Transformative Research Applications Strengthening the Cell Culture Market Outlook

Health |

2026-06-03 14:50:43

PW Consulting today releases its executive briefing for the Metallocene Polyethylene (mPE) market — a focused, decision-grade companion to our full market research report. Anchored on a 2025 base year and a 2026–2032 forecast horizon, the study quantifies a resilient market trajectory (2026–2032 CAGR: 6.8%) and positions that growth within the shifting dynamics of raw material availability, regulatory pressure, and concentrated supplier capacity. What follows is a high-fidelity preview of the strategic conclusions, operational implications, and tactical playbooks contained in the full report. Per our “trailer” approach, we deliberately summarize insights while withholding detailed subsegment metrics — readers wishing to operationalize these findings should consult the full report for granular regional, type and application splits.

Metallocene Polyethylene Market

Timing investment: Capital allocation windows are narrow. The market projection from 2025 through 2032 indicates a material expansion in demand and value capture that requires timely capacity, technology or offtake decisions.

Metallocene Polyethylene Market

Feedstock and margin management: Large ethylene capacity additions globally are reshaping feedstock cost curves and supplier bargaining power — procurement strategies must adapt to capture margin opportunity.

Metallocene Polyethylene Market

Product differentiation & access: Metallocene grades are no longer niche; new grades and specialty blends are redefining premium positioning across flexible films, industrial applications and emerging automotive uses.

Regulatory and sustainability alignment: Regional policy and compliance frameworks are creating both constraints and pathways for market access — companies that align early with evolving standards secure pricing and share advantages.

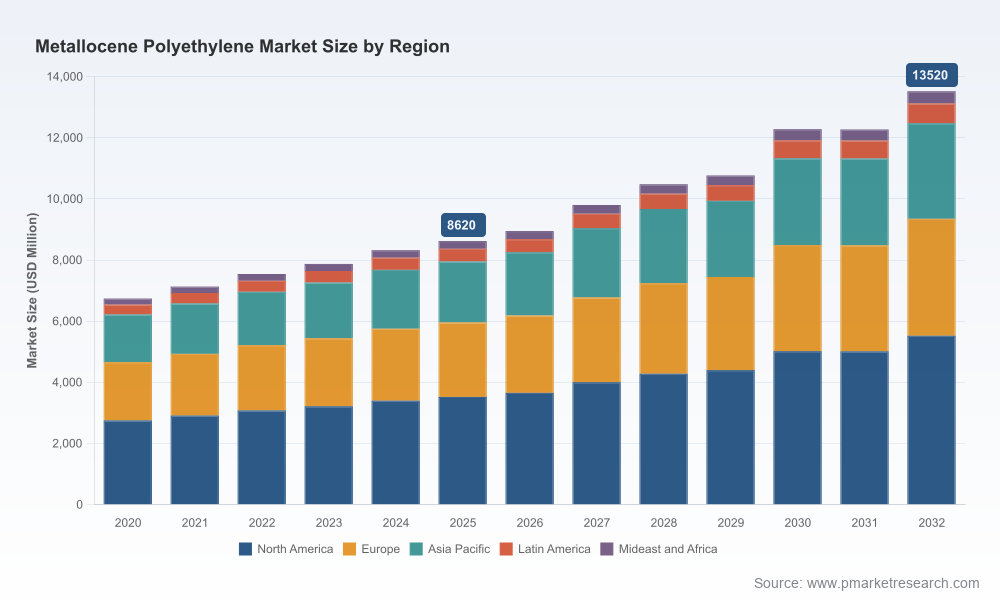

Our base-year calibration and historical window (2020–2025) show consistent expansion in overall market value, with the market moving into a new growth phase as major capacity projects come online and demand adoption for higher-performance metallocene grades accelerates. The forecast period (2026–2032) projects growth at a compound annual growth rate of 6.8%, reflecting a combination of sustained end-market uptake and structural changes on the supply side. The market is materially concentrated at the top, with the three- and five-firm concentrations reflecting significant incumbent influence — an important consideration for entrants and downstream buyers evaluating negotiation leverage and long-term offtake security.

Capacity expansion and re-shoring dynamics: Several large producers have announced or commissioned significant new mPE-capable capacity. These projects are shortening lead-times for high-spec grades and enabling integrated feedstock-to-resin platforms in targeted regions.

Feedstock tailwinds: Global ethylene capacity additions have materially improved feedstock availability and regional pricing dynamics, creating opportunities for margin recovery and competitive pricing strategies for producers that optimize crackers and downstream assets.

Technology and grade diversification: Advances in catalyst and reactor designs continue to broaden the performance envelope of metallocene-based resins — producers are launching product lines tailored to stretch film, breathable films, automotive interior components, and specialty rotomolding segments.

Regulatory shaping of production footprint: Environmental compliance standards and regional packaging regulations are influencing siting decisions, permitting timelines and technology choices — companies with experience navigating single-site catalyst technology compliance are advantaged.

Market leadership is held by a small set of global and regional players that combine technology portfolios with integrated value chains. Our review highlights four strategic archetypes exhibited by leading firms:

Integrated petrochemical majors expanding capacity and product suites — exemplified by a recent large-scale LLDPE unit that includes metallocene capability, which materially expands high-performance resin supply for packaging and automotive applications.

Specialty polymer platforms launching differentiated metallocene grades for targeted end-uses — recent product introductions focus on high-performance automotive and FMCG flexible packaging where property differentiation drives premium realization.

Regional capacity build-outs aligned to local regulations and market access — new facilities in Southeast Asia reflect a strategy to capture fast-growing flexible film demand while meeting tighter environmental and packaging standards.

Fast-follower regional producers releasing application-focused grades to protect share in consumer goods packaging and niche industrial markets.

Recent industry moves underscore these dynamics: a major producer initiated operations at a substantial LLDPE unit with metallocene capability in mid‑2025; another global producer unveiled a new Southeast Asian metallocene facility in late 2025 to enhance regional supply; leading firms have followed with targeted product launches in late 2025 and 2025–2026 that push metallocene into higher-value automotive and FMCG segments. These actions compress the window for new market entrants and raise the bar for differentiation.

The full PW Consulting report is intentionally operational. It includes:

Detailed market sizing and validated historical series (2020–2025) and scenario-anchored forecasts (2026–2032) with upside/downside cases for demand, price and margin evolution.

Supply-demand balances by region and by application with sensitivity to raw material shocks and policy shifts.

Commercial playbooks: go-to-market options for producers and traders, channel economics for film converters, and margin improvement initiatives for brand owners using mPE.

Investment decision frameworks: timing matrices for new capacity, payback sensitivities, and alternative CAPEX deployment paths (brownfield expansion vs. greenfield vs. tolling/contract manufacturing).

Procurement and hedging tools: recommended sourcing mixes and tactical hedging templates calibrated to the evolving ethylene landscape.

Regulatory and sustainability checklists linked to regional compliance regimes and certification programs relevant to flexible films and packaging.

Competitor benchmarking dashboards and M&A screening lists identifying strategically complementary targets and likely divestiture candidates.

Validate capacity timing: Re-run internal volume forecasts against our scenario models to determine whether to accelerate, delay or stagger expansion tranches.

Lock feedstock advantage: Use our feedstock-cost curve analysis to negotiate multi-year ethylene and feedstock contracts that protect margins during the next two cyclical turns.

Prioritize product differentiation: Invest selectively in grades that enable premium positioning (e.g., breathable film, high-clarity automotive interior grades) and align commercial teams to sell property-driven value.

Operationalize sustainability compliance: Map product portfolios to regional packaging and environmental standards and prioritize investments that reduce lifecycle impacts and simplify qualification for brand customers.

Design flexible offtake and tolling arrangements: Where balance-sheet capacity is constrained, structure tolling or joint-venture arrangements to secure a share of incremental demand.

Pursue targeted M&A and alliance plays: Use our screening to identify targets that fill technical gaps, accelerate market entry, or provide attractive feedstock/technology integration.

Feedstock volatility tied to upstream ethylene project realization or delays.

Regulatory tightening around single-use packaging in several jurisdictions which may accelerate demand shifts toward recyclable or compostable solutions.

Rate and timing of technology adoption — faster roll-out of next-generation catalysts or compounding technologies could reprice certain grade categories.

Competitive response dynamics as incumbents deploy integrated pricing or long-term offtake agreements to protect share.

Our analysis uses a blended approach: primary interviews with producers, converters and major brand procurement leads; bottom-up supply modeling from announced and commissioned plants; trade-flow reconciliation; and price series analysis tied to regional cost-to-serve assumptions. The study’s base year is 2025 with a validated historical series covering 2020–2025 and an explicit forecast period from 2026–2032. Financial references in the report are presented in USD (Million) and are accompanied by sensitivity tables that allow readers to stress-test assumptions. Note: consistent with this briefing’s purpose, we have intentionally omitted granular regional and application-level splits here — those datasets are included in the full report to enable transaction-level decision making.

The metallocene polyethylene market is entering a formative phase where supply additions, raw material dynamics and targeted product launches will determine winners and losers. For executives considering capital projects, procurement redesigns, or M&A activity in 2026, actionable intelligence and timing are everything. PW Consulting’s full report provides the scenario tools, supply-demand mechanics, and commercial playbooks required to convert opportunity into durable value. To access the full dataset, regional and application splits, and our proprietary decision frameworks, please consult the complete Metallocene Polyethylene Market report on the PW Consulting publications portal.

For detailed analysis of this topic, please visit the official page:Metallocene Polyethylene Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com