are re‑set for 2026, PW Consulting’s latest Diamond Saw Blades Market research report provides the focused, decision‑grade intelligence executives need to act with conviction. Built on a 2020–2025 historical dataset and a 2026–2032 forecast horizon, the study calibrates near‑term operational choices against medium‑term structural trajectories. The market reached approximately USD 9 billion in our base year (2025) and — given the prevailing industry dynamics — is projected to expand at a compound annual growth rate (CAGR) of about 2.41% through the 2026–2032 forecasting window, approaching the low‑to‑mid tens of billions by the end of the period.

Diamond Saw Blades Market

Why this study matters for 2026 planning

- Decision relevance: Supply chain managers, product executives, and corporate development teams are making commitments in 2026 whose impacts will last well into the next planning cycle. Our report converts macro momentum into executable options — from sourcing strategies to M&A targets.

- Actionable lens: Rather than a brochure of high‑level trends, the report delivers scenario models, supplier risk heatmaps, and tactical playbooks calibrated to 2026 market conditions.

- Time sensitivity: Several industry shifts announced or unfolding in late 2025 and early 2026 materially alter near‑term supplier capacity and channel economics — creating windows for strategic moves and vulnerabilities that require rapid assessment.

Core dynamics reshaping the market

- Demand fundamentals: After steady recovery through the early 2020s, the market expanded to roughly USD 9 billion in 2025. The next phase is characterized by moderate overall growth, with pockets of accelerated adoption driven by precision cutting needs in masonry, concrete and industrial metal processing.

- Technology & productivity: Labor shortages in construction and industrial sectors combined with energy‑efficiency mandates are accelerating the shift toward precision diamond solutions that reduce rework, lower energy use and enable automation. Suppliers that can demonstrate blade life gains, lower total cost of ownership, and compatibility with automated cutting systems will capture disproportionate share growth.

- Raw material & supply chain friction: Synthetic diamonds remain the dominant abrasive input. Recent customs and regulatory developments have highlighted concentrated sourcing geographies, requiring firms to evaluate supplier diversification, traceability, and inventory buffers as part of 2026 procurement strategy.

- Competitive fragmentation: Market concentration metrics show the landscape remains fragmented — a small cluster of global incumbents coexists with many specialized and regional suppliers. This fragmented structure creates opportunities for consolidation, vertical integration (into core bits, blades, and services), and niche specialization.

- Regulatory and operational safety: Newer guidance on mounting, use, and maintenance (including formalized manufacturer do’s & don’ts) is increasing the importance of after‑sale training and warranty strategy as differentiators — especially for higher‑value, industrial blades.

- Corporate portfolio adjustments: Strategic exits and portfolio rationalizations by legacy OEMs are re‑shaping capacity maps. Notably, planned discontinuations of non‑core stone tool lines by large groups will create both short‑term supply dislocations and strategic acquisition opportunities through 2026.

What the full report contains — practical, implementable modules

- Market sizing and trend engine: Rolling historical dataset (2020–2025) and scenario‑driven forecasts to 2032, with base‑case, upside and downside paths tied to macro and regulatory permutations.

- Supplier & capacity heatmaps: Facility footprints, technology capabilities (e.g., laser welding, segment metallurgy), and supplier risk indices to prioritize dual‑sourcing and inventory hedging.

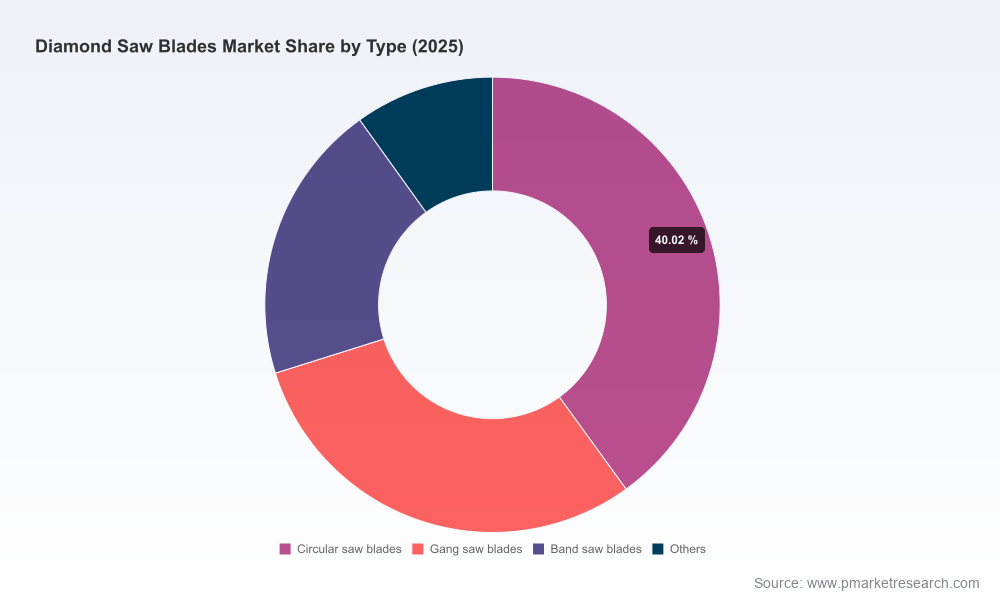

- Demand segmentation playbooks: Actionable insights by end‑use and customer archetype to inform pricing, SKU rationalization, and channel strategy. (Note: detailed segment allocations and numeric splits are reserved for subscribers of the full report.)

- Competitive strategy profiles: Comparative diagnostics across product, distribution and innovation vectors to identify likely winners and vulnerable propositions in 2026.

- M&A origination lists and valuation yardsticks: Target shortlists, estimated synergy levers, and regulatory red flags for roll‑up strategies in a moderately fragmented market.

- Procurement & manufacturing checklist: Tactical steps for mitigating synthetic diamond sourcing risk, optimizing bond formulations for energy‑efficiency mandates, and evaluating capital investments in automated brazing or laser welding equipment.

- Go‑to‑market and aftermarket modules: Field service economics, extended warranty modeling, and B2B content strategies that convert safety and performance advisories into win rates.

Competitive landscape — what incumbents and challengers signal for 2026

The market comprises a mix of established global manufacturers, regional specialists and direct‑to‑market retailers. Key interpretations for 2026 strategy include:

Diamond Saw Blades Market

- Value specialization by legacy leaders: Companies with deep construction and industrial portfolios continue to lead on brand and distribution. Their focus is on premium wet/dry product lines and multifunctional blades for concrete, stone and asphalt — an approach that defends margins but leaves niches open to focused competitors.

- Channel & service differentiation: Several direct retailers and wholesalers are leveraging content, tutorials and performance reviews to build trust and recurring revenue. Expect differentiated aftermarket services and bundled consumables to become more prominent as revenue diversifiers.

- Manufacturing and tech node competition: Firms that have invested in automated welding, segment metallurgy R&D, and in‑house synthetic diamond qualification gain both quality and cost advantages. Suppliers promoting ISO‑certified production and advanced joining techniques will be preferred by industrial customers prioritizing reliability.

- Strategic exits and portfolio realignment: Announced intent by major players to discontinue non‑core stone tool operations will reallocate manufacturing capacity; agile competitors and private equity sponsors should watch for attractive bolt‑on assets or capacity purchase opportunities.

- Regional playbooks: While demand drivers differ by construction cycle and industrial activity, the strategic imperative remains consistent — align product architecture to automation trends and energy regulations to capture higher‑value contracts.

Recent market signals to monitor closely in 2026

- Trade show and product cadence: Increased exhibitor activity and catalog refreshes across major industry events signal competitive product launches and marketing investments that will influence buying patterns throughout 2026.

- Sourcing rulings & origin transparency: Customs rulings and supply declarations affecting synthetic diamond origins have practical implications for compliance, lead times and supplier selection—integrate legal review into supplier onboarding.

- Public product trials and reviews: Retailers publishing comparative reviews and application tutorials are accelerating end‑user selection cycles; OEMs must balance technical claims with verifiable test data to avoid reputational risk.

Recommended strategic plays for 2026

- De‑risk the diamond supply chain now: Establish dual‑sourced contracts, qualify alternate synthetic diamond suppliers across geographies, and secure safety stocks tied to production lead‑times.

- Prioritize product lines aligned with automation and energy efficiency: Reposition R&D and marketing to emphasize lifetime cost, compatibility with automated cutters, and energy consumption per linear meter cut.

- Advance aftermarket and services: Convert safety guidance and mounting best practices into monetizable training, certification and premium support programs for commercial customers.

- Act on consolidation selectively: Use the market’s fragmentation to acquire capacity or market access from divesting incumbents, focusing on assets with complementary technology or channel reach.

- Invest in manufacturing agility: Evaluate capital deployment into laser welding, segment metallurgy labs, and small‑batch production capabilities to quickly adapt to changing bond and segment formulations.

- Align commercial strategy to channel evolution: Strengthen relationships with professional wholesalers, rental fleets and OEMs; leverage content and performance certification to win specification decisions.

Conclusion — how to use the report in boardroom deliberations

For 2026, the right moves are both tactical (supplier contracts, inventory policy) and strategic (portfolio tilt, M&A). PW Consulting’s Diamond Saw Blades Market report translates the market’s USD 9 billion base (2025) and the modest multi‑year growth trajectory (CAGR ~2.41% across 2026–2032) into prioritized actions, risk matrices, and a short list of value capture plays. We deliberately preserve granular segment-level allocations in the full subscriber pack to ensure our clients receive exclusive competitive intelligence that can be operationalized immediately.

Diamond Saw Blades Market

If your 2026 plan involves procurement, product development, or inorganic growth in the diamond cutting ecosystem, the full report will save you months of research and reduce execution risk. Visit PW Consulting to access the complete dataset, scenario models, and the supplier heatmap essential for decisive action this year.

For detailed analysis of this topic, please visit the official page:Diamond Saw Blades Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com