HFO-1234yf Market 2026 Strategic Preview — Actionable Intelligence for Executive Decision-Making

Executive summary

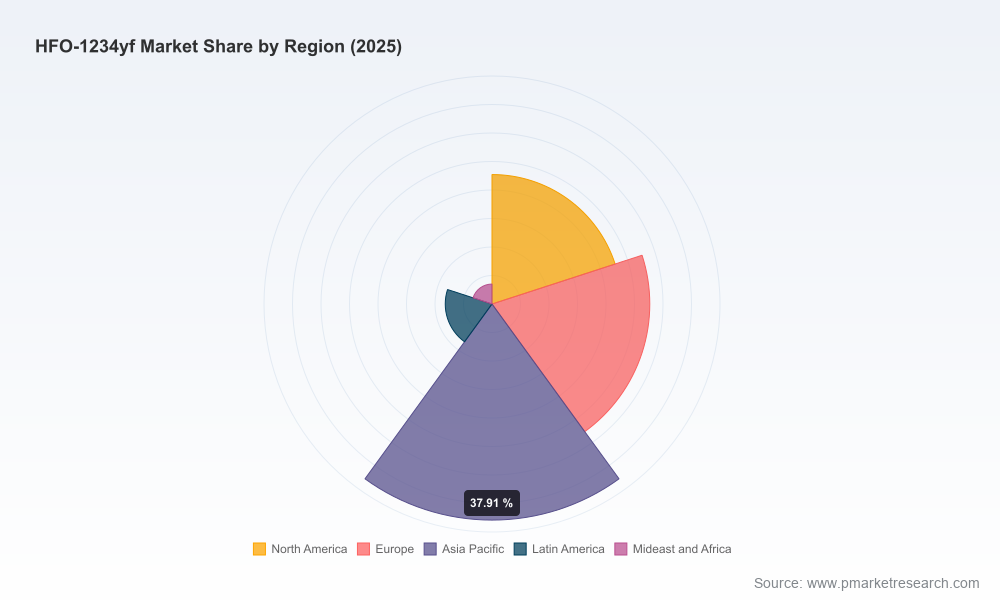

PW Consulting’s HFO-1234yf Market report (base year 2025; historical coverage 2020–2025; forecast 2026–2032) frames one of the chemicals sector’s fastest-growing segments. The market has expanded rapidly — rising from a modest base in 2020 to an estimated USD 2,000 Million in 2025 — and our forecast identifies a compound annual growth rate (CAGR) of 16.02% over the 2026–2032 period, reaching an anticipated market size in excess of USD 5.6 billion by 2032. For 2026 planning cycles, this profile creates a dual mandate: seize structurally attractive demand while hardening organizations against supply-side shocks and regulatory complexity.

HFO-1234yf Market

Why this matters in 2026

Three converging forces accelerate the strategic importance of HFO-1234yf for senior executives in chemicals, automotive OEMs, distributors and refrigerant service providers.

HFO-1234yf Market

- Regulatory ratification: The U.S. EPA’s April 2026 SNAP decision formalized HFO-1234yf as an acceptable substitute for ozone-depleting substances in motor vehicle air conditioning, with defined use conditions. This confirms regulatory runway for adoption and retrofit opportunities — but also raises compliance and documentation expectations for supply chains and OEMs.

- Price and feedstock volatility: Acid-grade fluorspar — a critical feedstock — has seen material price appreciation following supply restrictions in key Chinese mining regions. That dynamic, combined with a production base concentrated among a handful of global producers, drives outsized unit costs (market participants report HFO-1234yf trading at multiples of legacy refrigerants on a per-pound basis) and increases earnings volatility for exposed players.

- Concentrated supplier base: The market exhibits a high degree of concentration: the leading three suppliers account for a clear majority of global supply and the top five capture well north of 90% market share. This oligopolistic structure shapes commercial negotiating power, capacity expansion behavior and the pace of price normalization.

What the PW Consulting report delivers — pragmatic intelligence, not platitudes

Our deliverable is designed for boardrooms and deal teams that need to convert market insight into executable plans. The report combines empirical market sizing with playbooks and financial models built for real decisions:

HFO-1234yf Market

- Robust market-sizing and demand-driver analysis anchored to verified end‑use trends, with scenario projections to stress-test high- and low-adoption pathways across the 2026–2032 horizon.

- Supply-side mapping that goes beyond names — we stress-test global capacity, identify choke-points in feedstocks and logistics, and model the financial implications of tolling vs. greenfield options.

- Price and margin analytics with sensitivity sweeps for feedstock shocks, tariff regimes and inventory strategies — presented as operational levers for procurement and commercial teams.

- Regulatory tracker and compliance playbook documenting recent rulemaking (including SNAP and relevant retrofit guidance under U.S. statutes), anticipated rulings, and pragmatic compliance pathways that limit operational disruption.

- Competitive intelligence dossiers and supplier scorecards that synthesize capabilities, geographic posture, product breadth, and recent commercial moves into deal-ready recommendations.

- Action-oriented growth and defense strategies — from channel plays and retrofit-service rollouts to M&A screening, JV structures and contract templates tailored to the idiosyncrasies of refrigerant markets.

Competitive landscape — reading the strategic moves

The market is shaped by a small set of vertically integrated incumbent producers and an expanding cadre of regional manufacturers and distributors. Key strategic observations:

- Global brand leaders drive market norms. Established players with flagship product families (notably manufacturers marketing branded HFO-1234yf solutions for automotive air conditioning and stationary HVAC) set pricing benchmarks, influence OEM qualification processes and maintain preferred channel relationships with large automotive customers.

- Supply and pricing discipline matter. Recent commercial decisions by major suppliers — including mid‑2020s price adjustments to offset raw‑material and tariff pressures — illustrate how incumbents use pricing and capacity management to defend margins and slow commoditization.

- Distributors and service providers are strategic multipliers. Global gas distributors extend the reach of branded molecules into aftermarkets and retrofit services, often partnering with larger producers to secure allocations or acting as aggregation points for spot and contract volumes.

- Regional producers increase tactical complexity. Newer manufacturing centers and local champions are accelerating supply diversification. Their participation compresses lead times in certain corridors but also introduces variance in product qualification timelines and logistics risk.

Collectively, the marketplace dynamic is not a textbook commoditization: it’s an oligopolistic growth market where scale, contractual access to feedstock, and regulatory clearance create durable competitive advantage. For acquirers or partners, this means granular supplier diligence and scenario testing are table stakes.

Market dynamics that will shape 2026 boardroom choices

- Feedstock security will trump short-term price arbitrage. Firms that secure long-term fluorspar access, alternative feedstock routes or recycling/reclamation channels will gain asymmetric margin resilience.

- Regulatory clarity accelerates commercial pathways — and creates servicing opportunity. SNAP acceptance and retrofit permissions convert latent retrofit pools into addressable markets, but also create commercial frictions around documentation, equipment labeling and warranty exposure.

- Inventory and contract architecture become strategic weapons. Flexible contract designs (blended spot/contract structures, indexed pricing, capacity reservation clauses) will materially affect supply certainty and P&L volatility in 2026–2028.

- Premiumization and product differentiation will appear. Beyond pure HFO-1234yf supply, blended formulations and service bundles (warranty-backed retrofit kits, certified-charge programs) will be a growth vector for manufacturers and distributors seeking margin uplift.

2026 strategic playbook — recommended actions by stakeholder

- Producers: Fast-track brownfield expansions where permitting and logistics are tractable; secure feedstock via multi-year off-take or vertical integration; invest in blend capability and branded servicing to defend margin.

- Distributors and aftermarket players: Build certified service franchises for retrofit demand, establish allocation agreements with top-tier producers, and use premium service propositions (warranty, traceability) to capture higher-margin volumes.

- Automotive OEMs and fleet operators: Align procurement and warranty teams around supply qualification windows; secure long-term supply agreements tied to production schedules; evaluate in-house reclaim and on-site charging strategies.

- Private equity and corporate development teams: Target assets that add distribution breadth, localized production or reclamation capability; prioritize targets with off-take visibility and regulatory compliance infrastructure.

What we intentionally withhold in this preview

This briefing is a strategic overview intended to inform executive debate. To preserve the actionable advantage for subscribers and decision-makers, we have intentionally omitted the granular regional/application breakdowns, supplier-level volume schedules and detailed price-trajectory tables that appear in the full PW Consulting HFO-1234yf Market report. Those datasets — along with downloadable scenario models, supplier scorecards and contract annex templates — are provided to authorized report purchasers and are designed to be used directly in procurement negotiations and board-level decision packs.

How senior teams should use the full report in 2026 planning

Use the full PW Consulting report to accelerate three immediate deliverables for 2026 planning calendars:

- Inform capital allocation: run the integrated CapEx vs. tolling model in the report to determine the most defensible approach to capacity expansion under alternate feedstock-price scenarios.

- Structure commercial agreements: adapt our recommended contract clauses and pricing templates to protect margins while preserving flexibility under regulatory change.

- Prioritize M&A and partnerships: apply the supplier scorecards and diligence checklists to shortlist targets that will enhance access to allocation, diversify feedstock risk, or add aftermarket service capability.

Conclusion — a time to accelerate, but not to be reckless

HFO-1234yf presents a rare combination of strong secular demand and structural supplier power. The market’s trajectory — a multi-billion-dollar opportunity by the early 2030s with double-digit growth over the coming planning horizon — rewards decisive investment and disciplined contract design. However, margin outcomes will hinge on supply-chain strategy, regulatory readiness and the ability to translate product advantage into service-enabled pricing.

PW Consulting’s full HFO-1234yf Market report provides the empirical detail, operational playbooks and commercial models necessary to convert this industry momentum into durable competitive advantage. For teams preparing 2026 budgets and three‑year strategic roadmaps, the report is built to be immediately actionable.

For detailed analysis of this topic, please visit the official page:HFO-1234yf Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com