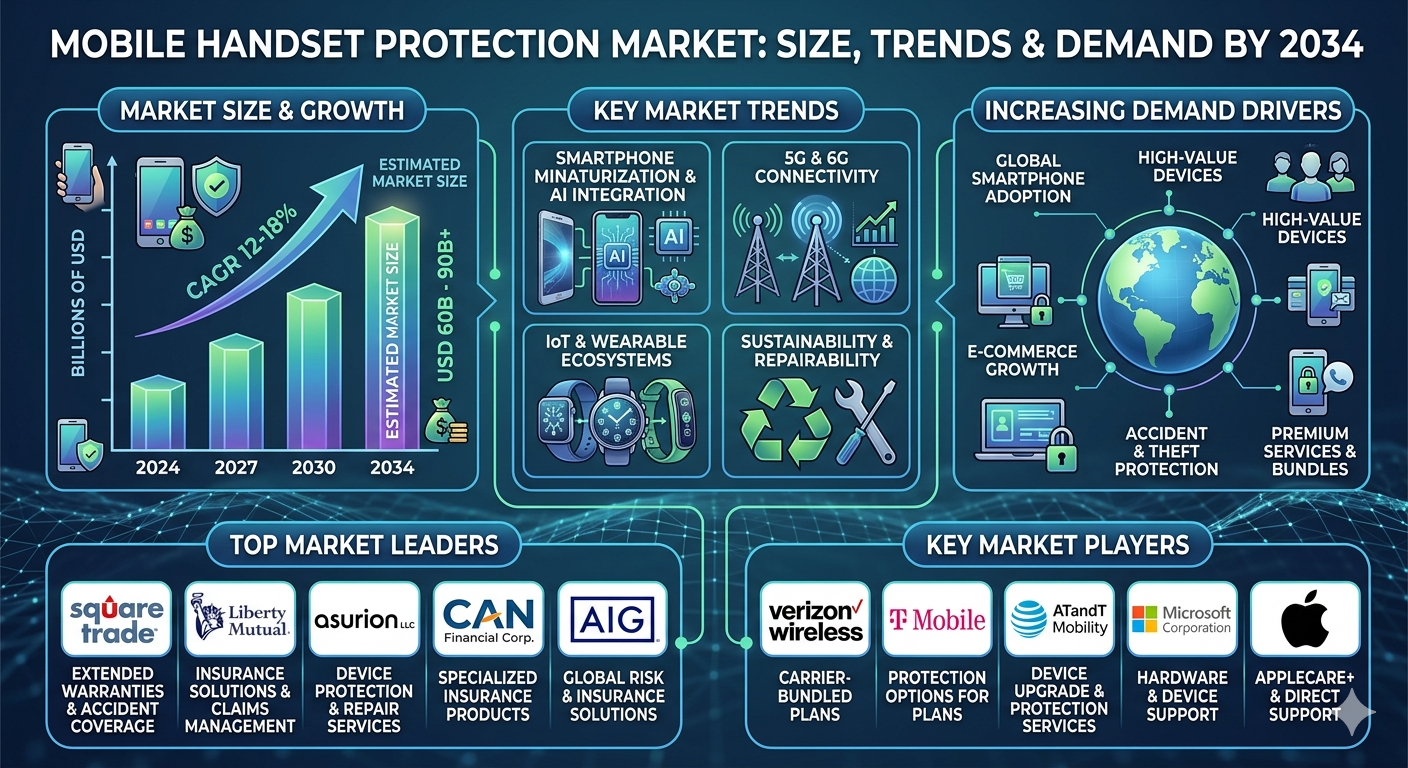

Mobile Handset Protection Market Growth in North America Driven by Premium Smartphones

Other |

2026-06-06 09:08:16

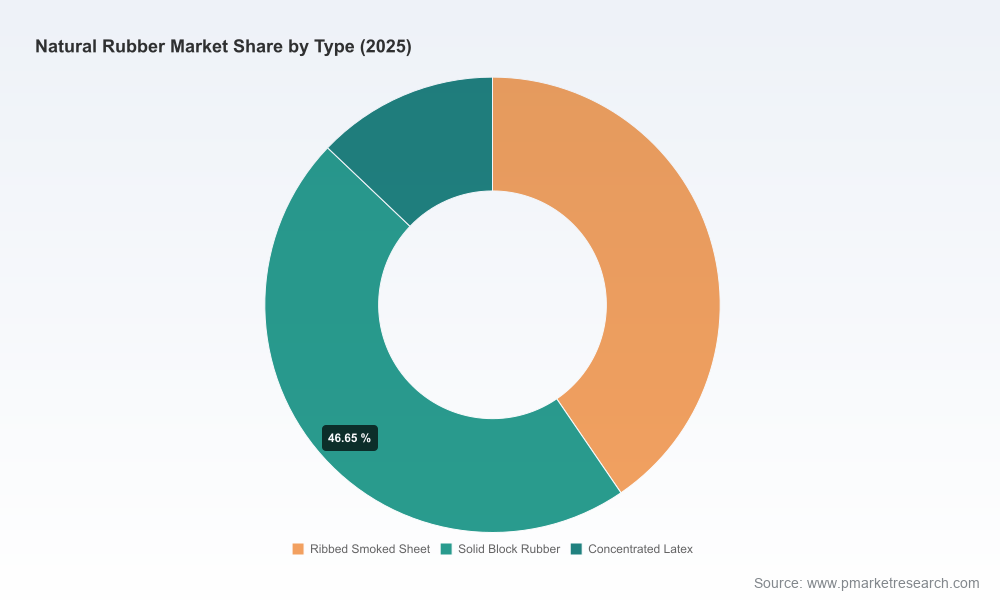

PW Consulting’s Natural Rubber Market report (base year 2025) delivers a forward-looking, decision-ready blueprint for executives, procurement officers, investors and policy teams facing an increasingly complex raw-material environment in 2026. After a multi-year recovery through the 2020–2025 historical window, the global natural rubber market recorded a material expansion into 2025 (base-year revenue: USD 215.0 Million). Our forecast horizon (2026–2032) projects continued expansion at a compound annual growth rate (CAGR) of 5.86%, with the market approaching the mid-2030s with materially higher revenue run-rates. The market remains meaningfully concentrated (CR3 ~68.2%; CR5 ~78.4%), a structural fact that amplifies the strategic importance of supplier relationships, traceability and risk mitigation in 2026.

Natural Rubber Market

2026 is a hinge year. Macro demand fundamentals remain firm: independent supply-demand monitoring indicates the natural rubber market continues to exhibit a persistent structural gap between production and consumption. That gap — together with acute weather risks and regulatory tightening — will shape pricing and availability for most buyers. Recent and queued regulatory developments, notably the EU Deforestation Regulation requiring demonstrable, plot-level traceability and legal compliance from the end of 2026, will force operational and capital choices for large downstream operators.

Natural Rubber Market

Operationally, two types of shocks dominate our risk analysis for 2026. First, physical supply shocks have become more frequent: flooding events in southern Thailand during 2025–2026 have been reported to potentially reduce regional output by a very large amount, directly pressuring global availability and creating immediate sourcing stress for downstream industries. Second, policy shocks — led by EUDR and emerging national-level sustainability programmes (for example, India’s iSNR initiative aimed at aligning domestic production with international sustainability standards) — are converting supply-chain transparency from “nice to have” into a contractual requirement. Together, these forces are increasing short-term price volatility while elevating the long-term enforcement costs of non-compliance.

Natural Rubber Market

The market concentration metrics underscore why the actions of a few large processors and exporters matter to buyers worldwide. Leading processors and exporters are taking differentiated strategic approaches:

For buyers, this landscape means counterparty selection cannot be treated as a pure price exercise in 2026. Scale suppliers will increasingly be preferred partners for compliance-heavy buyers, while specialized suppliers will command premiums for quality and reliability under stress.

Our modelling combines a top-down market-sizing framework (historical 2020–2025 trends validated against industry sources) with a bottom-up supply-chain build that quantifies exposure by corridor, product grade and counterparty risk band. The integrated model produces scenario outputs keyed to three strategic decision levers: sourcing strategy (diversify vs. concentrate), compliance investment (traceability vs. insurance), and capacity strategy (build vs. partner). We translate these model outputs into executable roadmaps, specifying timing, budget envelopes and KPIs for 12–24 month implementation cycles — enabling procurement and executive teams to move from strategy to contracts within a single planning cycle.

2026 is not just another planning year — it is the year that regulatory imperatives, concentrated supply dynamics and acute weather risks converge to make sourcing choices irreversible and expensive if mishandled. Companies that treat traceability and supplier resilience as embedded business capabilities (rather than compliance checkboxes) will secure privileged access to regulated markets, stabilise margins and protect brand equity. Conversely, delayed action will amplify supply-disruption costs, accelerate margin erosion and increase capital expenditures under duress.

This release deliberately showcases our analytical depth while reserving the detailed segmentation tables, supplier-level exposure matrices and our proprietary pricing curves for subscribers. These datasets contain the granular regional, product-type and application breakdowns that drive tactical contracting and investment decisions — and they are available through the full report and interactive client portal. For procurement directors and strategy teams preparing 2026 budgets and contracts, accessing the full dataset is essential to operationalise the playbook above.

PW Consulting’s Natural Rubber Market report is built to be both predictive and prescriptive: it tells you what is likely to happen, who will be most affected, and exactly how to reposition procurement, manufacturing and investment programs to capture advantage in 2026 and beyond. Contact PW Consulting to request the full report, supplier-level exposures, and scenario toolkits that will convert market intelligence into executable strategy.

For detailed analysis of this topic, please visit the official page:Natural Rubber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com