North America Digital PCR Market Innovation Trends 2031

Other |

2026-06-30 10:58:38

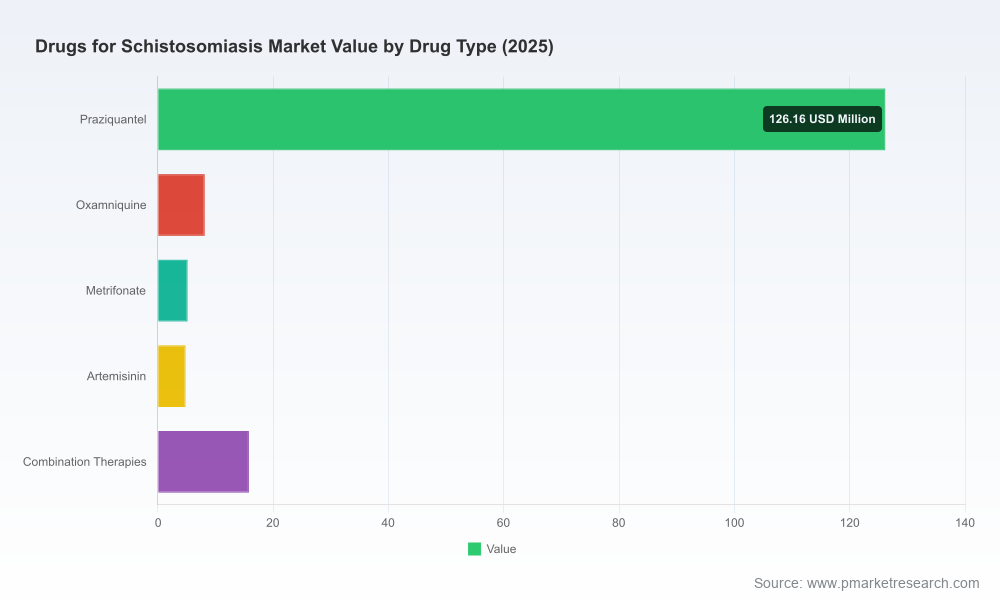

PW Consulting’s new market study on Drugs for Schistosomiasis provides the strategic intelligence that pharmaceutical manufacturers, donors, national health authorities, and private-sector investors need to shape high-conviction decisions in 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study quantifies a market that expanded from an estimated USD 118.5 million in 2020 to USD 160.0 million in 2025 and is projected to reach approximately USD 244.8 million by 2032, at a compound annual growth rate (CAGR) of 6.4%. This briefing distills the report’s key implications without disclosing the proprietary segment-level datapoints reserved for the full report—enough to inform immediate strategy, while pointing readers to the detailed models and country-level maps behind these conclusions.

Drugs for Schistosomiasis Market

Market maturity with concentrated dynamics: The market shows clear maturation patterns: a steady expansion in total value and persistent concentration among a small set of established producers. Our concentration metrics indicate that the top three players control a majority share and the top five approach three-quarters of the market — a structure that creates both stability and bottlenecks in global supply and procurement planning.

Drugs for Schistosomiasis Market

Policy-driven demand growth: Continued WHO endorsement and prequalification pathways—especially for pediatric formulations—are reshaping procurement preferences and creating distinct volumes tied to mass drug administration (MDA) campaigns and school-based platforms. These policy levers translate into predictable procurement windows that can be modeled into production planning and tender strategies.

Drugs for Schistosomiasis Market

Supply-side vulnerabilities: The interplay of patent expiries, geographic concentration of specialized manufacturing, and episodic geopolitical tensions has introduced intermittency into supply lines. These dynamics are not hypothetical: 2025 saw concrete instances of production discontinuity and temporary substitution in regulated markets, underlining the need for contingency plans and resilient supplier portfolios.

Robust market sizing and a transparent forecasting model: We provide a bottom-up model reconciled with demand drivers (MDA cycles, pediatric rollouts, clinical usage) and macro variables. The model is fully auditable and can be adapted to client-specific scenarios (e.g., alternative uptake curves, accelerated elimination programs).

Scenario-based revenue and demand dashboards: Users can stress-test outcomes under alternative assumptions—faster WHO-driven adoption of pediatric dispersible products, delayed procurement due to logistics disruptions, or accelerated generic entry—without compromising the report’s confidentiality for core segment datapoints.

Actionable go-to-market playbooks: For manufacturers and distributors, the report includes concrete launch sequencing recommendations, tender engagement playbooks, pricing levers matched to procurement modalities, and product-differentiation options (including pediatric formulations and combination therapies).

Country and procurement intelligence: Country-level risk matrices, procurement cycles, and donor-mapping highlight near-term opportunities and timing for supply agreements—structured to support business development teams in prioritizing targets in 2026.

Supply-chain and manufacturing playbooks: Practical guidance on dual-sourcing, tech-transfer triggers, inventory buffer sizing, and regulatory fast-tracks—designed to reduce the likelihood and impact of the disruptions observed in 2025.

Competitive intelligence dossiers: In-depth profiles of incumbent manufacturers, their capabilities, WHO prequalification status, recent product introductions, and alliance footprints—enabling targeted partnership and M&A screening.

The market continues to be dominated by a mix of global innovators and cost-optimized generics manufacturers. Our competitive review highlights five firms whose strategic moves will disproportionately influence market access, pricing, and supply in 2026:

Merck KGaA (Darmstadt, Germany): A leading supplier of standard praziquantel and the first mover on pediatric arpraziquantel dispersible tablets. Their recent operational investments and WHO-aligned supply agreements have positioned them as the primary partner for scaled pediatric rollouts. Strategic implication: manufacturers and donors should treat Merck as a de facto anchor supplier for pediatric programs while preparing contingency capacity in parallel.

Bayer AG (Leverkusen, Germany): Historically significant as the owner of a branded praziquantel product, Bayer’s production decisions can create near-term market dislocations in regulated markets. The 2025 temporary production shifts underscore the sensitivity of European and other high-regulation markets to manufacturing changes. Strategic implication: regulatory and procurement teams must plan for short-term substitution and rapid product registration contingencies when incumbent producers alter supply.

Taj Pharmaceuticals Ltd (Mumbai, India): A volume-focused generic producer with strengths in supplying mass drug administration programs. Their cost position and local manufacturing footprint make them a natural participant in government tenders across endemic regions. Strategic implication: players seeking scale should engage early with Indian generics for co-manufacturing or contract manufacturing relationships.

Cipla Ltd (Mumbai, India): Noted for WHO prequalification of generic praziquantel, Cipla occupies a privileged position in donor and government procurement channels for essential medicines. Strategic implication: prequalification status confers preferential procurement access—an important variable for market entry and tender strategy.

Shin Poong Pharmaceutical Co. Ltd (Seoul, South Korea): An experienced producer with a track record of supplying generics globally. Their presence illustrates the cross-regional footprint of specialized praziquantel production. Strategic implication: consider regional supply partnerships that leverage Shin Poong’s manufacturing expertise.

Operational shifts: In 2025, Bayer’s pause in global production of its branded praziquantel product caused temporary importation and relabeling dynamics in some markets. That event crystallized a broader operational risk—single-source legacy production can create procurement friction in regulated geographies.

Programmatic advances: Merck’s distribution of arpraziquantel pediatric tablets to preschool-aged children in Uganda and the formalized partnership with the END Fund signal an industry pivot toward child-optimized treatment strategies. Programmatic momentum around pediatric formulations is likely to accelerate adoption and alter demand composition over the next 18–36 months.

Supply constraints: The industry experienced episodic supply chain interruptions in 2025 tied to geopolitical tensions and limited specialized manufacturing capacity. These constraints had measurable impacts on MDA timetables and donor procurement behavior, reinforcing the strategic value of resilience investments.

Regulatory tailwinds: Ongoing WHO prequalification and essential medicines listing for new pediatric formulations are driving preferential pricing and procurement access—an advantage that holders of such credentials can monetize through prioritized tenders.

Patent landscape: Expirations and patent cliffs have enabled multiple low-cost Indian and South Korean generics to scale into government procurement. While this intelligent commoditization reduces unit costs, it also compresses margins and raises the strategic premium on differentiation through service, formulation, and supply reliability.

Short-term (next 6–12 months): Secure capacity commitments and multi-supplier contracts to hedge supply-risk; prioritize WHO prequalification for any new pediatric or combination formulations; and map donor procurement cycles to align offer readiness with tender windows.

Medium-term (12–24 months): Invest in dual-source manufacturing, regional fill-and-finish capabilities, or contract manufacturing agreements to reduce lead times and respond quickly to MDA demand spikes. Explore public–private partnerships to underpin national elimination drives that will create predictable volume growth.

Portfolio & pricing: Balance low-cost generics supply opportunities with selective differentiated products (e.g., dispersible pediatric formulations) where price premiums and tender preference exist. Use the report’s scenario analysis to quantify margin outcomes under alternative uptake assumptions.

M&A and alliances: For private equity and strategic buyers, consolidation opportunities exist where regional production capabilities and WHO-prequalified assets can be aggregated to create a resilient, preferred-supplier profile.

Risk & resilience: Operationalize contingency playbooks for logistics, including buffer inventory sizing reflective of the 2025 supply interruptions, and embed geopolitical risk monitoring within procurement processes.

Use the macro market trajectories and concentration indicators in this briefing to prioritize resource allocation: production scale-up, prequalification investments, or alliance building. Supplement these strategic choices with the report’s granular tools—auditable forecast models, country risk maps, and procurement-tender calendars—to convert strategic intent into executable plans. The real value in 2026 will come from aligning production, regulatory, and commercial actions with donor cycles and national program calendars rather than chasing short-term pricing arbitrage.

PW Consulting’s Drugs for Schistosomiasis Market report provides the data architecture and playbooks required to navigate a market that is growing steadily (CAGR 6.4%), structurally concentrated, and increasingly shaped by policy-driven pediatric initiatives and supply-chain constraints. This briefing sketches the core strategic choices facing industry and public-health decision-makers in 2026; the full report supplies the proprietary segmentation, country-level forecasts, supplier scorecards, and downloadable scenario models required to operationalize those choices.

To access the complete datasets, interactive models, and the prioritized list of high-opportunity country and procurement targets, consult the report landing page on PW Consulting’s website or contact our advisory team for a tailored briefing and model walk-through.

For detailed analysis of this topic, please visit the official page:Drugs for Schistosomiasis Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com