The Foundational Power and Scope of the Global Event Stream Processing Industry

Other |

2026-06-25 06:12:50

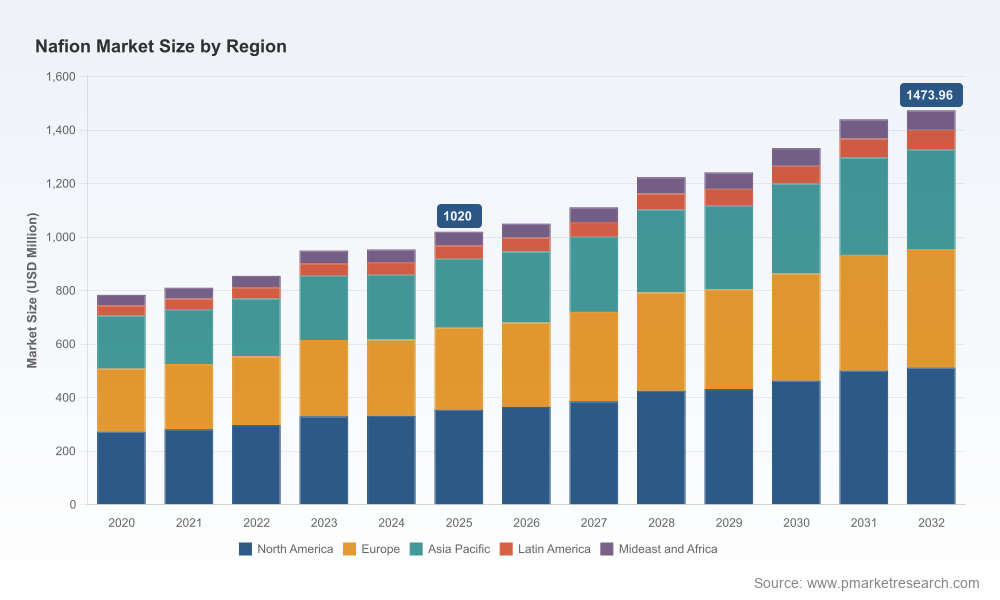

PW Consulting’s Nafion Market report (base year 2025; historical coverage 2020–2025; forecast period 2026–2032) synthesizes market dynamics that will shape high‑stakes decisions in 2026. The Nafion ecosystem — encompassing membranes, dispersions and resins used across fuel cells, electrolyzers, chlor‑alkali, and other electrochemical applications — has demonstrated steady expansion, with the total market advancing from a mid‑hundreds million USD footprint in 2020 to just over one billion USD by 2025. Our forecast model projects continued growth through 2032 at a compound annual growth rate of approximately 5.4%, delivering meaningful scale for incumbents and creating a widening set of strategic choices for new entrants and downstream OEMs.

Nafion Market

Portfolio prioritization: As demand pathways for clean hydrogen and fuel cell technologies solidify, Nafion‑based components are moving from niche to industrial scale. 2026 is a pivot year for companies to decide whether to double down on Nafion chemistry (capex, vertical integration, long‑term supply contracts) or to pursue alternate PEM chemistries and supply diversification.

Nafion Market

Supply chain resilience: Raw material price volatility and energy‑driven cost swings are driving procurement teams to re‑engineer sourcing strategies. Organizations that implement multi‑tier supplier visibility and hedging protocols for fluorinated precursors will preserve margin and program timelines in 2026 and beyond.

Nafion Market

Regulatory leverage: Policy momentum — notably hydrogen strategies in major jurisdictions — is accelerating commercialization pathways for Nafion applications. Companies that align product standards, certification programs, and project pipelines to regulatory windows will capture first‑mover advantages.

Competitive positioning: The Nafion market displays a concentrated supplier landscape (CR3 ≈ 68.5%; CR5 ≈ 75.0%), creating both stability and strategic friction for buyers. Understanding the implications of supplier concentration—price negotiation leverage, innovation capture, and supply security—is essential heading into 2026.

Time‑series market model (2020–2032) with scenario variants that quantify demand under conservative, base, and accelerated technology adoption cases.

Bottom‑up demand drivers and production‑capacity overlays that map OEM programs to polymer demand trajectories and identify timing mismatches that can create short‑term shortages or price spikes.

Supplier benchmarking and vendor scorecards covering manufacturing footprint, technical capability, channel strategy, IP position, and commercial terms — presented to support supplier selection, JV structuring, and M&A diligence.

Actionable go‑to‑market playbooks for membrane manufacturers, dispersion formulators, and resin suppliers — including channel design, licensing frameworks, and sample commercial agreements to accelerate partner onboarding.

Technology risk matrix and R&D roadmap options that prioritize incremental cost reduction levers versus disruptive material substitutions, with expected payback horizons under multiple policy environments.

Investment‑grade scenario analyses and sensitivity testing for capital projects, covering feedstock price shock, energy cost regimes, and contract tenor assumptions to stress‑test business cases.

Regulatory intelligence and policy impact appendices that translate hydrogen strategies, emissions targets, and procurement incentives into quantifiable addressable demand estimates for Nafion‑based products.

Note: This preview intentionally omits the granular segmentation tables and unit‑level pricing schedules included in the full report; those datasets and downloadable model files are available on the PW Consulting report portal.

Our competitive analysis centers on a small number of established players that define technology standards, distribution channels, and manufacturing scale in the Nafion market. Key profiles included in the report:

The Chemours Company — Originator of Nafion™ perfluorosulfonic acid polymers with an integrated product set (membranes, dispersions, resins). Chemours’ commercial strategy and capacity investments materially influence global supply dynamics and technology roadmaps.

Ion Power, Inc. — Value‑added manufacturer and authorized distributor focused on electrochemical applications; acts as a bridge between polymer producers and OEM integrators.

Perma Pure LLC — Specialist in Nafion® tubing and gas conditioning components, representing the application‑specific end of the value chain where materials meet system design.

Beantown Chemical — Supplier and distributor oriented to research and small‑batch customer segments; plays a role in innovation diffusion and early‑stage application testing.

What this concentration means for corporate strategy: incumbents enjoy price discipline and IP advantages, but the market is not immune to disruption. Strategic buyers should consider layered approaches — combining long‑term supply agreements with selective equity investments or co‑development partnerships — to secure product continuity while accessing novel material pathways.

Corporate performance and visibility: The Chemours Company’s 2025 financial disclosures underscored the ongoing commercial relevance of their Nafion product family, and industry commentary through early 2026 indicates tightened attention on capacity planning and margin management across the value chain.

Industry collaboration: Industry working groups and co‑authored studies led by established suppliers are harmonizing technical standards and emissions accounting practices — a critical step toward scalable adoption in automotive and stationary energy markets.

Capacity and investment signals: Recent capital projects to expand production capacity in strategic locations reflect an industry positioning for hydrogen and fuel cell commercialization. These moves reduce medium‑term supply risk but create near‑term execution pressure on commissioning and quality validation.

Raw material and energy cost volatility: Fluorinated feedstocks and energy‑intensive processing expose Nafion producers to commodity cycles and geopolitical supply disruptions. Procurement strategies that combine multi‑sourcing with contractual hedges will materially lower P&L volatility.

Regulatory opportunity and compliance burden: Supportive hydrogen policies create demand corridors, but evolving regulatory standards for fluorinated compounds introduce compliance and liability considerations that must be managed through lifecycle analyses and product stewardship programs.

Technology evolution pressure: Alternative proton exchange membranes and non‑fluorinated chemistries continue to advance. Organizations must balance investment in current‑state Nafion capabilities with a structured R&D watchlist to avoid being technologically locked‑in.

Supply concentration risk: High CR3/CR5 metrics suggest that a limited set of suppliers can influence supply terms; buyers should treat supplier relationships as strategic assets and incorporate contingency capacity into sourcing plans.

For manufacturers: Accelerate capacity synchronization to demand signals, establish staged product qualification exits for new plants, and deploy modular upgrades to reduce startup risk.

For OEMs and system integrators: Lock multi‑year supply agreements with volume flex provisions, co‑invest in qualification testing to reduce time‑to‑market, and fund joint development to tailor Nafion grades to system needs.

For investors: Use the PW Consulting scenario models to stress‑test capex timing and returns under varying policy uptake rates; prioritize assets that combine technological differentiation with de‑risked feedstock exposure.

For policy makers and project sponsors: Design procurement windows and incentive structures that reduce first‑mover commercialization risk while preserving competitive supplier participation.

PW Consulting’s Nafion Market report is intended to be an operational playbook as much as a market study. Clients gain access to our downloadable financial model, supplier scorecards, regulatory impact templates, and a prioritized list of near‑term action items tailored by corporate archetype (supplier, OEM, investor, policy body). We combine primary interviews, plant‑level capacity mapping, and proprietary demand‑supply modeling to deliver recommendations that are immediately executable.

Leading organizations are already using the market trajectories and supplier intelligence in this report to set 2026 procurement cycles, capex approvals, and R&D priorities. For executives preparing to finalize their 2026 strategic plans, the full PW Consulting Nafion Market report provides the granular segmentation, contract‑level pricing scenarios, and downloadable models necessary to move from intent to execution. To access the complete dataset and model files, visit the Nafion Market report page on the PW Consulting website or contact our industry team for a briefing.

For detailed analysis of this topic, please visit the official page:Nafion Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com