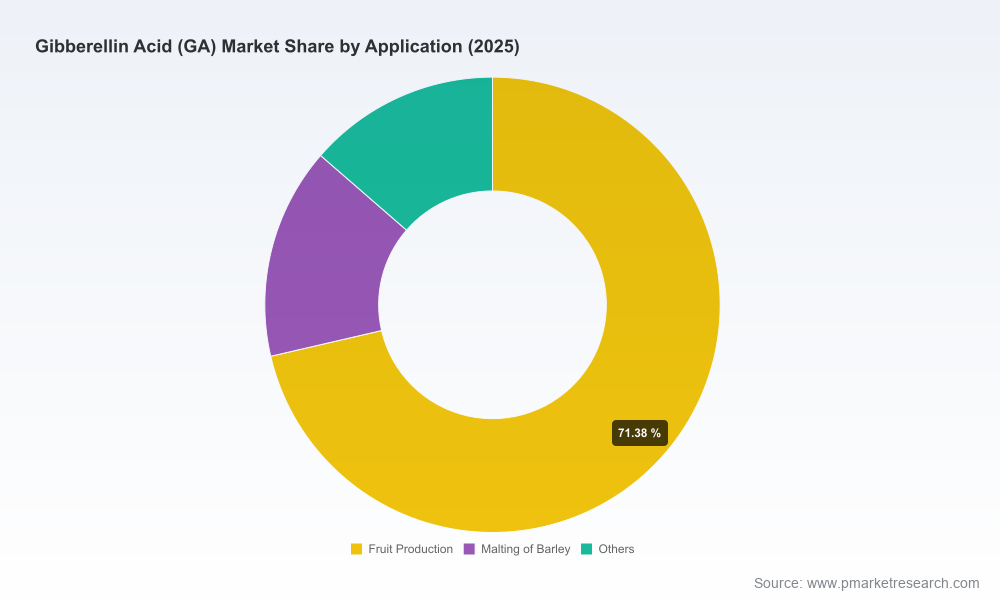

Gibberellin Acid (GA) Market — 2026 Strategic Outlook (PW Consulting)

PW Consulting today releases a strategic briefing drawn from our full Gibberellin Acid (GA) Market study (base year 2025), designed to equip senior executives, investors, product leaders, and policy teams with the actionable intelligence they need to make high‑stakes decisions through 2026 and beyond. The study synthesizes historical performance (2020–2025), a robust forecast window (2026–2032), regulatory scans, supply‑chain stress tests, and competitor playbooks to translate market signals into board‑level options.

Gibberellin Acid (GA) Market

Market Momentum: What the headline figures mean for strategy

After a steady recovery and expansion during 2020–2025, the global GA market moved from a mid‑seven‑hundred million USD base in 2020 to just under one billion USD in 2025 (USD, Million). Our forecast projects continued growth at a compound annual growth rate of 8.15% across 2026–2032, with the total market crossing the billion‑dollar threshold early in the forecast window and approaching the high‑single‑billion range by the end of the period. These headline dynamics point to a structurally growing market driven by product innovation, faster adoption in high‑value crop applications, and improving production economics.

Gibberellin Acid (GA) Market

From a strategic perspective, the trajectory and growth rate establish three interrelated imperatives for 2026 decisions: accelerate product‑market fit for differentiated formulations; harden supply chains to capture rising demand; and align regulatory and go‑to‑market strategies to benefit from premium positioning (organic/OMRI listings, low‑volatility formulations, extended shelf‑life claims).

Gibberellin Acid (GA) Market

Why 2026 is a pivotal year — regulatory and production inflection points

- Regulatory cadence: The EU renewal process and U.S. regulatory listings active through 2025–2026 have clarified allowable use patterns and labeling expectations for gibberellins. Notably, recent official entries in regulatory repositories have reduced legal ambiguity for mainstream formulations, but they also raise compliance costs for novel claims and formulations.

- Product innovation accelerating commercialization: Commercial launches in 2025 illustrate a shift toward low‑volatility, crop‑specific formulations with organic/OMRI support. These introductions compress time‑to‑value for differentiated SKUs that can command higher margins if supported by field data and retailer endorsement.

- Manufacturing efficiency: Adoption of optimized fermentation and probiotic‑assisted processes in late 2025 drove a meaningful step‑change in production cost — our analysis flags nearly single‑digit percentage cost reductions at commercial scale. That margin expansion is a window for price competition or reinvestment into R&D and channel development.

Report composition — practical, transaction‑ready outputs

The full PW Consulting report is deliberately operational. It is structured to convert market insight into executable plans and includes:

- Detailed market sizing and a transparente forecasting model (2026–2032) with scenario toggles for commodity feedstock shocks, accelerated regulatory constraints, and premium formulation adoption rates.

- A modular commercial playbook offering go‑to‑market templates for incumbents and new entrants: pricing architecture, channel segmentation, and distributor incentive frameworks.

- Regulatory matrix and labeling risk register that cross‑references major jurisdictions and maps mitigation actions for claim substantiation, residue monitoring, and organic listing pathways.

- Supply‑chain heatmaps and stress tests identifying single‑point vulnerabilities in bulk GA supply and formulation intermediates; alternative sourcing options and contract‑structuring templates are provided.

- Competitor profiles, product portfolios, and capability diagnostics for leading manufacturers and formulators — structured to support M&A target screening, JV assessments, and alliance negotiations.

- Investment and M&A playbooks, including valuation sensitivity tests, deal structuring considerations, and integration checklists tailored to the GA value chain.

Competitive landscape — strategic takeaways

The GA market remains commercially attractive but structurally fragmented. Our concentration analysis shows that the top three and five players do not dominate the market to the degree seen in many agrochemical categories, creating runway for consolidation, premium niche plays, and regional specialists to win share.

- Major multinational formulators (e.g., established global agrochemical firms): These firms bring broad channel access, regulatory teams, and brand recognition. Their strategy will be to expand high‑value formulations, secure OMRI/organic designations where possible, and leverage distribution scale to accelerate adoption.

- Specialist manufacturers (bulk producers in Asia): Lower‑cost bulk producers with large fermentation capacity are well positioned to supply intermediates and commodity GA3. Their commercial advantage is cost competitiveness, but they face margin pressure if differentiation on formulation and regulatory support is required.

- Turf, aquatic and niche application suppliers: Firms focusing on turf, ornamentals, and aquatic management commercialize differentiated formulations that capture higher ASPs (average selling prices) through performance guarantees and service contracts.

- Recent product entrants: The 2025–2026 product introductions emphasize the market’s tilt toward stabilized, low‑volatility formulations and organic‑eligible claims — these entrants are accelerating the timeline for premiumization in certain crop verticals.

For dealmakers, the combination of fragmented concentration metrics and improving production economics presents a classic roll‑up opportunity for firms that can integrate procurement, regulatory capabilities, and route‑to‑market execution. For incumbents, defensive bolt‑on acquisitions focused on formulation IP and channel reach are likely to deliver faster synergies than greenfield expansion.

Actionable recommendations by stakeholder

- For agrochemical incumbents: Prioritize rapid commercialization of differentiated low‑volatility/extended‑shelf formulations and invest in field trials for premium crops. Lock long‑term supply contracts with bulk producers, and create co‑development agreements to secure innovation pipelines.

- For new entrants & startups: Focus initial efforts on niche, high‑margin applications (e.g., specialty horticulture, turf) where clinical data and channel partnerships can justify a premium. Consider contract manufacturing partnerships rather than CAPEX‑heavy production buildouts.

- For private equity and strategic investors: Target consolidation plays that combine supply cost advantage with formulation capability and distribution reach. Use scenario models that stress test regulatory tightening and raw material shocks to set realistic IRR thresholds.

- For regulatory & compliance teams: Accelerate dossier preparation for major jurisdictions and plan label harmonization early. OMRI and organic‑compatible claims deliver outsized retail value in certain markets — make these a priority where feasible.

- For agribusiness and grower networks: Negotiate performance‑based procurement contracts and deploy agronomic trials to document yield and quality gains. Consider supplier partnerships that bundle product with crop management advisory to capture margin uplift from value‑added services.

Why PW Consulting — how we convert insight into outcomes

PW Consulting’s report goes beyond conventional market forecasts. We combine a suite of deliverables that are adoption‑focused: interactive forecast models, playbooks, supplier scorecards, regulatory checklists, and a prioritized pipeline for R&D and field demonstration. Where boards need immediate options, we deliver scenario‑tested entry plans and a short list of M&A targets with integration blueprints.

Importantly, this release follows a “trailer” approach — we intentionally showcase strategic framing and high‑confidence signals while reserving the detailed sub‑segment and pricing matrices for the full report and tailored advisory engagements. That ensures readers get the directional clarity needed to act now, while the complete dataset supports execution and negotiation.

Next steps — how to use this briefing in 90 days

- Commission a rapid supplier due‑diligence using our template to validate contract exposure and alternative sourcing routes.

- Initiate two parallel pilots: (1) a formulation trial in a prioritized high‑value crop and (2) a channel test with a strategic distributor offering co‑marketing support.

- Update the regulatory roadmap to reflect recent EU renewals and U.S. listings, and budget for label rework and residue testing where necessary.

- Run a deal‑screening session using our M&A filters to identify 3–5 targets aligned with your scale and margin objectives.

For decision teams that need the full analytical annex, raw data files, and competitor scorecards — including the granular segmentation tables and valuation models — PW Consulting offers the complete report and bespoke advisory packages to translate insights into executable deals and commercial plans. Contact our team to schedule a briefing and secure the dataset that supports transaction‑grade decisions.

PW Consulting — translating market momentum into decisive, defensible strategy for the Gibberellin Acid market as firms plan for 2026 and the next growth cycle.

For detailed analysis of this topic, please visit the official page:Gibberellin Acid (GA) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com