Reliable Solutions for Every Home: Finding the Right Plumbing Experts

Other |

2026-04-30 03:06:41

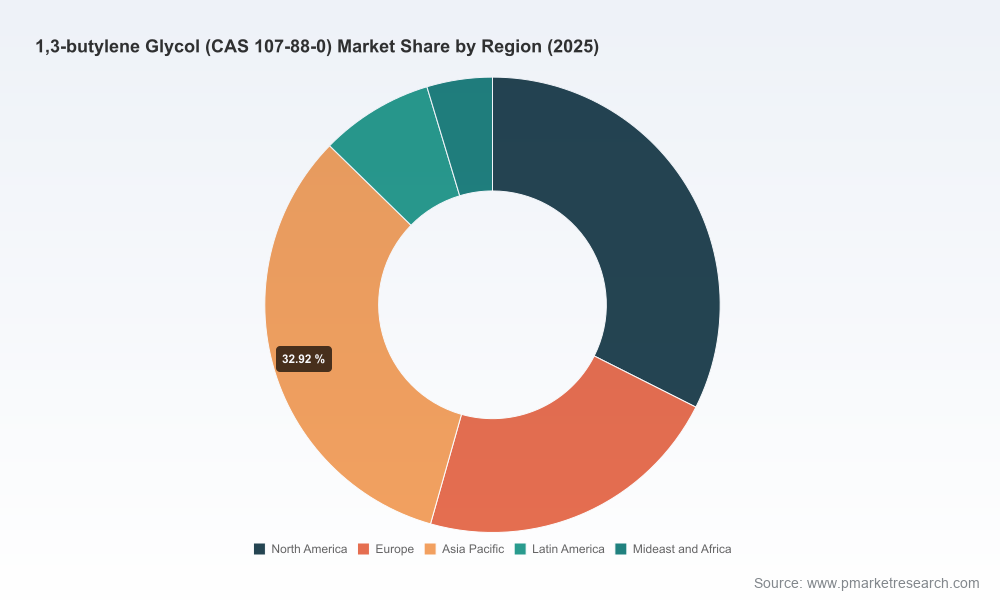

PW Consulting’s new market study on 1,3-butylene glycol (1,3-BG) delivers a focused, decision-grade perspective for executives planning investment, sourcing, and product strategy in 2026. The global market has demonstrated resilient expansion from the early-2020s and reached an estimated USD 212.52 Million in 2025. Our baseline forecast shows continued momentum — the market is projected to grow at a compound annual growth rate (CAGR) of 5.9% through the 2026–2032 forecast window, reaching an expected USD 321.67 Million by 2032. This trajectory hides important inflection points and supply-side dynamics that will determine winners and laggards over the next investment cycle.

1,3-butylene Glycol (CAS 107-88-0) Market

Actionable forecasts for portfolio allocation: the report reconciles demand drivers across personal care, pharmaceutical intermediates, and industrial uses with supplier capacity and raw-material exposures — enabling CFOs and strategy teams to allocate capital with scenario-based ROI estimates.

1,3-butylene Glycol (CAS 107-88-0) Market

Risk-first supply planning: given feedstock volatility and certification-driven demand for bio-derived inputs, procurement leaders can use our supply-side stress tests and supplier scorecards to construct resilient multi-sourcing strategies.

1,3-butylene Glycol (CAS 107-88-0) Market

M&A and partnership screening: corporate development teams receive a short-listing framework and financial sensitivity templates to evaluate bolt-on acquisitions, joint ventures, and tolling arrangements without overpaying into a concentrated supply base.

Market model and forecast engine: a transparent, model-backed forecast from 2026–2032 with scenario toggles for feedstock price shocks, regulatory shifts, and accelerated bio-adoption. The model is delivered in an Excel workbook so clients can re-run assumptions against their internal KPIs.

Demand-by-use-case playbooks: commercial briefs that translate macro demand into product and formulation levers for personal care formulators, pharmaceutical suppliers, and industrial intermediates teams — including go-to-market tactics and price-elasticity benchmarks.

Supplier and capacity intelligence: company profiles, operational footprints, recent CAPEX/debottleneck events, and a risk rating (technical, regulatory, logistical) for every active supplier. This section supports sourcing decisions and offtake negotiations.

Raw-material sensitivity and margin maps: inputs-level analysis comparing bio-based (sugarcane fermentation) vs synthetic (butadiene-derived) routes, with break-even curves showing the feedstock price bands where each route is advantaged.

Regulatory and certification matrix: a concise guide to COSMOS, NATRUE, REACH, TSCA and voluntary programs such as the U.S. EPA Safer Choice — with checklists and expected timelines for registration or certification to inform market-entry timing.

Commercial diligence attachments: primary-interview insights, sample offtake agreement clauses, and a supplier negotiation playbook calibrated to current concentration dynamics and recent corporate moves.

End-market compositional shifts: growth in value-added personal care formulations and pharmaceutical intermediates is increasing demand for higher-purity 1,3-BG grades. At the same time, industrial applications continue to anchor baseline consumption.

Certification and sustainability: voluntary natural-origin certifications (COSMOS, NATRUE) and eco-labeling programs are driving formulators to prefer bio-derived 1,3-BG for premium product tiers. This creates a price premium and separate competitive track for bio-based producers.

Feedstock volatility: synthetic production remains exposed to butadiene and downstream petrochemical market cycles, while bio-based production is dependent on agricultural feedstock supply (notably sugarcane) and its seasonality — a structural source of short-term price swings.

Regulatory overheads: cross-border commerce is influenced by REACH and TSCA registration costs and timelines, which raise entry barriers for smaller suppliers and create commercial advantage for incumbents with established regulatory compliance footprints.

The market remains commercially concentrated around a relatively small set of global producers and specialized distributors. Our report includes in-depth profiles of leading players, including operational summaries, strategic posture, and risk assessments. Notable participants covered in the study include:

OXEA GmbH (Oberhausen, Germany) — integrated manufacturer supplying industrial and cosmetic grades for personal care, food, and pharmaceutical uses.

Daicel Corporation (Osaka, Japan) — a major producer of both bio-based and synthetic 1,3-BG with multi-tens-of-thousands of tonnes-per-year capacity and a strong focus on sustainable product lines.

Godavari Biorefineries Ltd. (Hyderabad, India) — specializes in bio-derived 1,3-BG produced via renewable sugarcane fermentation, focused on humectant and emollient markets.

Penta Manufacturing Company (New York, United States) — supplier of FCC and NF grades targeting pharmaceutical intermediates and food-grade applications.

MMP Inc. (United States), Shanghai Jinjin Industry Co., Ltd. (Shanghai, China), KH Neochem Co., Ltd. (Japan), Whyte Chemicals Limited (UK), and Rita Corporation (United States) — distributor and specialty manufacturer roles that support regional demand and formulation supply chains.

Strategic reviews and portfolio optimization — Daicel Corporation initiated a business-plan review in early 2026 that included its 1,3-BG operations, a signal that incumbents are re-evaluating capacity alignment with long-term demand.

Capacity debottlenecking — Godavari Biorefineries completed capacity debottlenecking in 2025 to expand throughput and capture higher-margin bio-derived demand; such operational tweaks are becoming more common as producers chase premium bio-certified segments.

Regulatory recognitions — public programs such as the U.S. EPA’s Safer Choice have begun to explicitly recognize 1,3-BG as a safer option for some personal care applications, creating marketing and formulation advantages for compliant suppliers.

Procurement: Implement a two-track sourcing playbook. Secure strategic long-term supply from qualified incumbents while developing tertiary supply relationships with certified bio-based producers to manage certification-led demand spikes.

Product and portfolio: Accelerate formulation work to productize bio-certified grades for premium personal care customers. Capture margin expansion through higher-value positioning rather than volume-only competition.

Capex and operations: Favor modular debottlenecking and tolling arrangements over large greenfield builds unless long-term guarantees or feedstock-integrated models are in place. Our sensitivity analysis shows faster payback under capacity debottlenecking with flexible feedstock sourcing.

M&A and partnerships: Use our screening criteria to pursue bolt-ons that add certification capabilities, backward-integrated feedstock access, or regional regulatory compliance presence. Prioritize targets that close the gap between current capabilities and premium bio-certified product demand.

Regulatory readiness: Build a compliance roadmap for REACH/TSCA registration and voluntary certifications; costs and lead times are predictable inputs that should be built into go-to-market timing and customer commitments.

Commercial: Negotiate offtake contracts with indexed pricing and flexible volume commitments to share feedstock volatility risk. Use supplier scorecards to allocate volumes to partners with demonstrated reliability and regulatory completeness.

A downloadable forecasting workbook with scenario toggles and sensitivity charts so teams can stress-test outcomes against internal budgets.

Supplier scorecards with qualitative and quantitative ratings (technical, financial, regulatory, logistics), red-teams for supply disruption scenarios, and a recommended shortlist for primary sourcing.

Commercial playbooks (pricing, contract clauses, certification timelines) and an M&A checklist that translates market dynamics into minimum acceptable returns and integration risks.

Primary-sourced intelligence: excerpts from interviews with plant managers, procurement heads, and formulators to ground model assumptions in market reality.

As the 1,3-BG market moves from recovery into a structurally higher growth path (5.9% CAGR through 2032), strategy and execution will separate market leaders from followers. The combination of certification-driven premium demand, feedstock-linked cost volatility, and a concentrated supply base requires a disciplined, data-driven approach to sourcing, capacity, and product strategy. PW Consulting’s report equips 2026 decision-makers with the practical tools, supply-side intelligence, and scenario frameworks necessary to convert market growth into sustainable commercial advantage.

To access the full dataset, supplier scorecards, and the interactive forecast workbook, please visit our report page or contact PW Consulting’s industry practice for a tailored briefing and licensing options.

For detailed analysis of this topic, please visit the official page:1,3-butylene Glycol (CAS 107-88-0) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com