Emmental Cheese Market Dynamics: Key Drivers and Restraints

Other |

2026-06-12 07:34:27

PW Consulting today releases a forward-looking briefing derived from our full Polyetheretherketone (PEEK) Market report — a practical, decision-oriented companion for corporate leaders planning capital allocation, supply-chain moves, and product strategy in 2026. Built on a detailed historical review (2020–2025) and scenario forecasts through 2032, this briefing highlights the strategic implications of today’s material, regulatory and competitive shifts while intentionally withholding granular segment tables to encourage direct engagement with the full report.

Polyetheretherketone (PEEK) Market

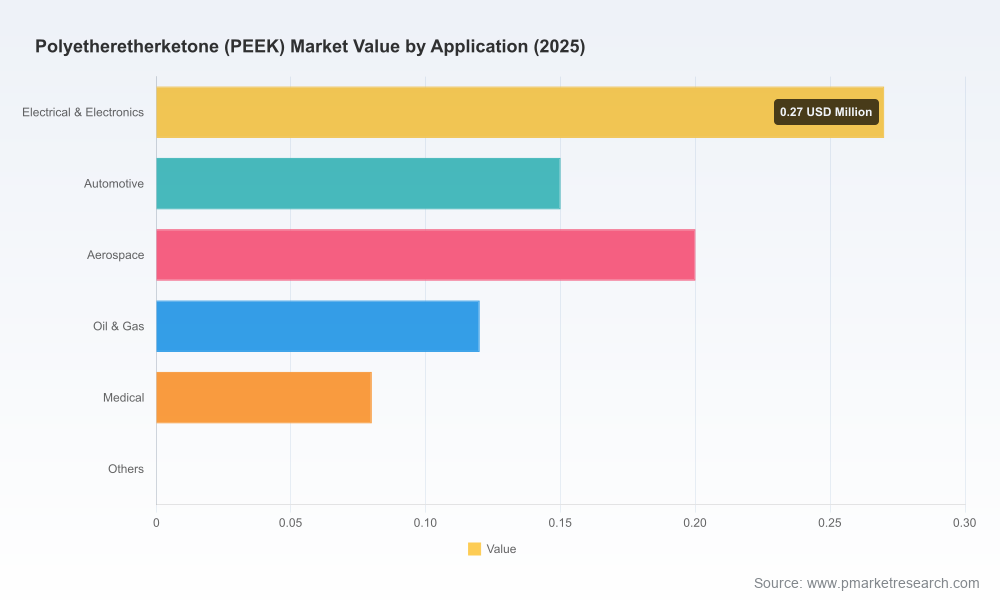

PEEK remains one of the fastest-moving niches within the high-performance polymer space. Using 2025 as our base year, PW Consulting’s market model shows an uninterrupted expansion from the 2020 baseline into the forecast window (2026–2032), driven by structural demand in aerospace, medical and high-end electronics, together with widening industrial adoption where lifetime cost and thermal performance trump commodity polymers.

Polyetheretherketone (PEEK) Market

Historical and base-year framing: our analysis covers 2020–2025 with 2025 as the base reference for all scenarios.

Polyetheretherketone (PEEK) Market

Mid-term growth: the market is projected to continue expanding through 2032 under a central scenario that assumes continued technology diffusion and steady recovery in capital-intensive end markets. Our central forecast implies a compound annual growth rate (CAGR) of approximately 6.3% over the forecast period.

Market concentration: the global PEEK sector remains moderately concentrated at the top—three firms account for a clear majority share and the top five firms consolidate roughly three quarters of market revenues—creating a supplier landscape where scale and integration confer measurable advantages on pricing, raw-material security and new-grade development.

PW Consulting designed the full report as a working toolkit for senior decision makers. Beyond topline numbers and forecasts, the deliverables include:

Decision-ready supplier and capacity maps, including scenario-based supply continuity plans and a supplier risk heatmap that links precursor markets to finished PEEK availability.

Go-to-market playbooks tailored to corporate roles—procurement, product management, R&D and business development—detailing contracting structures, inventory tactics and technical validation roadmaps for component qualification.

Process and cost benchmarkers: manufacturing- and processing-focused benchmarks that align polymer grade selection with injection molding, extrusion and additive manufacturing process windows.

Technology adoption frameworks: readiness assessments for emerging grades (including lower-melting PAEK-like derivatives), additive manufacturing integration, and composite substitution matrices for aerospace and transportation programs.

M&A and partnership playbooks: strategic criteria and financial scorecards for bolt-on acquisitions, capacity leases and long-term supply commitments in a concentrated supplier market.

Regulatory & sustainability checklists, including PFAS-related positioning, medical implant compliance pathways and end-of-life considerations for high-performance thermoplastics.

A set of interlocking dynamics will determine winners and losers in the next 12–36 months. The full report layers quantitative sensitivity testing on these dynamics; the headline forces are:

Raw-material and vertical integration pressure: security of feedstock for the 4,4’-DFBP precursor remains a decisive factor. Players with upstream integration or long-term precursor agreements can better buffer feedstock volatility and preserve margin during tight supply cycles.

Product innovation lowering production barriers: new low-melting PAEK-like grades and PEEK variants with wider processing windows materially reduce manufacturing complexity for high-temperature polymers. These innovations—now commercialized by leading firms—improve yield and reduce capital investment requirements for processors, accelerating adoption in traditionally cost-sensitive segments.

Sustainability and regulatory clarity: PEEK’s status as PFAS-free in unfilled polymer manufacture provides a differentiator for OEMs under regulatory and customer scrutiny. This attribute is increasingly important in medical and electronics programs where material declarations factor into procurement decisions.

Geopolitical and regional capacity shifts: capacity expansions in Asia—particularly China—are re-shaping the cost base and shortening lead times for regional markets. Our broader analysis highlights both the commercial benefits of proximity and the strategic risks of single-region dependence.

The market is led by a mix of incumbent multinational producers, specialist compounders and regional-scale manufacturers. PW Consulting’s competitive analysis combines publicly available disclosures, recent product launches and capacity moves to assess strategic positioning:

Victrex plc (UK): a recognized technology leader with a strong history in high-performance PEEK and PAEK solutions. Recent launches of lower-melting PAEK variants and partnerships in additive manufacturing underline a dual strategy—sustain leadership through grade innovation while building ecosystem advantages with AM partners. Their product and application focus positions them to capture aerospace and energy program wins where qualification cycles are longer but margins higher.

Solvay S.A. (Belgium): a producer with deep strength in high-temperature grades and medical applications. Recent launches targeting enhanced biocompatibility and radiolucency signal a deliberate push into advanced medical implants and instrumentation markets where regulatory differentiation matters.

Evonik Industries AG (Germany): notable for downstream compounding and expanding compounding footprints in Asia. Their strengths lie in tailored compound solutions and supply proximity to regional OEMs, which translates into shorter qualification times for industrial customers.

Arkema S.A. (France): positions itself through complementary high-performance ketone polymers (PEKK/PAEK family) and a strong focus on additive manufacturing applications, useful for OEMs seeking broader design flexibility.

China-based players and regional specialists: manufacturers focused on medical-grade resins, pellets and powders have scaled rapidly. Their rise is altering sourcing conversations around cost, lead time and qualification pathways—especially for producers of semi-finished and finished profiles.

Compounding & semi-finished specialists (e.g., RTP Company, Ensinger): critical partners for development teams needing custom-filled grades, semi-finished shapes and short-run production support. Their role in the value chain is growing as OEMs seek to reduce time-to-market while minimizing capital exposure.

Notable recent industry moves—new grade announcements and additive-manufacturing partnerships by incumbent leaders—underscore an industry pivot: advancing material performance while simplifying manufacturability to broaden PEEK end-markets.

For corporate leadership aligning budgets and strategies in 2026, PW Consulting’s prioritized recommendations are tactical and immediate:

Procurement & Sourcing: institute a two-tier sourcing policy that combines a strategic long-term agreement with a primary supplier (to secure capacity and R&D cooperation) and secondary regional partners for resilience. Include feedstock hedging clauses where feasible.

R&D & Product: evaluate low-melting PAEK-type grades in parallel trials with incumbent PEEK grades to quantify lifecycle cost savings from processing efficiency. Target proof-of-concept runs that replicate expected end-use environments rather than laboratory-only characterization.

Manufacturing & Operations: invest in training and minor capital adaptions to make existing processing lines compatible with new-grade processing windows; this is often lower-cost than full line replacement and accelerates adoption.

Commercial & Go-to-Market: reposition value propositions around lifecycle economics, regulatory clarity (PFAS profile) and qualification support for high-value OEM verticals. Use ensured supply and design-for-manufacture services as premium differentiators.

M&A & Partnerships: prioritize transactions that provide either immediate capacity access in strategic regions or complementary downstream capabilities (compounding, semi-finished shapes, AM partnerships).

Risk & Compliance: incorporate material-declaration protocols into customer-facing documentation and pursue certifications relevant to medical and aerospace paths early in program timelines.

Decisions made in 2026 will lock in cost and qualification pathways for multi-year product programs across aerospace, medical and electronics sectors. PW Consulting’s PEEK report converts market and technology trends into executable strategies: it moves beyond “who did what” to provide the supplier scorecards, processing benchmarks and scenario-tested financial models that procurement, R&D and corporate development teams need to act with confidence.

To preserve the report’s role as a strategic instrument, we have presented high-level findings here while omitting detailed segmentation tables and line-item forecasts. Those granular datasets—regional and application-level splits, supplier-specific capacity maps and downloadable financial models—are available only in the full report and accompanying data package.

For executives ready to operationalize the insights or to request a tailored briefing for your board, procurement or engineering teams, please contact PW Consulting or visit our website to download the full PEEK Market report and the supplementary decision toolkit.

For detailed analysis of this topic, please visit the official page:Polyetheretherketone (PEEK) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com