Wireless Occupancy Sensor Market Insights and Growth Trends

Other |

2026-06-25 09:26:40

PW Consulting today publishes an executive-level industry brief accompanying our full market study, PID Sensors and Detectors Market — Base Year 2025. The brief synthesizes high-conviction implications for corporate strategy in 2026 while showcasing the empirical backbone and tactical outputs of the full report. Executives evaluating product roadmaps, M&A targets, channel strategies, or capital allocation for environmental and industrial-safety sensor portfolios will find immediate, actionable guidance — and a clear path to the underlying data and vendor scorecards via our report portal.

PID (Photoionization Detection) Sensors and Detectors Market

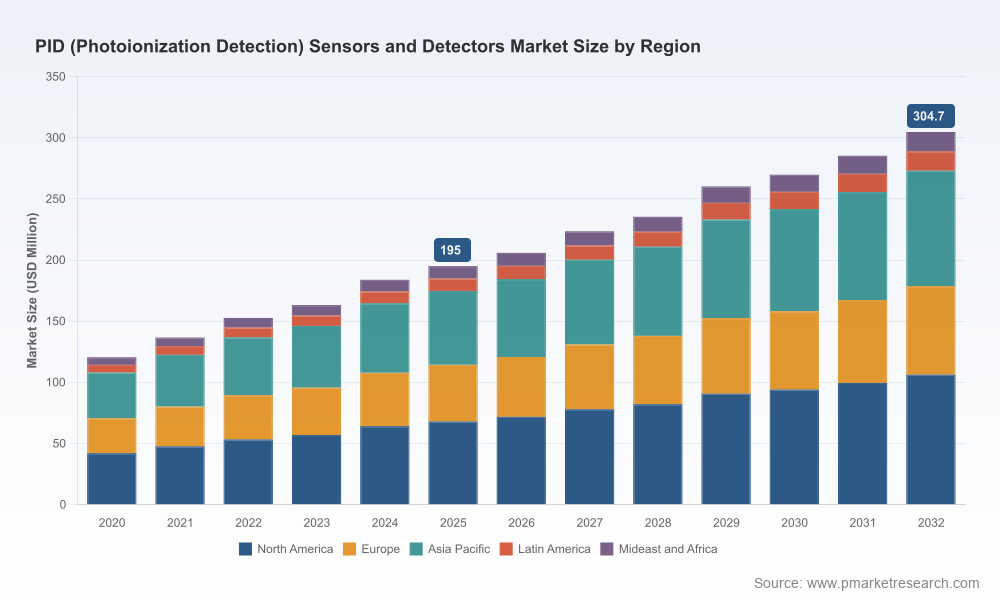

Our base-year analysis (2025) and forward-looking model through 2032 show a durable expansion in PID sensors and detectors, underpinned by a combination of tightening VOC regulations, renewed investment in remote environmental monitoring, and technical advances that push detection limits toward ppb sensitivity with lower power budgets. The market measured USD Million 195.0 in 2025 and is projected to grow at a 6.5% CAGR across 2026–2032 to reach approximately USD Million 304.7 by 2032. That trajectory reflects a blended demand response across portable, fixed, and handheld segments and across environmental monitoring and industrial safety end markets.

PID (Photoionization Detection) Sensors and Detectors Market

Two structural facts matter for 2026 decision-making: (1) growth is steady rather than hyperbolic, favoring disciplined, ROI-focused investments; and (2) the market remains moderately consolidated — our concentration analysis shows the top-three suppliers control 35.5% of the market, and the top-five suppliers control 52.8% — creating an environment where technology differentiation and channel reach deliver disproportionate value.

PID (Photoionization Detection) Sensors and Detectors Market

Timing: 2026 is a pivot year for many industrial and environmental programs that moved from pilot to scale between 2022–2025. Procurement cycles and calibration infrastructure investments committed in 2026 will determine realized market share through the subsequent three-year window.

Regulatory inflection points: New enforcement emphasis on VOC exposure limits and EU REACH/CLP implementations are accelerating demand for validated PID solutions for compliance monitoring.

Technology thresholds: Achieving ppb sensitivity with acceptable battery life is a gate condition for many portable and handheld deployments. Companies that solve the power–sensitivity trade-off will win the largest upstream procurement deals in 2026–2028.

The full PW Consulting report is designed as a decision-support toolkit for CXOs, product leaders, and corporate development teams. It contains the following practical modules:

Market model and scenario suite — multi-year, bottom-up demand models with sensitivity runs for regulatory tightness, oil & gas CAPEX cycles, and industrial automation adoption rates. (Summary figures are included in this brief; the full model and underlying assumptions are available in the paid report.)

Vendor performance scorecards — a standardized assessment across technology robustness, sensor-to-sensor repeatability, lamp life, supply-chain resilience, and aftermarket serviceability.

Go-to-market playbooks — segment-specific pricing and packaging strategies for OEMs, integrators, and instrument manufacturers, including channel-refresh timetables for handheld, portable, and fixed units.

Calibration & validation protocols — operational checklists and ISO 17025 alignment guidance for laboratories and field service teams responsible for PID detector validation.

Technology roadmap and component sourcing matrix — priorities across lamp technology, UV sources, low-power electronics, and MEMS integration, and supplier risk maps for critical subcomponents.

Use-case ROI models — templated calculations for total cost of ownership (TCO), payback timelines, and value capture in compliance monitoring, leak detection, and real-time plume tracking.

M&A and partnership framework — a repeatable scoring methodology for target screening, and a shortlist of archetypal targets by capability (sensor IP, production scale, channel reach) together with integration playbooks.

The PID landscape is led by several specialized players with distinct go-to-market approaches and technical emphases. Our competitive analysis synthesizes public information, primary interviews, and technical benchmarking to map strengths and strategic gaps.

ION Science Ltd (Fowlmere, UK) — established as a market anchor with a broad OEM client base and a growing portfolio of integrated detectors. Their ION SENSE brand and recent ARA-X4 multi-gas detector introductions signal a focus on platform consolidation and compliance-grade performance.

Alphasense (Chorleywood, UK) — investing in sensor repeatability and lamp-life improvements through its PIDX series. For OEMs prioritizing replacement compatibility and long-term calibration stability, Alphasense is a strategic supplier.

AMETEK MOCON (Brooklyn Park, MN, USA) — pursues a product-led strategy emphasizing accuracy and field usability, exemplified by the piD-TECH eV-NXT and eVx sensor lines. Recent launches reinforce their position in industrial-safety and environmental segments.

PID Analyzers, LLC / HNU — focused on niche analytical applications across air, water, and process analytics, offering integrated systems for laboratory and field workflows.

RKI Instruments and WatchGas — arrayed toward portable and multi-gas detection devices, integrating PID capabilities into broader gas-sensing platforms targeted at first responders and industrial mobile teams.

Strategic implication: competing purely on cost is a weak value proposition. Successful vendors combine demonstrable detection performance, lifecycle calibration economics (fewer field recalibrations), and channel-service networks that can execute ISO 17025-aligned validation. The concentration metrics above mean that scale advantages are meaningful, but not insurmountable for specialists with strong technology differentiation.

Regulation: Updated VOC exposure guidelines and enforcement activity in multiple jurisdictions are increasing the use of PID detectors for compliance duties rather than purely for safety or process optimization. Buyers will prioritize validated, auditable detection stacks that integrate with compliance workflows.

Standards & Calibration: The rising importance of ISO 17025 accreditation for calibration labs elevates the commercial value of vendor-supplied calibration services and portable verification kits.

Power and sensitivity trade-offs: Achieving ppb-level sensitivity while maintaining battery life for portable and handheld units remains a key technical challenge. Solutions that pair advanced lamp lifetimes with low-power analog/digital front ends will capture the growing field-installed base.

Infrastructure integration: Remote monitoring architectures in oil & gas and chemical plants increasingly embed PID sensors into IoT telemetry stacks to enable real-time plume tracking and predictive maintenance. Interoperability and secure telemetry are now procurement prerequisites.

Based on our scenario modeling and supplier assessments, PW Consulting recommends the following near-term actions for executive teams:

Re-baseline product roadmaps for calibration economics — prioritize sensor technologies and service models that reduce lifetime calibration costs by at least one re-calibration cycle compared to incumbent designs.

Invest in compliance-first features — audit trails, tamper-evident calibration flows, and interoperability with centralized compliance platforms will accelerate enterprise procurement approvals.

Pursue targeted partnerships — specialist vendors (detection IP) plus systems integrators (telemetry, analytics) create value faster than organic scale in many geographies.

Screen M&A targets with a two-axis view — technology defensibility and channel penetration — and apply our scorecard methodology to prioritize diligence targets that close at least one critical capability gap.

Plan pilots with scaled validation — design pilots that include ISO 17025-aligned calibration lab sign-offs and operational acceptance criteria tied to business KPIs (e.g., % reduction in undetected VOC events).

The full PID Sensors and Detectors Market report operationalizes the guidance above: it converts strategic imperatives into executable plans — with vendor-specific recommendations and financial impact estimates. We provide procurement-ready RFP language for OEM and system integrator sourcing, detailed TCO templates for capital and service decisions, and a prioritized action matrix for 90-, 180-, and 365-day initiatives.

Importantly, this brief follows a “trailer” approach: it demonstrates the empirical rigor and the practical relevance of our work while withholding the granular proprietary segmentation and price-by-region tables that are included in the full report. Those detailed datasets are intentionally gated to ensure confidentiality of primary-source inputs and to preserve the actionable advantage for report subscribers.

For 2026 strategy planning, PW Consulting recommends securing the full report to access the complete market model, supplier scorecards, and the M&A screening toolkit. Organizations that adopt the report’s pragmatic playbooks will be able to make faster, evidence-backed decisions about product investments, partnership structures, and acquisition targets.

Visit the PW Consulting report page to download the executive summary and to request the full PID Sensors and Detectors Market study, including the editable model and vendor benchmarking appendices. Our analysts are available for briefings and for tailored advisory work to embed the findings into your 2026 corporate planning cycle.

For detailed analysis of this topic, please visit the official page:PID (Photoionization Detection) Sensors and Detectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com