PW Consulting: Strategic Brief — 3D Laser Scanners Market Outlook 2026 (Executive Trailer)

PW Consulting today releases an executive trailer for our forthcoming in-depth market research report on the 3D laser scanners market, built to inform executive decisions entering 2026. This brief synthesizes the market’s trajectory, competitive forces, regulatory inflection points, and recommended strategic actions—while preserving the granular segmentation and forecast tables for subscribers and clients. The full dataset, vendor scorecards, and modelled scenarios are available on the report landing page.

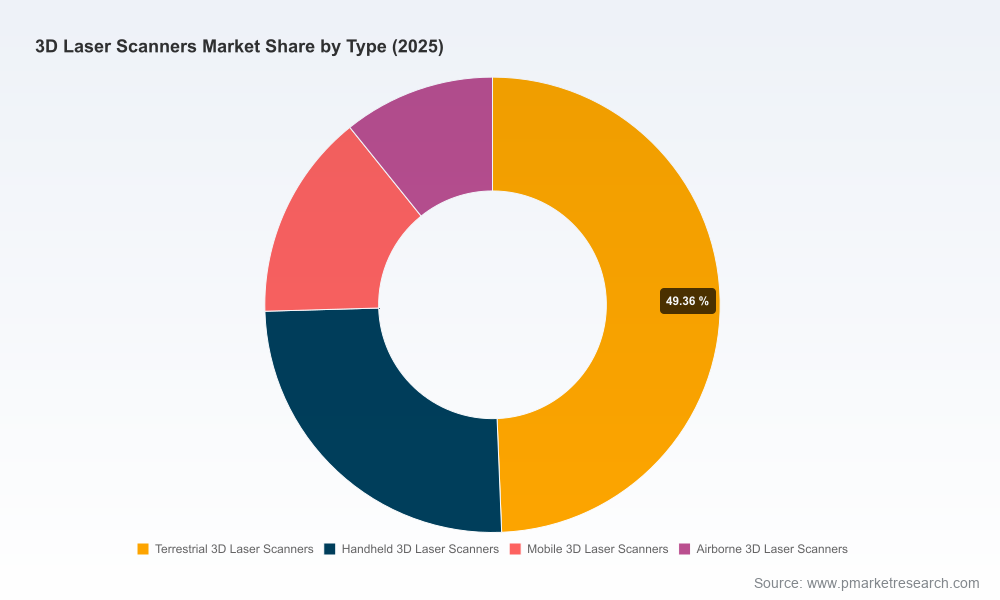

3D Laser Scanners Market

Why this market matters for 2026 decision-makers

3D laser scanning has moved from a niche measurement tool to a mission‑critical element across surveying, construction, manufacturing metrology, forensics, and digital preservation. Our base-year is 2025: the market reached a substantive mid‑hundred‑million USD scale in 2025 and is forecast to expand materially through the next planning cycle. Over the 2026–2032 forecast horizon the market is projected to grow at a compound annual growth rate (CAGR) of 6.98%, reaching roughly USD 346 million by 2032. That growth profile underlines a window of commercial opportunity in hardware, software ecosystems, services, and adjacent analytics.

3D Laser Scanners Market

What the PW Consulting report delivers (practical, actionable elements)

- Proprietary market sizing and seven-year forecasts (2026–2032) with sensitivity scenarios tuned to adoption curves and pricing dynamics.

- Vendor benchmarking and scorecards that evaluate product families across accuracy, throughput, certification, integration APIs, and total cost of ownership.

- Go-to-market playbooks for OEMs, distributors, and systems integrators emphasizing channel structures, bundling strategies (hardware + software + services), and subscription models.

- Case studies and ROI calculators for five major end-use verticals illustrating break-even timelines under different labor and data-processing cost assumptions.

- Regulatory and standards annex detailing compliance pathways for the latest metrology and forensic capture standards, plus an audit checklist for accreditation readiness.

- Technology roadmap appendix covering sensor fusion (LiDAR + photogrammetry), edge processing, mobile mapping integrations, and firmware/security lifecycle considerations.

While this trailer highlights core insights, readers seeking the full model inputs, subsegment revenue breakdowns, and vendor-level forecasts should consult the full report. Access details are provided at the end of this brief.

3D Laser Scanners Market

Market dynamics shaping 2026 choices

- Steady, predictable growth: A near-7% CAGR frames a market that favors disciplined investment—incremental product improvements and software-enabled differentiation will compound value over time.

- Fragmentation with consolidation potential: The market concentration ratios indicate a fragmented competitive landscape where a modest share sits with established leaders while numerous specialized vendors compete on accuracy, portability, and price-performance. This environment favors strategic alliances, white-label partnerships, and bolt-on acquisitions to scale distribution and R&D efficiently.

- Standards and traceability: Adoption of metrology and forensic capture standards is accelerating procurement requirements. Recent and active standards—including newly relevant guidance for forensic LiDAR capture and updated acceptance tests for handheld coordinate systems—are shifting procurement toward vendors who can demonstrate traceable calibration and accredited testing.

- Cost structure sensitivity: Project labour intensity (data capture and post-processing) remains a principal driver of total project cost. Automation of registration, AI-assisted cleaning, and edge pre-processing are key levers to reduce marginal costs and enable higher-margin service offerings.

Competitive landscape — what to watch in 2026

The vendor environment blends incumbent metrology specialists, long-established surveying brands, and aggressive entrants from Asia. Recent product and firmware activity demonstrates the market’s focus on improved metrological traceability, portability, and operational robustness.

- Creaform (Canada): Reinforces its portable handheld portfolio with metrology-grade additions and expanded certification claims. This positions them well for inspection and reverse-engineering workflows that demand ISO‑level traceability.

- Artec 3D (Luxembourg): Recent device refreshes emphasize optics and measurement stability with updated metrology certifications—an explicit play to capture quality-focused portable scanning segments.

- FARO Technologies (USA): Continues to iterate on firmware and processing pipelines for its mid-to-high-end scanners, signaling a focus on lifecycle maintenance, backward compatibility, and field reliability.

- Hexagon, Leica Geosystems, Trimble, RIEGL, Topcon: These incumbents continue to strengthen integrated terrestrial and surveying solutions, leveraging installed bases and enterprise contracts for construction, infrastructure, and large‑scale documentation projects.

- China-based entrants (e.g., SHINING 3D, SCANOLOGY, 3DMakerpro, Revopoint): Compete on accessible price-performance and are rapidly closing the gap on calibration credentials through accredited labs and ISO/IEC certifications. Their strategies focus on expanding addressable markets via prosumer-to-industrial tiers.

Strategic takeaway: incumbents that combine certified accuracy, field usability, and robust software ecosystems retain bargaining power with enterprise buyers. Aggressive entrants disrupt the lower tiers and force incumbents to defend share with bundled services and certification-backed claims.

Standards, regulation, and procurement implications

- OSAC guidance for forensic LiDAR capture has implications for public-sector procurements and law-enforcement agencies; vendors and integrators must present compliant workflows to be considered for such contracts.

- ISO 10360-13 and ISO 17123-9 remain central to acceptance testing and re-verification; organizations pursuing metrology-grade outcomes should require traceability evidence to accredited labs.

- VDI/VDE metrology recommendations and ISO/IEC 17025 accreditation are emerging as differentiators in tender evaluation—especially where legal defensibility or precision inspection is required.

Technology & commercial plays for 2026

We recommend organizations consider the following strategic options depending on role and appetite:

- For OEMs and hardware vendors: Prioritize certification and partner with accredited calibration labs. Invest in robust firmware and SDKs to lock-in software partners and systems integrators. Consider modular product lines that allow customers to scale from handheld to terrestrial systems within a unified platform.

- For software and analytics providers: Differentiate on post-processing automation, AI-assisted noise reduction, and cloud-native pipelines that reduce on-premise labour. Integration with mainstream CAD/BIM and GIS tools is table stakes.

- For integrators and service providers: Build verticalized offerings (e.g., forensics, cultural heritage, manufacturing QA) that combine certified capture processes, SLA-backed deliverables, and outcome-based pricing to mitigate project cost sensitivity driven by labour.

- For investors and M&A teams: Target assets that provide accredited calibration, unique IP in registration/automation, or complementary software stacks that can accelerate margin expansion across services.

Near-term tactical checklist for purchasers (2026 planning)

- Require demonstrable compliance with applicable metrology and capture standards in RFPs.

- Factor in firmware support and calibration cadence when total-costing devices—initial hardware price is not the primary determinant of lifetime expense.

- Run pilot projects that stress both capture and post-processing workflows to validate labour and throughput assumptions.

- Evaluate vendors’ roadmaps for sensor fusion and edge processing to future-proof procurement decisions for integrated mapping and BIM use cases.

Regulatory & operational risk radar

Compliance with updated standards and accreditation processes is both a cost and a market access requirement. Non-compliant offerings face procurement exclusion in regulated segments such as forensics and high-precision inspection. Additionally, labour and data-processing bottlenecks can erode project margins if not addressed through automation and optimized workflows.

Concluding advisory — how PW Consulting supports your 2026 strategy

Our full 3D Laser Scanners Market report (base-year 2025) provides the complete financial models, scenario analyses, and vendor-level forecasts required to make capital allocation, procurement, and partnership decisions for 2026 and beyond. We couple quantitative forecasts (market trajectory to 2032 at a 6.98% CAGR) with practical, implementable playbooks and a standards-compliance annex to accelerate time to value.

For strategic briefings, custom vendor benchmarking, or to obtain the full dataset and model inputs (including subsegment detail and regional application breakdowns reserved for subscribers), please visit the PW Consulting report page or contact our industry team to schedule a tailored executive session.

For detailed analysis of this topic, please visit the official page:3D Laser Scanners Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com