Global Peritoneal Dialysis Drainage Bag Market Growing at 6.6% CAGR

Other |

2026-06-05 11:20:10

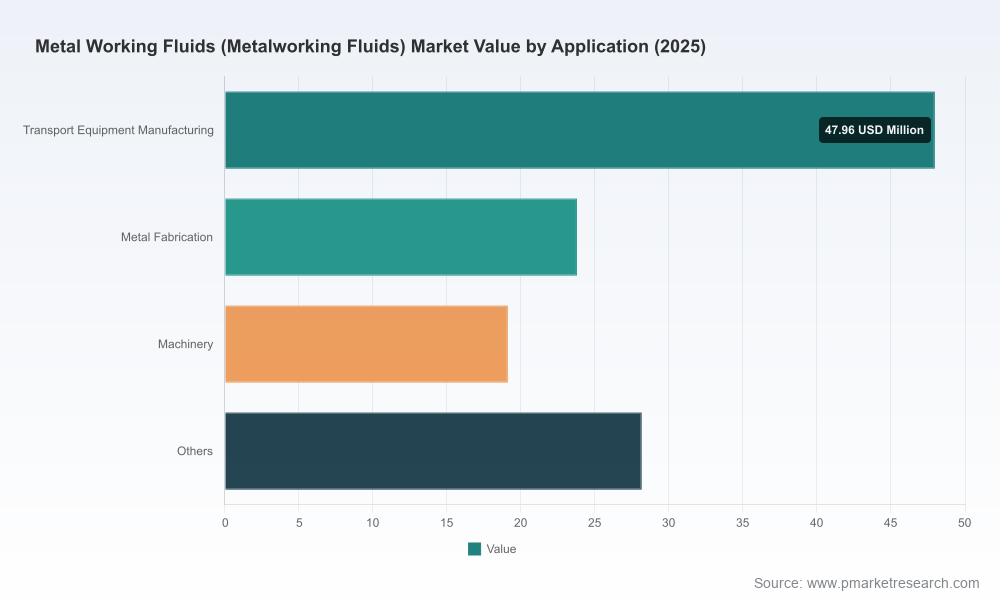

As manufacturers, suppliers, and investors reset priorities for 2026, PW Consulting’s latest Metalworking Fluids (MWF) market study delivers a focused strategic compass. Built on a five‑year historical base (2020–2025) with 2025 as the base year and a forward forecast to 2032, the report tracks an industry that has expanded steadily — from roughly USD 95 million in 2020 to about USD 119 million in 2025 — and is projected to grow at a compound annual growth rate (CAGR) of 4.8% through 2032. These headline numbers frame an industry that is neither hyper‑consolidated nor fragmented: our concentration metrics show the top three players control roughly one‑third of the market and the top five about mid‑forties percent, creating space for both global champions and regional specialists to capture value.

Metal Working Fluids (Metalworking Fluids) Market

Actionable foresight for capital allocation: with moderate, predictable growth and identifiable inflection points driven by regulation and feedstock risk, our report translates macro forecasts into capital allocation scenarios for R&D, capacity expansion, and M&A prioritization.

Metal Working Fluids (Metalworking Fluids) Market

Risk‑calibrated procurement strategies: a base oil supply disruption expected to intensify in 2026 materially changes supplier bargaining power and inventory policy. We provide procurement levers and supplier risk scoring templates to de‑risk short‑term exposure while positioning for long‑term cost competitiveness.

Metal Working Fluids (Metalworking Fluids) Market

Regulatory readiness as a competitive advantage: evolving restrictions on VOCs, formaldehyde, chlorinated paraffins and heightened PFAS scrutiny are already influencing product roadmaps. Companies that operationalize compliance into product development and customer service capture premium positioning—this brief outlines the regulatory pathways and pragmatic responses.

Customer & application migration playbooks: as aerospace, automotive, and precision manufacturing sectors demand higher performance and lower environmental impact, we map practical go‑to‑market plays for suppliers to move up the value chain without eroding margins.

Decision‑grade market model: a transparent, auditable financial model that converts the report’s top‑line trajectory into demand scenarios by end‑use clusters and product classes (note: core subsegment tables are accessible in the full report to preserve proprietary analytic value).

Procurement & supply‑chain playbook: supplier scorecards, dual‑sourcing templates, and an inventory hedging guide tied to base‑oil shock scenarios to protect production continuity in 2026.

Regulatory compliance map: line‑by‑line interpretation of recent rule changes (including 2025 updates to regional VOC rules, EU deliberations on formaldehyde and chlorinated paraffins, and PFAS risk management developments) and a compliance‑to‑product roadmap that links likely regulatory timing to reformulation windows.

Product innovation roadmap: prioritized R&D initiatives (biobased formulations, neo‑synthetics, additive optimization) grounded in cost‑benefit matrices and customer willingness‑to‑pay analysis.

Commercial playbooks: segmentation approaches, pricing optimization levers, and service bundling concepts (fluid management services, on‑site monitoring, and pay‑per‑use models) to drive higher lifetime value.

M&A and partnership framework: target profiles, valuation sensitivities tied to regulatory and supply risks, and integration checklists for bolt‑on acquisitions and technology partnerships.

The market is characterized by a mix of global integrated energy and chemical majors, long‑established specialty lubricants firms, and regional players with strong local service capabilities. Key companies covered in our analysis include Castrol (UK), ExxonMobil (USA), FUCHS (Germany), Houghton, Quaker Chemical, TotalEnergies/Total, Chevron Phillips Chemical, Lubrizol, APAR, Eni, Cimcool, Henkel, Blaser Swisslube, Master Fluid Solutions and others. Each plays a differentiated role: majors leverage scale, distribution and base‑oil integration; specialty firms compete on formulation expertise, service models and customer intimacy.

Recent product initiatives illustrate the push for more sustainable and higher‑performance solutions. Examples include launches of eco‑friendly MWF lines, next‑generation emulsions that extend sump life and operational efficiency, and bio‑compatible formulations aimed at aerospace and other precision sectors. These industry moves underscore two convergent trends: a technological race to reduce environmental and occupational risks, and a commercialization race to convert formulation advantages into recurring revenue through service and lifecycle propositions.

Regulatory tightening: new limits and testing expectations are shifting the cost of compliance and raising barriers to entry for legacy chemistries. Suppliers that invest early in compliant formulation will avoid disruptive reformulation costs and win specification slots in regulated facilities.

Feedstock volatility: base‑oil supply challenges projected for 2026 create an urgency to secure feedstock flexibility and invest in additive engineering that reduces raw material intensity.

Customer expectations: OEMs and Tier‑1s increasingly require traceability, emissions transparency and product stewardship across the fluid lifecycle—service models that incorporate monitoring and fluid management achieve stickiness and margin uplift.

Fragmentation opportunity: the market concentration metrics demonstrate room for challenger brands that combine formulation niches, local service excellence and digital enablement to displace incumbents in targeted corridors.

Diversify feedstock and hedge strategically. Short term: secure flexible base‑oil contracts and establish tactical inventory buffers. Medium term: co‑develop alternative base stocks and expand neo‑synthetic and bio‑based capabilities.

Accelerate compliant reformulations into product roadmaps. Prioritize chemistries likely to be restricted and align reformulation milestones with expected regulatory timelines to avoid rushed, expensive transitions.

Monetize services around fluids. Transition from product sales to outcome‑based offerings—on‑site management, performance‑based pricing, and digital monitoring can increase retention and margin.

Pursue bolt‑ons that enhance formulation IP or service reach. Our M&A framework identifies targets that offer cost synergies, access to regulated markets, or proprietary additives that mitigate feedstock risk.

Invest in customer‑facing digital tools. Real‑time sump monitoring, lifecycle analytics and an integrated compliance dashboard are effective differentiators for winning OEM specifications.

Boards and executive teams need decision templates that convert market trajectories and regulatory catalysts into capital and operating choices. Our forecast and scenario tools let executives stress‑test outcomes under multiple permutations of regulatory timelines, feedstock scarcity, and customer adoption curves. The result: actionable thresholds for greenlighting capex, pulling forward reformulation plans, or accelerating M&A activity.

Strategic Procurement: procurement heads can use our supplier risk matrices and hedging playbooks to maintain continuity and control cost inflation.

R&D and Product Management: product teams receive a prioritized innovation agenda that aligns technical feasibility with commercial payoff.

Commercial & Sales Leadership: go‑to‑market scripts and pricing optimization tools help field teams convert technical advantages into margin‑accretive contracts.

Investors & M&A Teams: scenario‑driven valuations, target screening and integration roadmaps sharpen deal selection and execution.

This release is designed as a strategic preview. To preserve the competitive integrity of our primary research and to ensure clients retain exclusive deployment value, core subsegment tables and granular regional/application splits are available only in the full report. If your team needs executable templates — including the downloadable scenario model, supplier scorecard Excel, or the reformulation ROI calculator — those are distributed with the paid report package.

Immediate (0–3 months): adopt our procurement hedging checklist and baseline regulatory impact assessment to stabilize near‑term operations.

Near term (3–9 months): execute prioritized reformulation and pilot service bundles with select customers; run supply continuity drills tied to the base‑oil scenarios.

Medium term (9–18 months): evaluate targeted acquisitions or technology partnerships using our M&A valuation sensitivities and integration playbooks.

For executives preparing 2026 budgets and strategic plans, PW Consulting’s Metalworking Fluids market brief converts market growth expectations — reflecting a projected rise from a 2025 base through 2032 at a 4.8% CAGR — into a practical, prioritized agenda. The industry is in a phase where regulatory pressure, feedstock risk and customer demand for sustainable, high‑performance chemistries intersect to create both risks and opportunities. Firms that treat regulatory compliance and supply‑chain resilience as strategic assets will not only protect margin, they will capture disproportionate share of the sector’s incremental value.

To access the full dataset, downloadable decision models, and client‑only implementation toolkits, visit our report page or contact PW Consulting’s industry desk. Our team stands ready to help translate the report’s scenarios into a bespoke action plan tailored to your organization’s risk tolerance and growth objectives.

For detailed analysis of this topic, please visit the official page:Metal Working Fluids (Metalworking Fluids) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com