Automotive Steel Piston Market: Strategic Imperatives for 2026 Decision-Makers

Executive summary

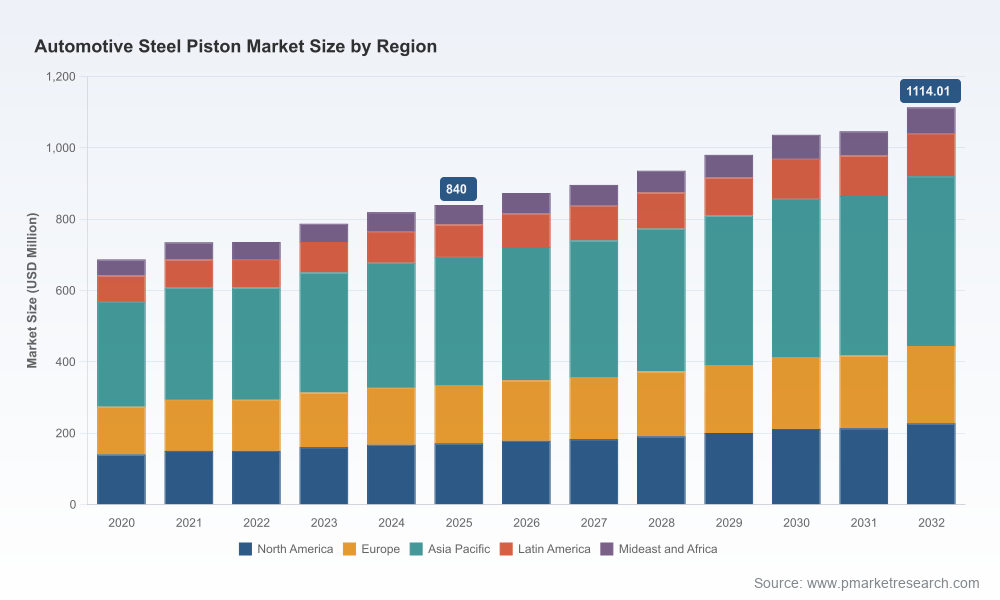

PW Consulting's Automotive Steel Piston Market report (base year 2025) provides a focused, actionable intelligence package designed to support board-level and operational decisions through 2026 and beyond. The global market expanded from USD 687.5 Million in 2020 to USD 840.0 Million in 2025 (USD Million), and our modeling shows a continued expansion at a compound annual growth rate (CAGR) of 4.2% through the 2026–2032 forecast window. Under our base forecast, the market reaches approximately USD 873.6 Million in 2026 and is projected to approach USD 1,114.0 Million by 2032.

Automotive Steel Piston Market

This release is structured as a “trailer”: it outlines the strategic implications, methodological rigor, and practical tools included in the full report, while deliberately reserving detailed segmented forecasts and proprietary matrices for report download. The aim is to demonstrate our depth of analysis and immediate utility for 2026 planning cycles while encouraging executives to engage with the full dataset for transaction-level or plant-level decisions.

Automotive Steel Piston Market

Why this matters for 2026 planning

- Capital allocation and capacity planning: modest but steady market growth (CAGR 4.2%) changes the calculus for investments in forging, welding capacity, and precision machining. Decisions initiated in 2026 will reach steady-state during the forecast horizon — making this the inflection moment for brownfield expansions vs. opportunistic greenfield

- Product strategy under regulatory pressure: diesel and heavy-duty applications continue to demand high-strength steel piston solutions that offer durability and emissions benefits. Suppliers and OEMs that position around these attributes will capture disproportionate value as long-tail ICE demand persists in commercial fleets

- Competitive moves and M&A windows: moderate market concentration (CR3 ~35%; CR5 ~38%) indicates leading suppliers capture meaningful share while significant portions of the market remain accessible to regional specialists, new entrants, and technology-focused challengers. 2026 is a strategic year to evaluate tuck-ins and capability buys

Market dynamics and technology drivers

Three engineering and regulatory dynamics are defining buyer requirements and supplier economics:

Automotive Steel Piston Market

- Peak-pressure, high-strength requirements: modern heavy-duty diesel applications require steel piston constructions capable of withstanding peak ignition pressures up to 300 bar — a performance threshold that influences alloy selection, joining techniques, and bore-sizing strategies (Mahle Official Product Catalog, 2026).

- Emissions and lifecycle optimization: steel pistons are not merely a strength play. Through improved friction management and thermal control, steel piston systems can contribute to quantifiable CO2 reductions at the engine level, with supplier literature citing potential CO2 savings on the order of single-digit percentages in optimized applications (Kolbenschmidt Pistons Official Website, 2026).

- Advanced joining and design techniques: laser-welded and friction-welded constructions permit reduced compression heights, superior cooling paths, and lower friction losses — enabling both performance gains and packaging advantages in high-output engines (Mahle Official Product Catalog, 2026; Tenneco Official Product Page, 2026).

These technological enablers also shift the cost curve: enhanced processes increase per-unit cost but extend service life (field data show service lives in commercial applications exceeding one million kilometers in some platforms), changing total cost of ownership calculations for fleet operators (Mahle Official Product Catalog, 2026).

Competitive landscape — what executives need to know

The steel piston market is characterized by a mix of global Tier-1 specialists and regional manufacturers with deep OEM ties. Leading players combine systems know-how with materials science and high-precision manufacturing:

- Mahle GmbH (Stuttgart, Germany) — offers multiple steel piston concepts for passenger and commercial platforms, including friction- and laser-welded designs engineered for peak pressures and optimized cooling (https://www.mahle.com).

- KS Kolbenschmidt Pistons (KSPG AG / Rheinmetall Automotive) (Neckarsulm, Germany) — focuses on steel systems across heavy-duty segments with add-on technologies that target emissions reductions and fuel-efficiency gains (https://www.kolbenschmidt-pistons.com).

- Tenneco Inc. (Southfield, Michigan, United States) — markets Monosteel® friction-welded one-piece pistons and expanded steel piston offerings for large-bore commercial diesel engines (https://www.tenneco.com).

- Aisin Seiki Co., Ltd. / Art Metal MFG. Co., Ltd. (Nagoya, Japan) — integrated OEM and aftermarket supplier with steel piston and piston-pin capabilities feeding global powertrain programs (https://www.aisin.com).

- Hitachi Astemo, Ltd. (Tokyo, Japan) — supplies steel piston solutions in OEM channels, emphasizing systems integration for engine performance (https://www.astemo.com).

- Shriram Pistons & Rings Ltd. (Chennai, India) — regional leader in forged steel pistons for heavy-truck platforms, with a value proposition centered on fuel efficiency and durability (https://shrirampistons.com).

The picture this creates is one of selective dominance: top specialists command meaningful share and technology leadership, while mid-sized and regional manufacturers retain crucial relationships in high-volume domestic fleets and aftermarket channels. For buyers and investors, the implication is clear: partner selection should be based on long-run platform commitments and capability roadmaps (forging, welding, coating, and thermal-treatment competencies), not purely price.

Report contents — practical deliverables

The full PW Consulting report provides end-to-end, transaction-ready assets for 2026 decision cycles. Highlights include:

- Top-line market sizing and historical reconciliation (2020–2025) with transparent methodology and sensitivity checks.

- Base-case and alternate scenarios to 2032, with sector-specific drivers and downside stress tests tied to fuel prices, electrification trajectories, and raw-material volatility.

- Price and cost curve modeling for key manufacturing processes (forging, friction-welding, laser-welding, heat treatment) and an input-cost sensitivity module denominated in USD Million.

- Supplier benchmarking and capability matrices for the named incumbents plus a curated list of regional challengers.

- Supply chain heatmaps, risk scoring, and mitigation playbooks — including supplier dual-sourcing, alloy-substitution pathways, and logistics contingency planning.

- Commercial playbooks tailored to OEMs, Tier-1s, aftermarket distributors, and private-equity investors (partnering frameworks, commercial terms, warranty design, and service offerings).

- Deal-screen templates and a shortlist of M&A targets fitted to three corporate archetypes: scale acquirers, margin improvers, and technology consolidators.

Importantly, segmented tables and granular regional and application-level forecasts are contained in the full dataset and accompanying Excel models. Those segmented cells are intentionally gated to preserve the report’s commercial value and to ensure licensing for downstream use.

Strategic recommendations for 2026 (by stakeholder)

- OEMs: Prioritize platform-level lifecycle cost modeling. Where heavy-duty platforms remain core to your portfolio, specify steel-piston options early in program APQP cycles and lock in supplier performance guarantees tied to CO2 and TCO metrics.

- Tier suppliers: Invest selectively in welding and coating capabilities that lower friction and improve thermal management. Consider capability partnerships (co-investments or JV) with foundry and heat-treatment specialists to control lead times and improve margin capture.

- Material and process technology providers: Accelerate R&D on low-density alloy adaptations and coating systems that preserve strength while reducing reciprocating mass; market narratives that tie material choices to fleet-level emissions benefits will unlock OEM specification windows.

- Aftermarket and fleet operators: Reframe procurement to prioritize total life cost and uptime. Given field evidence of extended service lives for steel systems, warranty and service bundles can be a differentiator.

- Investors and M&A teams: Screen targets against three criteria — OEM connectivity, differentiated process capability (e.g., friction- or laser-welding IP), and defensible cost curves. The current market concentration profile favors bolt-on acquisitions that enhance technology or geographic reach.

How to use the forecast — practical notes and limitations

Our base-year alignment (2025) and historical reconciliation (2020–2025) ensure that the 2026 planning cycle has a robust, audit-ready starting point. The 4.2% CAGR to 2032 reflects bottom-up demand drivers and verified supplier capacity; however, two caveats merit emphasis:

- Electrification risk is asymmetric: passenger-car BEV penetration will reduce some ICE piston demand more quickly than commercial and heavy-duty segments, which remain the core structural market for steel pistons for the near-to-medium term.

- Raw-material and process shocks can materially change unit economics; buyers should run sensitivity scenarios around steel billet prices and key process yields before locking large CapEx decisions.

For clients using the report to underpin contractual or CapEx commitments, we recommend a two-stage approach in 2026: (1) adopt the report’s base and two alternate scenarios in internal business cases; (2) commission a short-form bespoke module from PW Consulting that maps your specific platform volumes against the report’s detailed segmented model.

Next steps — obtaining the full intelligence

This release highlights the strategic value embedded in PW Consulting’s Automotive Steel Piston Market research: validated market sizing, technology-led dynamics, a pragmatic competitive map, and a set of executable recommendations for the 2026 planning cycle. For access to the full segmented datasets, Excel models, supplier scorecards, and the exclusive appendices that contain regional and application-level forecasts, please download the full report from PW Consulting’s publications page or contact our automotive practice to commission a tailored briefing and scenario run.

PW Consulting stands ready to convert this market intelligence into procurement contracts, CapEx decision frameworks, and M&A diligence packages — helping clients convert the projected 4.2% CAGR and the evolving technical landscape into market advantage in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Automotive Steel Piston Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com