Buy Funeral Flower Arrangements Mississauga OnlineShop

Gardening |

2026-04-13 19:16:03

PW Consulting today publishes a forward-looking intelligence briefing on the Precipitated Barium Sulfate (PBS) market that is designed to be immediately actionable for executive teams planning investments, procurement strategies, and commercial plays in 2026. Built on a base year of 2025 with a historical window spanning 2020–2025 and a detailed forecast through 2032, the study quantifies a steady expansion trajectory — from an assessed global market of USD 356.25 Million in 2020 to USD 437.4 Million in 2025, and a projected rise to USD 583.94 Million by 2032 — implying a compound annual growth rate (CAGR) of 4.16% through the forecast period.

Precipitated Barium Sulfate Market

Timing: Many capital and commercial plans that will be implemented in 2026 are being finalized now. This briefing translates macro growth into operational scenarios that show where margin capture and risk exposure will crystallize over the next 18–36 months.

Precipitated Barium Sulfate Market

Cost and supply pressure: The market is exhibiting sustained cost inflation on multiple fronts — raw materials, freight, and select critical inputs — requiring procurement teams to update price-forecasting and hedging assumptions for 2026 budgets.

Precipitated Barium Sulfate Market

Competitive positioning: With a moderately concentrated supplier base (CR3 ≈ 46.5%; CR5 ≈ 53.2%), converging commercial moves by top producers materially affect availability and commercial leverage in key end-use value chains.

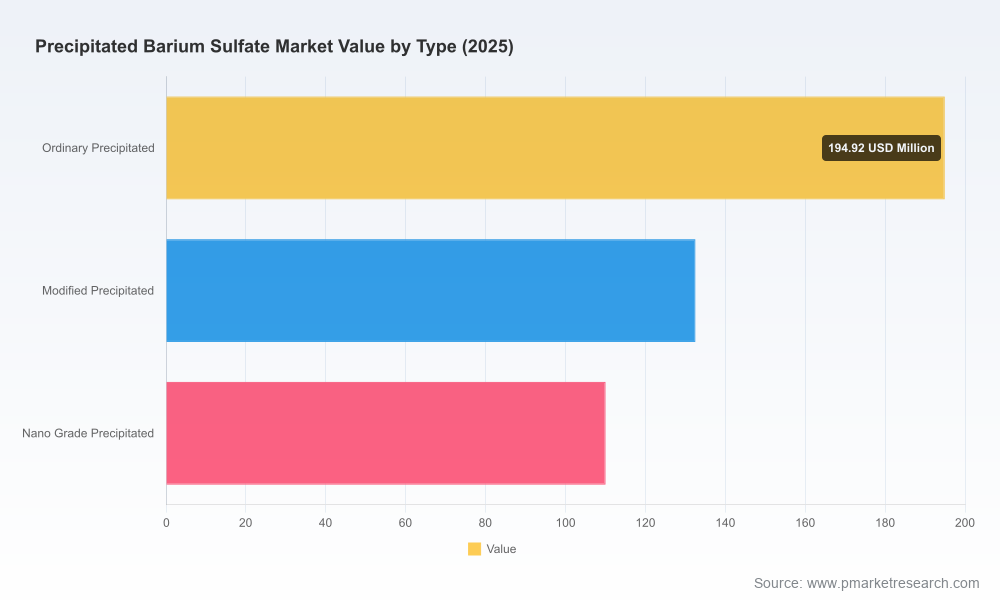

The PBS market’s trajectory reflects both steady demand recovery post-2020 and structural shifts in formulations and end-use requirements. Between 2020 and 2025 the market expanded from approximately USD 356 Million to USD 437 Million, an acceleration driven by specialty-demand in engineered coatings and polymer formulations that require controlled particle properties; our base-case forecast shows continued growth to roughly USD 468.6 Million in 2026 and a sustained climb to nearly USD 584 Million by 2032 under current conditions.

Key demand drivers include formulation replacement cycles in paints and plastics, growing specification requirements in high-performance powder coatings, and incremental uptake in niche applications such as specialty healthcare composites and precision pigments. Equally important are substitution dynamics: where formulators seek performance per unit cost, differences in surface treatment and particle engineering are changing specification windows, creating opportunities for differentiated grades and premium pricing.

Input-cost inflation: We observe upstream pressure across the supply chain. Bulk-freight and container cost inflation has amplified delivered costs for import-dependent markets. Separately, escalating prices for critical chemicals (e.g., antimony and allied inputs) are triggering manufacturer price passes and compressing gross margins if not absorbed or offset by productivity gains.

Commercial responses: Leading suppliers have already signalled and implemented price adjustments. Notable industry moves include coordinated price increases announced in early 2025 by several suppliers to address elevated raw-material and production expenses, and earlier specialty-mineral price actions by major North American producers. These actions set a new baseline for commercial negotiations in 2026 and reduce the window for catching up on historic margin erosion.

Capacity balances: Capacity additions in select regions were completed in 2024, and the near-term effect is a tighter structural balance in higher-spec grades. However, capacity expansion cycles are uneven globally, which translates to geographic pockets of price sensitivity and supplier leverage.

This is not a high-level overview. The briefing delivers practical tools and calibrated scenario workstreams that can be embedded in 2026 planning decks. Highlights include:

Scenario-based demand modeling keyed to key macro and micro variables (GDP drivers, construction cycles, paint & plastics demand drivers), with sensitivity analyses that translate percentage swings in end-use demand into revenue and margin outcomes for manufacturers and distributors.

Supply-chain stress tests and supplier concentration maps that allow procurement teams to run “what-if” scenarios for supplier failure, freight shocks, and regional export controls.

Price-elasticity matrices for different value tiers (commodity vs. engineered grades) to guide pricing strategies and contract design through 2026.

Capital-expenditure (capex) playbooks which assess the payback for incremental capacity additions, beneficiation of particle-technology assets, and retrofit investments aimed at margin recovery under different pricing regimes.

Go-to-market frameworks for specialty producers, including channel strategies, formulation partnerships with major coatings and polymer producers, and premiumization blueprints.

M&A and JV scorecards that prioritize targets by technology, geographic footprint, and customer overlap — structured to shorten diligences and support rapid transaction calls in an environment where capacity consolidation materially affects pricing power.

The PBS sector is served by a mix of integrated minerals businesses and specialized chemical manufacturers. Our briefing focuses on the companies that materially shape supply, specification standards, and price-setting in North America, Europe, and Asia. Among the prominent names examined in depth are:

Cimbar Performance Minerals (Chatsworth, Georgia, USA) — historically one of the largest North American producers, with a product portfolio tailored to paints, coatings, plastics, printing inks, and lead-acid battery markets. Recent commercial decisions by the company around specialty-mineral pricing are an important signal for market comparables.

Nippon Chemical Industrial Co., Ltd. (Tokyo, Japan) — a supplier of high-purity precipitated barium sulfate for demanding industrial applications; the company’s product positioning underscores a trend toward performance differentiation as a route to margin protection.

Shanghai Tengmin Industry Co., Ltd. (Shanghai, China) — focused on bulk filler products and pigment-grade solutions for coatings and paints, playing to the large-scale domestic demand and export channels in the Asia Pacific region.

Hubei Qinba Advanced Materials Co., Ltd. (Hubei Province, China) — a specialist in synthetic PBS for high-performance powder coatings and industrial applications; strategic pricing moves by Hubei Qinba and peers in early 2025 materially impacted regional price baselines.

Our competitive analysis goes beyond profiling: it synthesizes commercial signals (price actions, capacity investments, product launches) into a playbook that tells manufacturers, distributors, and buyers where negotiating power will consolidate and where strategic partnerships will be decisive in 2026.

Regulatory and trade exposure: Export-import dependencies and compliance requirements for critical inputs create non-linear risk profiles by geography. Our briefing provides monitoring triggers that map regulatory changes to immediate supply disruption risk and medium-term cost impacts.

Logistics sensitivity: Bulk-freight and container cost inflation has been an active risk driver in import-reliant markets. We quantify the leverage that freight dynamics exert on delivered cost and recommend contract structures to mitigate spot volatility.

Input concentration: The price and availability of specific critical inputs (notably antimony and allied reagents) have driven recent supplier price increases. Our supplier risk matrix ranks inputs by substitution difficulty and procurement lead time to help procurement teams prioritize hedges.

Manufacturers: Accelerate product-tiering initiatives that separate commodity grades from engineered, premiumized products. Direct capex to particle-engineering assets that unlock product differentiation and higher margin pools.

Buyers / formulators: Shift from single-indexed contracts to hybrid models that combine volume commitments with index-based pass-throughs and performance rebates. Leverage supplier competition where capacity is available, but prepare fallbacks for geographies where supplier concentration is high.

Distributors: Expand value-added services (technical formulation support, just-in-time logistics) to defend margins as raw-material pass-throughs compress spread.

Investors and M&A teams: Prioritize targets that either strengthen footprint in low-cost feedstock regions or bring proprietary surface treatments and particle-engineering capabilities that can be cross-sold into coatings and high-performance plastics customers.

Executives told us they need intelligence that maps directly into boardroom decisions. The PW Consulting PBS briefing is structured to be clip-and-play into investment memoranda, procurement strategies, and commercial playbooks. It contains ready-made slides, risk registers, contract templates, and a prioritized checklist for due diligence teams — all linked to the underlying scenario models so teams can re-run assumptions for specific corporate circumstances.

We intentionally withhold certain granular segmentation tables and proprietary vendor-level pricing curves in this summary: our objective is to present depth and trust while directing stakeholders who require the full dataset and executable templates to our complete report and supporting data room. This ensures strategic gatekeeping of high-value inputs and enables tailored briefings for corporate subscribers and transaction clients.

The Precipitated Barium Sulfate market is no longer a background commodity story. Between persistent input-cost inflation, concentrated supplier behavior, and shifting formulation requirements in core end-use markets, the 2026 planning year will be a decisive window for capturing margin and competitive advantage. Organizations that update their procurement frameworks, reprioritize capex towards product differentiation, and adopt dynamic contract structures will be the ones to convert the forecasted market growth into durable enterprise value.

For boards, executive teams, and investors preparing 2026 strategies, PW Consulting’s full report — including the complete data appendices, supplier scorecards, and transaction-ready diligence templates — provides the granular inputs required to make high-conviction decisions. To request access to the full report and to schedule a tailored briefing, please visit our report portal or contact your PW Consulting representative.

For detailed analysis of this topic, please visit the official page:Precipitated Barium Sulfate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com