Thermoplastic Polyamide Market 2026: Strategic Imperatives for Decision‑Makers

Executive snapshot

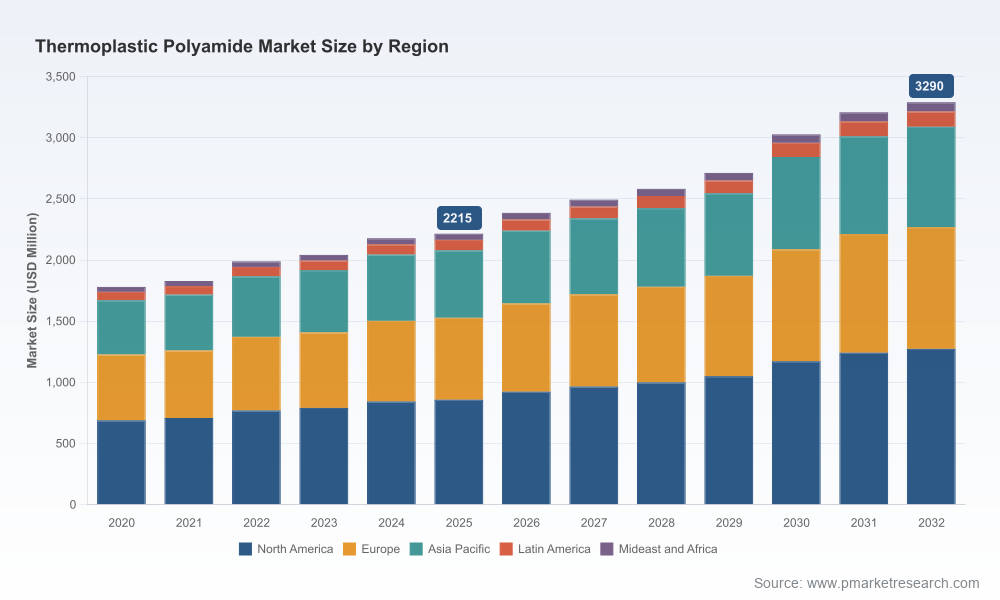

The thermoplastic polyamide market is entering 2026 from a position of steady, structurally driven growth. Our base-year analysis (2025) and seven-year forecast (2026–2032) show a compound annual growth rate (CAGR) of 5.85% across the forecast window. After expanding from approximately USD 1,780 Million in 2020 to USD 2,215 Million in 2025, the market is projected to register continued expansion — rising past USD 2,385 Million in 2026 and trending toward an estimated USD 3,290 Million by 2032. For executives making investment, sourcing, or portfolio decisions in 2026, these topline dynamics frame both opportunity and urgency: demand is robust, but the structure of value capture will hinge on supply-chain agility, material differentiation, and regulatory navigation.

Thermoplastic Polyamide Market

Why this report matters for 2026 decisions

- Proven-growth context: Our analysis combines a five-year historical window (2020–2025) with scenario-based forecasting through 2032, delivering a view that is long enough to detect structural shifts yet short enough to inform near-term capital allocation.

- Actionable rather than academic: The report translates market moves into commercial playbooks — from pricing strategy to localized sourcing and product road-mapping — enabling organizations to convert market visibility into measurable decisions within the next 12–18 months.

- Risk-to-reward mapping: We quantify sensitivity to raw-material swings, tariff and standards changes, and concentrated supply points so leadership teams can stress-test projects and prioritize de‑risking measures.

Market trajectory and strategic implications

The mid‑decade profile of thermoplastic polyamides is characterized by two complementary forces. On the demand side, engineering plastics use-cases (notably in transportation, industrial components, medical devices, and premium consumer applications) continue to drive volume and value migration away from commodity resins. On the supply/cost side, feedstock volatility, concentrated production hubs, and evolving regulatory frameworks have increased the premium for secure, compliant, and sustainable supply chains.

Thermoplastic Polyamide Market

For 2026, the practical implications are clear: firms that lock into differentiated value propositions (lightweighting solutions, bio-circular grades, or performance‑critical compounds) and who can demonstrate supply continuity will capture disproportionate margin expansion. Conversely, entities overly exposed to commodity PA6 feedstock cycles or to single-region sourcing will face compressed returns and heightened capex risk.

Thermoplastic Polyamide Market

Key dynamics and near-term risks

- Raw-material volatility: Caprolactam-linked price moves continue to propagate through PA6 chains. Recent bid-tone increases and ongoing crude‑oil sensitivity mean short-term price spikes are more probable than in the prior decade, requiring disciplined hedging and flexible contract design.

- Regulatory and trade shifts: Updates to tariff classifications and product standards have immediate operational consequences. New customs schedule entries and the rollout of ISO 21036:2025 for PA12 piping, for example, alter compliance pathways for pipeline and industrial customers and may change landed-cost math for exporters and importers.

- Concentration and competition: The market displays moderate top-end concentration: our concentration analysis indicates the three largest players (~CR3) account for approximately 35% of market share, and the top five (~CR5) around 45%. This leaves room for both scale players to defend margin through integration and for niche players to carve out premium positions.

- Innovation and product differentiation: Suppliers are actively launching new grades with focused performance attributes — permeability control, improved hydrophobicity, bio-derived monomers, and tailored flame-retardant systems — shifting the basis of competition toward formulation and systems integration.

Competitive landscape — what to watch in 2026

The competitive field blends global commoditized producers with vertically integrated speciality players. Five names anchor the industry narrative and exemplify different strategic postures:

- BASF SE (Ludwigshafen, Germany) — A broad‑portfolio leader with a focus on engineering-grade PA66, PA6 and copolymers. Recent product introductions signal a push into new performance vectors, including water‑permeable thermoplastic polyamides and targeted consumer collaborations launched in late 2025.

- Evonik Industries AG (Essen, Germany) — Strong in PA12 and specialty resin applications for safety‑critical components; Evonik’s positioning emphasizes high‑value industrial and transportation applications where reliability and certification matter.

- Arkema S.A. (Colombes, France) — Notable for Rilsamid® and Rilsan® brands and for early commercialization of bio‑circular PA11; Arkema’s route to market is centered on premium, sustainability‑oriented applications in automotive and industrial segments.

- Ascend Performance Materials LLC (Charlotte, NC, USA) — As a large fully integrated PA66 producer, Ascend focuses on scale advantages and flame‑retardant grades for electrical and automotive platforms, with strategy leaning on cost control and secure feedstock integration.

- UBE Industries, Ltd. (Tokyo, Japan) — A diversified nylon polymer producer with deep exposure to fiber, industrial yarn, and engineering plastics customers; UBE’s strength is in customized polymer architectures for demanding applications.

Each player’s choices — whether to invest in bio‑feedstocks, expand compounding capacity, or pursue downstream alliances — will materially reshape supply options for OEMs and compounders in 2026 and beyond. Notably, BASF’s late‑2025 launches underline how product innovation can open new use cases and redistribute value along the chain.

What the report contains — practical, executable modules

Designed for commercial, strategic, and M&A teams, the report emphasizes prescriptive outputs over descriptive statistics. Highlights include:

- Market sizing model and scenario engine — a dynamic framework reconciling bottom‑up supplier capacity withtop‑down demand drivers, and three demand scenarios (base, upside, downside) through 2032.

- Price and margin sensitivity matrix — quantifies the impact of feedstock and freight shocks on EBITDA across common product families.

- Supply‑chain heat map — identifies concentrated nodes, alternative sourcing pathways, and the utilities/infrastructure dependencies that drive delivery risk.

- Regulatory and standards playbook — an actionable table linking anticipated regulatory changes (customs coding updates, ISO standards) to compliance steps, certification timelines, and cost implications.

- Competitive dossiers and M&A screening criteria — deep profiles of incumbent suppliers, plus a readiness checklist and valuation heuristics for tuck‑in and scale transactions.

- Commercial go‑to‑market templates — pricing ladders, contract clauses for volatile feedstock, and customer segmentation playbooks tuned to 2026 purchasing behavior.

- Case studies — real‑world examples showing how leading OEMs and compounders mitigated shortages, redesigned components for resin substitution, and accelerated materials adoption cycles.

Strategic playbook for 2026 — recommended actions

- Secure diversified feedstock pathways: Build contingent supply agreements across regions, and design short‑term hedges layered with strategic buffer inventories for high‑impact SKUs.

- Pursue value over volume: Prioritize investments in higher-margin, performance‑differentiated grades (e.g., PA11/PA12, bio‑circular offerings, specialty copolymers) where technical paybacks justify premium pricing.

- Localize selectively: For critical customers and sectors with high compliance touchpoints (medical, piping, automotive safety components), consider closer local compounding or tolling to reduce logistics and tariff exposure.

- Embed compliance early: Treat standards (ISO 21036:2025 and equivalents) and tariff reclassification as product requirements, not afterthoughts — build certification timelines into product launches and procurement cycles.

- Leverage partnerships: Co‑development agreements with compounders, recyclers, and end‑users accelerate qualification cycles and spread commercialization risk.

- Adopt a disciplined M&A filter: Target acquisitions that deliver either technology differentiation (new copolymers, bio‑routes), strategic capacity in undersupplied geographies, or complementary vertical capability (compounding, color/pigment mastery).

How to use this study in boardroom decisions

Boards and executive teams should use the report as the connective tissue between market intelligence and capital decisions. Specific uses include:

- Capex prioritization — a decision framework to evaluate brownfield expansion versus strategic buyouts under multiple price scenarios.

- Sourcing strategy — a phased migration plan to balance cost, service, and compliance objectives across tiers of suppliers.

- Commercial roadmaps — a playbook for pricing, contract architecture, and product launches tied to qualification timelines and regulatory milestones.

- M&A and JV origination — a shortlist of target attributes and integration risks that materially improve the probability of value creation within 24 months.

Conclusion and next steps

Thermoplastic polyamides present a clear growth trajectory through the end of the decade, but the value is not evenly distributed. Companies that combine supply resilience, product differentiation, regulatory foresight, and disciplined commercial execution will be the winners of 2026 and beyond. Our full Thermoplastic Polyamide Market report provides the underlying data models, supplier heat maps, and transaction checklists required to operationalize these recommendations.

For the complete dataset, segmented forecasts, and proprietary scenario models — including downloadable Excel workbooks and supplier scorecards — please visit the report page and request access to the full study.

For detailed analysis of this topic, please visit the official page:Thermoplastic Polyamide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com