Deconstructing the Intrinsic and Projected WordPress Hosting Market Value Proposition Today

Other |

2026-06-20 07:16:08

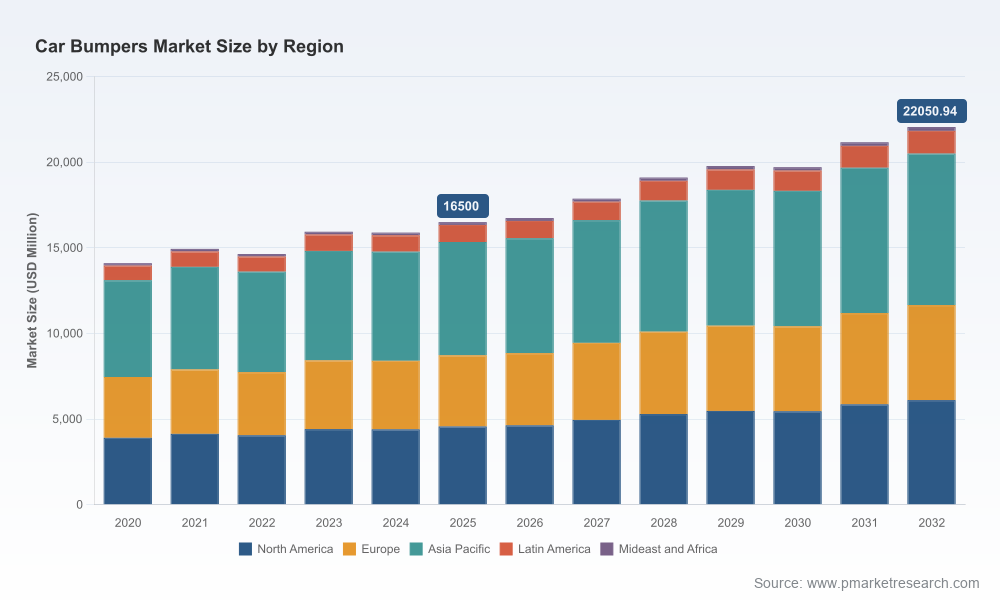

PW Consulting’s latest market intelligence on the global Car Bumpers market provides a targeted, decision-ready briefing for executives planning actions in 2026. Anchored on a 2025 base year and a 2026–2032 forecast horizon, our modeling shows the market expanding at a steady 4.2% compound annual growth rate (CAGR). The market recovered from a 2020 base and reached an estimated USD 16,500 Million in 2025; under our central scenario the industry is on a path toward roughly USD 22,050 Million by 2032. Market concentration has meaningful implications for competitive dynamics — the top three and top five firms account for a sizable portion of industry revenue, creating both entry barriers and consolidation opportunities for ambitious players.

Car Bumpers Market

Capital allocation: With predictable mid-single-digit growth and defined consolidation mechanics, manufacturers and suppliers must prioritize where to allocate scarce CAPEX—capacity expansions, refinery-to-resin partnerships, or recycling investments.

Car Bumpers Market

Product strategy: Lightweighting, integration of sensors and ADAS interfaces, and recycled-content mandates are not future abstractions; they are active cost and compliance levers that will influence engineering roadmaps and sourcing choices in 2026.

Car Bumpers Market

Commercial positioning: Aftermarket demand, warranty terms, and channel strategies will determine margin outcomes for OEM suppliers and independent aftermarket players. Firms that can translate sustainability credentials into supply certainty will command pricing power.

Regulatory acceleration toward circularity — Europe’s recent policy workstreams focused on automotive plastics and local landfill bans in select jurisdictions are tightening the operating environment. Expect regulators and major fleets to demand higher recycled-content thresholds and end-of-life collection programs in 2026.

Material economics and feedstock volatility — polypropylene remains the dominant material choice in bumpers due to its combination of light weight, impact resistance, and cost-effectiveness. Observed price behaviors in Northeast Asian markets underscore how packaging and automotive demand shifts, plus feedstock trends, rapidly influence input costs.

Aftermarket and specialty niches — heavy-duty steel and premium fabricated bumpers for trucks and SUVs continue to show resilience in the aftermarket and off-road segments, where product differentiation and brand reputation are stronger determinants of buyer choice than raw material cost.

Consolidation and scale — concentration ratios indicate that a relatively small set of players control a meaningful share of revenue. This produces incentives for mid-sized suppliers to seek alliances, carve out vertical niches, or pursue bolt-on acquisitions to secure distribution or engineering capabilities.

Buckstop Truckware — a U.S.-based specialist known for heavy-duty aftermarket steel bumpers and winch solutions. Their recent facility relocation completed in 2026 is positioned to increase operational throughput and shorten delivery cycles for North American truck and SUV platforms.

Expedition One — focused on precision-built off-road bumpers and overland accessories. Their engineering-first approach to fitment and finish keeps them closely aligned with enthusiast and aftermarket channels where premium margins persist.

Fab Fours — a U.S. manufacturer emphasizing premium steel truck and SUV bumpers and accessories. Fab Fours’ branding is strongly tied to domestic manufacturing and performance positioning in specialty segments.

Partify — a supplier of painted replacement body parts and CAPA/OEM-style bumpers, with service and warranty propositions designed to win fleet and collision-repair business. Their lifetime warranty offering is a competitive differentiator in cost-of-ownership conversations.

Recyclers and materials innovators — market activity includes industrial-scale recycling pilots converting damaged or end-of-life bumpers back into resin feedstock. These pilots, supported by some OEMs and polymer specialists, are emerging as strategic levers for sourcing security and compliance.

Facility investment and reshoring moves by select manufacturers point to a renewed emphasis on lead-time control and service levels in core markets.

Public-sector measures in Europe and local landfill bans in some North American regions are catalyzing investment in bumper collection and reprocessing programs — turning waste management into a competitive asset rather than an externality.

Material price trends in 2025 reinforced the sensitivity of bumper producers to feedstock dynamics; firms that locked in bilateral resin agreements or invested in recycling enjoyed cost resilience during price swings.

Proprietary demand model calibrated to 2020–2025 historicals and stress-tested across multiple macro scenarios for 2026–2032, enabling robust revenue and margin forecasting under alternative oil, policy, and vehicle production trajectories.

Supply-side heatmaps and supplier risk scores that identify single-source exposures, geographic bottlenecks, and logistics vulnerabilities down to tier-2 resin supply.

Regulatory & compliance matrix mapping policy levers to product design and manufacturing impact, with recommended compliance timelines and capex implications for each jurisdiction.

Cost model and scenario tools that isolate the effect of resin price, labor, transport, and recycled content premiums on finished goods margins — ready for CFO-level decision sessions.

Commercial playbooks for OEM suppliers and aftermarket players: go-to-market designs, warranty-architecture options, channel economics, and pricing templates keyed to use cases and customer segments.

M&A and partnership playbook outlining target archetypes, valuation heuristics, and integration priorities for buyers seeking bolt-on scale, technical capabilities, or recycled-resin capacity.

Operationally — secure dual-source access to polypropylene and establish contractual pathways to recycled resin. For manufacturers, mini-granulation or on-site reprocessing pilots reduce exposure to feedstock volatility and create a new margin lever.

Product and engineering — accelerate workstreams to make bumpers sensor-ready and compatible with ADAS components while maintaining crash-energy performance. Lightweighting should be balanced with repairability and recycled-content requirements.

Commercial — review warranty and returns policies to align with lifecycle requirements from fleets and insurers; consider value-added service packages (fitment, painting, lifetime support) as premium revenue streams.

M&A and partnerships — prioritize targets that fill capability gaps (recycling, painting & finishing, regional distribution) rather than only adding capacity. Strategic partnerships with polymer recyclers and resin suppliers can be less capital-intensive than greenfield capacity.

Regulatory engagement — formalize a policy-scan and lobbying cadence to both anticipate changes and help shape pragmatic recycled-content standards that permit scale without compromising safety or cost parity.

Sustainability as differentiation — transparency on recycled content, end-of-life programs, and supplier-chain traceability is becoming table stakes. Use recycled-content commitments to unlock preferential procurement from fleets and rental operators.

Week 1–4: Executive briefing and scenario alignment — share the central dashboard with C-suite and conduct a one-day scenario workshop to align on risk tolerance and priority opportunities.

Month 2: Rapid supplier and cost audit — deploy our supplier heatmap and cost model to identify top 3 supply risks and a quick-win resin sourcing re-negotiation target.

Month 3: Pilot and partner sprints — launch one recycled-content pilot or service-bundle pilot with a lead customer to test pricing, warranty terms, and logistics before a broader roll-out.

This release is designed as a strategic trailer: it surfaces the critical signals and recommended decision levers that will matter for 2026, while preserving the full suite of proprietary data, segment-level forecasts, and supplier-level analyses for the complete report. If you are positioning your company for profitable growth, resilient sourcing, and regulatory compliance in the mid-2020s, the in-depth models, playbooks, and risk matrices in PW Consulting’s Car Bumpers Market report are engineered to convert uncertainty into executable plans.

To access the complete dataset, scenario outputs, and actionable integration templates, visit our report page and request the full briefing. PW Consulting stands ready to support tailored workshops, valuation workstreams, and implementation sprints that translate the market outlook into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Car Bumpers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com