Sweet Protein Extracts Market Growing from USD 720M in 2025 to USD 1.8B by 2035; ADM Competes

Food |

2026-05-19 17:05:36

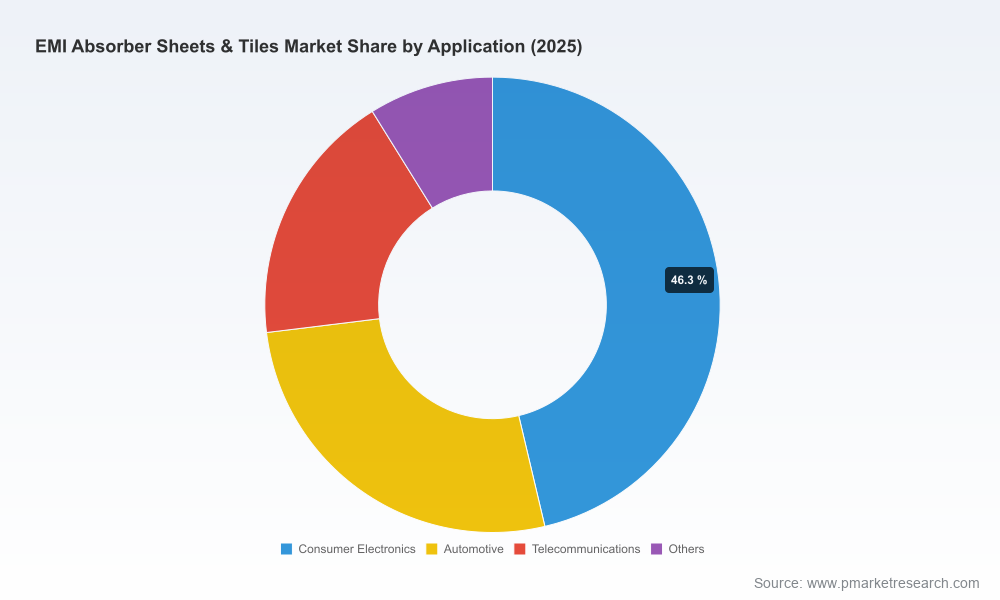

As the electronics, automotive and telecommunications industries accelerate toward higher frequencies, denser assemblies, and tighter regulatory oversight, EMI absorber sheets and tiles have moved from a niche mitigation product to a mandatory design element. PW Consulting’s latest market report (base year 2025, historical coverage 2020–2025, forecast period 2026–2032) distills the evolving competitive, regulatory, and supply-chain realities into decision-ready guidance for executives planning 2026 initiatives. At a macro level, the global market is projected to grow at a compound annual growth rate (CAGR) of 5.1% through 2032, expanding from a 2025 aggregate of USD 778.0 Million to an estimated USD 1,102.04 Million by 2032. This briefing highlights the strategic value of the full report and how senior leaders should use it to prioritize investments, partnerships, and operational changes in 2026.

EMI Absorber Sheets & Tiles Market

Risk-aware investment: With disciplined growth but notable technology and regulatory drivers, the sector favors targeted, risk-managed capital allocation. Our analysis quantifies near-term demand trajectories and maps them to leverageable capabilities (materials, converting, testing), enabling CFOs and corporate strategy teams to size investments with confidence.

EMI Absorber Sheets & Tiles Market

Time-bound product roadmaps: OEMs must balance broadband vs. narrowband approaches, thermal integration, and form-factor constraints. The report translates frequency-, form-, and thermal-driven performance needs into suggested product roadmaps and R&D milestones aligned to a 2026 development calendar.

EMI Absorber Sheets & Tiles Market

Supply chain rebalancing: Raw material concentration (ferrites and conductive polymers) and labor-sensitive converting processes drive differentiated cost exposure. The report provides a pragmatic supplier-risk matrix and contingency playbooks for procurement and operations teams.

Regulatory compliance planning: EMC standards now mandate absorption performance across wide frequency ranges and end-use certifications like RoHS and flame-retardancy (e.g., UL94V-0) are table stakes. Our compliance checklist converts regulatory language into testable, sourcing, and labeling actions for 2026 product launches.

Stable, mid-single-digit growth: The market’s CAGR of 5.1% through 2032 reflects steady demand improvement driven by higher-frequency electronics, automotive electrification, and 5G/edge infrastructure rollouts. Growth is consistent but not hyper-exponential—favoring disciplined strategic moves over speculative bets.

Consolidation and concentration: Market concentration is meaningful—our CR3 and CR5 metrics (65% and 75% respectively) show a compact competitive set with several large, capability-rich suppliers dominating core technologies. This dynamic favors buyers that can secure strategic supply agreements and partners that pursue adjacent feature differentiation.

Material and process as differentiators: Ferrites and conductive polymers constitute the primary raw material footprint, while adhesive converting and die-cutting remain cost and quality inflection points. Companies that optimize material mixes and converting efficiency will unlock margin and performance advantages.

Regulatory and testing overheads: EMC compliance up to 10GHz and flame-retardant certifications are elevating test-lab investment and supplier qualification requirements. Organizations that front-load compliance planning reduce time-to-market friction for 2026 product cycles.

The report is designed for executives, product leaders, procurement heads, and corporate development teams who require executable guidance rather than descriptive market anecdotes. Highlights of the contained deliverables:

Executive dashboard with scenario modeling: Sensitivity analyses by demand shock, raw material price stress, and regulatory tightening to quantify P&L and working-capital impacts on a 6–24 month horizon.

Detailed go-to-market playbooks: Channel mixes, sample pricing frameworks, recommended distributor partnerships, and OEM engagement sequencing tailored for consumer electronics, automotive, and telecom customers.

Supply-chain risk maps and supplier scorecards: Assessment of raw-material sourcing, converting capability, lead-time sensitivity, and near-shore/on-shore opportunity matrices for reducing single-source exposure.

Product engineering guidance: Technical trade-offs between broadband and narrowband absorbers, thermal pad integration strategies, die-cut tolerances, and adhesive selection criteria linked to manufacturability and certification outcomes.

Regulatory and test-plan templates: Stepwise certification roadmaps aligned with EMC requirements up to 10GHz and flame-retardancy standards that buyers and manufacturers can operationalize.

Opportunity heatmap and investment prioritization: Market segments and use cases ranked by near-term revenue potential, margin attractiveness, and strategic fit—presented as prioritization guidance rather than raw segment figures (those granular numbers are reserved for the full report).

Competitive benchmarking: Capability matrices across materials, converting, distribution, and technical support—structured to support supplier selection, JV screening, and M&A diligence.

The sector’s leading vendors bring distinct capabilities. Our full competitive analysis synthesizes public disclosures, product catalogs, and PW Consulting’s primary interviews to map strengths, strategic intent, and vulnerabilities for 2026 engagement. Representative profiles include:

3M Company (St. Paul, MN): A broad product arsenal that spans absorber sheets across wide frequency bands. 3M’s strengths are brand, application engineering, and integrated adhesive solutions—advantages in high-volume consumer and industrial OEM channels. Expect continued emphasis on broad-spectrum, validated materials and system-level testing support.

Laird Performance Materials (United States): Known for thin elastomer absorbers, ferrite sheet integration, and dispensable formats for complex assemblies. Laird’s proficiency in near-field and cavity-resonance mitigation makes it a preferred partner where mechanical constraints and weight are critical.

Fair-Rite Products Corp. (Wallkill, NY): A core ferrite-component specialist that feeds absorber-sheet makers and OEMs directly. Their updates targeting smart-home, automotive, and medical end-uses indicate a focus on application-specific ferrite formulations and catalog refresh cadence.

KITAGAWA INDUSTRIES (Japan): Supplier of series-based absorber sheets and ferrite absorbers for EMC applications, with a product lineup regularly refreshed to address broadband and narrowband needs—particularly in markets with stringent EMC protocols.

Henkel AG & Co. KGaA (Düsseldorf): Active in shielding films and adhesive systems with a recent focus on cost-effective automotive electronics solutions. Henkel’s Productronica 2025 launch signaled an intent to capture assembly-integrated applications through film-adhesive-system bundles.

Recent documented developments in 2025 and 2026 confirm the trend toward product catalog modernization, targeted launches for automotive electronics, and ferrite component updates—signals of vendors aligning portfolios with higher-frequency, automotive and smart-home demand.

Based on scenario analyses and supplier assessments, PW Consulting recommends the following prioritized actions for organizations active in or adjacent to the EMI absorber market in 2026:

Secure multi-year supply agreements for critical raw materials (ferrites, conductive polymers) with defined quality and lead-time SLAs. Include price-hedging triggers for raw-material spikes.

Invest in in-house or partnered testing capabilities for EMC up to 10GHz and flame-retardancy; early compliance reduces integration cycles and warranty risk.

Optimize converting and die-cutting either through CAPEX investments or by consolidating to qualified contract manufacturers that meet tight tolerance and throughput requirements.

Prioritize modular absorber design (plug-and-play tiles, customizable sheets) for OEM customers to accelerate qualification and increase per-customer share of wallet.

Use CR3/CR5 concentration metrics to structure competitive bidding: diversify among top-tier suppliers while securing co-development relationships with one strategic partner for innovation acceleration.

Pursue bolt-on M&A selectively to fill capability gaps—target firms with unique ferrite formulations, low-cost converting footprint, or proprietary adhesive chemistries.

In keeping with the “trailer” principle of this release, we have provided high-confidence macro market sizing (2025 base of USD 778.0 Million; forecast to USD 1,102.04 Million by 2032 at a 5.1% CAGR), concentration metrics (CR3 = 65%, CR5 = 75%), and qualitative competitive and regulatory insight. However, we are intentionally not publishing the granular per-region, per-type, and per-application split numbers in this briefing. Those detailed segment-level figures and proprietary unit-cost models are included exclusively in the full PW Consulting EMI Absorber Sheets & Tiles report and are essential for precise supplier selection, pricing strategies, and go-to-market modeling.

Board-level strategy: Use the scenario dashboards to stress-test capital allocation and acquisition strategies under alternative demand and material-cost scenarios.

Product development: Align R&D roadmaps to the broadband/narrowband and thermal integration guidance to prioritize feature sets most likely to capture incremental margin.

Procurement and operations: Implement the supplier scorecards and contingency blueprints during Q1–Q2 2026 sourcing cycles to mitigate lead-time exposure and ensure certification compliance.

Corporate development: Apply the M&A filter and valuation overlays to screen targets that provide immediate capability uplift or route-to-market acceleration.

For executives and teams preparing 2026 budgets, contracts, and product timelines, PW Consulting’s full report delivers the quantitative granularity and implementation templates needed to convert market trends into measurable outcomes. Access to the complete dataset, supplier-level benchmarking, and downloadable modeling tools is available on our report page. Contact PW Consulting to request a briefing tailored to your organization’s role in the ecosystem—whether you are an OEM seeking design-in, a materials supplier optimizing production, or a strategic buyer hedging supplier risk.

For detailed analysis of this topic, please visit the official page:EMI Absorber Sheets & Tiles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com