Electric Vehicles and Fuel Cell Vehicles Market — Strategic Outlook for 2026: Key Takeaways from PW Consulting’s Market Report

Executive summary

PW Consulting’s latest Electric Vehicles and Fuel Cell Vehicles Market report (base year 2025) provides a forward-looking, decision-focused assessment designed explicitly for executives shaping 2026 strategies. The market reached approximately USD 215.0 Billion in our base year and is forecast to expand to about USD 238.2 Billion in 2026. With a compound annual growth rate of 14.06% across our 2026–2032 forecast horizon, the sector is projected to exceed half a trillion USD by 2032, underscoring the scale and urgency of strategic moves now.

Electric Vehicles and Fuel Cell Vehicles Market

Historical performance (2020–2025) shows a market that is both resilient and dynamic: pockets of temporary downturn were rapidly recovered through renewed investment, product launches, and policy-driven demand. Yet beneath headline growth lies a fragmented competitive structure, where the leading OEMs and component specialists together capture roughly one quarter of total market revenue — signalling substantial opportunity for challengers, niche suppliers, and new vertical integrators.

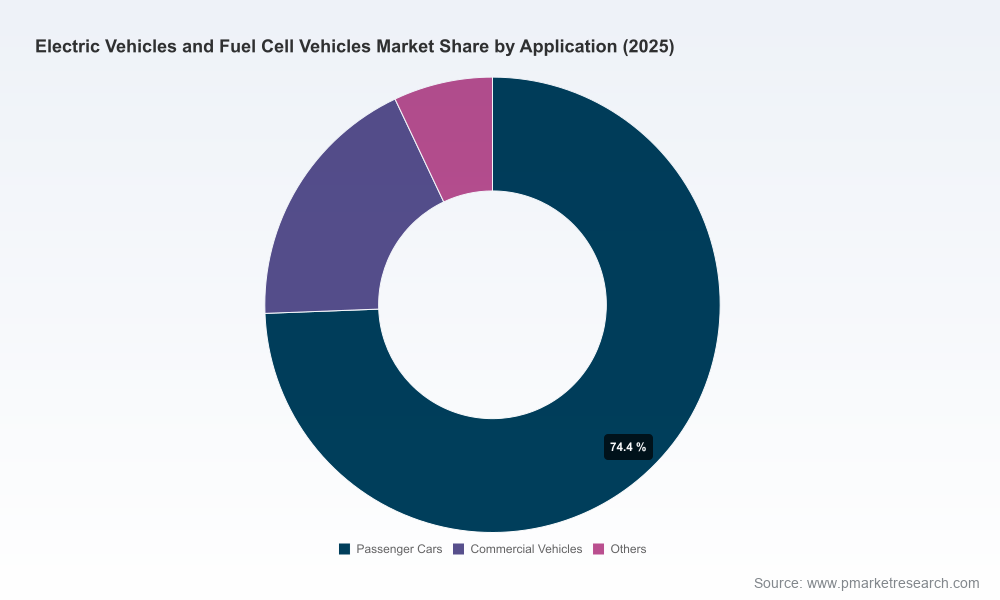

Electric Vehicles and Fuel Cell Vehicles Market

Why this report matters for 2026 decision-making

- Prioritization of capital: Our financial model translates market trajectories into capital need windows by vehicle architecture and value chain node, so CFOs can align 2026–2027 CAPEX with realistic adoption curves.

- Product roadmap alignment: R&D leaders will find timing guidance for when fuel cell value propositions (range, refuel time, total cost of ownership) become competitive versus battery alternatives for specific use cases.

- Partnership and M&A playbooks: The report identifies where inorganic moves accelerate access to critical technologies (fuel cell stacks, catalysts, hydrogen logistics) and where organic capability building is preferable.

- Procurement and supply-chain playbook: Practical levers to mitigate raw-material and component volatility — including modular sourcing templates and contract structures — are provided for procurement teams planning 2026 commitments.

- Regulatory and commercial risk calibration: We map policy-imposed timing and pricing pressure points which materially affect 2026 product positioning and go-to-market choices.

What the report delivers — operational, executable intelligence

- Proprietary market sizing and bottom-up revenue model (USD Billion), calibrated to base year 2025 and rolled forward with scenario-adjusted CAGR assumptions.

- Three detailed 2026–2032 scenarios (Baseline, Accelerated Adoption, Infrastructure-Constrained) with implications for unit volumes, OEM margins, and supplier revenue pools.

- Technology readiness assessments for battery electric vehicles (BEV), fuel cell electric vehicles (FCEV), and hybrids — including maturity curves for stack durability, system integration, and catalyst substitution paths.

- Cost-curve analysis and sensitivity testing tied to key external levers (platinum-group metal costs, hydrogen production cost, cell manufacturing scale).

- Supplier and partner ecosystem maps with capability heatmaps and suggested engagement templates for strategic alliances, JV structures, and minority investments.

- Investor-grade financial templates and an M&A diligence checklist tailored to mobility and hydrogen ecosystem assets.

- A practical pilot-evaluation toolkit for fleet operators and municipal buyers to assess TCO and operational constraints at the tender and deployment stages.

Competitive landscape — what recent moves tell us

The competitive field is dynamic: incumbent OEMs are moving from proof-of-concept to production-readiness while component specialists commercialize enabling subsystems.

Electric Vehicles and Fuel Cell Vehicles Market

- Toyota Motor Corporation (Toyota City, Japan) — Toyota’s announcement of a third‑generation fuel cell system with improved durability signals a strategic bet to broaden fuel cell applicability across passenger, commercial, and heavy-duty segments. For firms evaluating partnerships, Toyota’s technology trajectory suggests a focus on scalable, durable modules that reduce integration risk.

- Hyundai Motor Company (Seoul, South Korea) — Hyundai’s refreshed Nexo and expanded truck/bus fuel cell programs reflect a dual-pronged strategy: capture Asia‑Pacific and global fleet opportunities while using heavy-duty platforms as technology accelerators for cost reduction.

- Honda Motor Co., Ltd. (Tokyo, Japan) — Honda’s start of U.S. production for a plug-in FCEV demonstrates a localization play that reduces trade exposure and shortens time-to-fleet for North American buyers. OEMs and suppliers should expect increased pressure to localize key assemblies where demand density justifies it.

- BMW AG (Munich, Germany) — BMW’s planned series-production FCEV (targeted for later in the decade) underscores continued cross‑OEM collaborations; this is an example of volume-risk sharing where cost per unit can be materially lowered through shared platforms.

- Nippon Shokubai Co., Ltd. (Tokyo, Japan) — Advanced, platinum-group-metal-free catalyst developments highlight the upstream innovation that can materially change FCEV economics, particularly for light- and heavy-duty applications.

- Adjacent supply moves — Purem by Eberspaecher — Expanded hydrogen recirculation blowers and fuel cell system portfolios indicate suppliers are building integrated subsystem offerings to simplify OEM adoption and accelerate time-to-market.

Industry dynamics driving 2026 strategic choices

- Policy shifts: Stricter CO2 standards in markets such as the EU have acutely increased pressure on manufacturers to field more affordable electrified models, including FCEV variants, which alters pricing and portfolio strategies.

- Macro adoption: Global electric car sales hit a record in 2025, with over 20 million units sold — lockdown-level adoption rates that change consumer expectations and dealer network economics.

- Cost and infrastructure targets: Public targets, such as efforts to reduce fuel cell costs toward long-term DOE benchmarks and hydrogen production cost targets, create definable check-points for investment staging. These targets are critical inputs to our scenario timelines.

- Demand signals and early churn: Some mature markets are already showing mixed signals — for example, a recent decline in annual FCEV registrations in a major U.S. state — indicating that deployment is sensitive to local refuelling availability and policy incentives.

Strategic implications and 2026 playbook

- OEMs: Use a hybrid approach to R&D and commercialisation — accelerate fuel cell pilots where infrastructure rollout is imminent, and prioritize BEV expansion where charging density and lower TCO are established. Consider platform-sharing and co‑development to derisk scale-up.

- Tier-1 suppliers & component specialists: Focus on modular subsystems and standardized interfaces to capture OEM mindshare. Investment in catalyst and balance-of-plant innovations will deliver outsized returns if aligned to DOE-style cost milestones.

- Fleet operators and logistics firms: Undertake corridor-based deployments tied to hydrogen cost and refuelling density rather than national rollouts. Use PW Consulting’s pilot-evaluation toolkit to formalize go/no-go criteria for 2026 projects.

- Investors: Allocate funds across a spectrum of plays — catalyst/stack IP, hydrogen production and storage, and fleet conversion services — favoring assets with clear paths to non-dilutive revenue in 24–36 months.

- Policy-makers: Design time-limited incentives that bridge the gap between early adopter economics and scale-driven cost declines; targeted investment in hydrogen corridors is a leverage point for systems-level adoption.

Risks, uncertainties and monitoring triggers

- Raw material price shocks (including catalyst components) and missed cost-reduction targets can materially stretch return timelines.

- Delay or mismatch in hydrogen infrastructure deployment remains the primary adoption constraint for heavy-duty and long-haul use cases.

- Regulatory reversals or incentive tapering in key markets could produce lumpy demand and inventory overhangs; watch for shifts in fleet procurement policies and municipal procurement cycles.

- Consumer preference swings and dealer channel readiness — despite strong BEV growth in 2025 — mean commercial acceptance of FCEVs will be uneven without coordinated ecosystem action.

How executive teams should use the report in 2026 planning

- Run a one-day scenario workshop with PW Consulting’s templates to stress-test your 2026 product and investment plan against the three market scenarios provided.

- Adopt the report’s procurement playbook to renegotiate supplier terms with staged volume commitments tied to predefined technology and infrastructure milestones.

- Use the M&A diligence checklist to accelerate identificaton of high-value bolt-on targets that plug capability gaps (e.g., catalysts, balance-of-plant suppliers, hydrogen logistics providers).

- Integrate the pilot-evaluation toolkit into your CFO’s capital allocation gates so that fleet pilots convert to scale only when measured TCO and refuelling density criteria are met.

PW Consulting’s Electric Vehicles and Fuel Cell Vehicles Market report is intentionally crafted as a decision tool: it provides the modelling fidelity, commercial templates, and strategic frameworks executives need to move from hypothesis to funded programmes in 2026. This public summary highlights the strategic contours; for the full regional, application, and vehicle-type splits, granular financial models (USD Billion), and supplier-level forecasts that underpin these recommendations, please consult the complete report and datasets available through PW Consulting’s client portal.

For detailed analysis of this topic, please visit the official page:Electric Vehicles and Fuel Cell Vehicles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com