Latin America Radiology Services Market

Other |

2026-05-28 11:25:11

PW Consulting today publishes an in-depth market study on the global cephalosporin sector designed to support executive decision-making in 2026. The study synthesizes five years of historic market behavior (2020–2025) with scenario-based forecasts covering 2026–2032. Our base-year calibration for commercial planning is 2025. At the macro level, the market is expanding steadily, with a 3.0% compound annual growth rate (CAGR) embedded in our central case and a projected market value of approximately USD 21,829 Million by 2032. This release explains why those headline metrics matter for commercial, manufacturing and M&A plays in 2026 — and why granular segment-level intelligence in the full report is essential for execution.

Cephalosporin Market

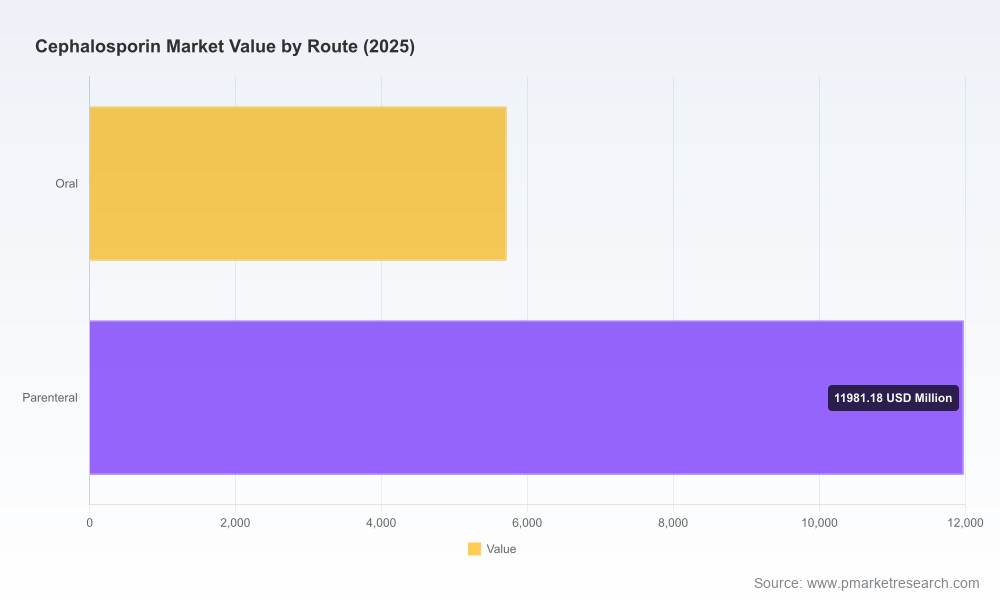

Measured, investment-grade growth: A low-mid single-digit CAGR (3.0%) across the forecast window reflects steady demand for both oral and parenteral cephalosporins, tempered by generic competition and procurement-driven pricing pressure. For most industry players, 2026 will be a year of operational optimisation rather than aggressive market expansion.

Cephalosporin Market

Transitional product mix: While older-generation cephalosporins will continue to form the backbone of many hospital formularies, demand pockets are emerging around higher-value injectable and combination therapies that address resistant Gram-negative pathogens. Portfolio prioritisation will therefore be a primary lever for margin recovery.

Cephalosporin Market

Timing for capital deployment: Given the projected market plateauing and measured growth, near-term capex should be targeted and modular — focused on sterile injectable capacity, quality upgrades (GMP compliance) and regional fill/finish capabilities that shorten lead times and reduce landed cost exposure.

Supply-chain concentration and input risk: Our sector analysis reconfirms that a small number of production clusters in China account for the majority of key cephalosporin intermediates (notably 7‑ACA and 6‑APA derivatives). This concentration creates significant pricing and availability leverage for those suppliers and exposes downstream manufacturers and procurers to geopolitical and tariff shocks.

Tariff and landed-cost volatility: Since early 2025 expanded trade measures have materially increased duties on certain Chinese API imports. Buyers that fail to model tariff scenarios and landed-cost sensitivities risk margin erosion or supply interruptions; conversely, proactive hedging and supplier diversification yield outsized resilience.

Regulatory and reimbursement context: Generics continue to dominate the market structure, driven by patent expirations and hospital procurement contracts. Regulatory pathways in major markets (US FDA, NMPA, EMA) are simultaneously accelerating review for products that address antimicrobial resistance, but they also require demonstrable GMP-compliant manufacturing. These dynamics create a bifurcated opportunity set: low-cost generics at scale versus premium, higher-margin advanced-generation or combination therapies.

Commercial procurement pressures: Hospital tendering and group purchasing organisations remain the primary demand levers, reinforcing price sensitivity for commodity cephalosporins while opening negotiation windows for differentiated sterile injectables and novel combinations.

The cephalosporin market sits in a mid-fragmented structure: the three largest global players account for a meaningful share but not dominance, and the top five collectively still leave substantial volume to regional and specialist suppliers. PW Consulting’s concentration metrics show a market where scale matters, but agility and manufacturing quality deliver strategic advantage.

Indian specialists and scale players: Aurobindo, Lupin, Cipla, Sun Pharma, Orchid and Wockhardt are prominent producers with integrated API and formulation capabilities. Their strengths are cost-competitive supply chains, manufacturing scale and established relationships with institutional buyers. Strategic questions for these players in 2026 will revolve around upgrading sterile injectable capacity, mitigating API tariff impact, and commercialising advanced combinations.

Western and global generics leaders: Teva, Pfizer, GSK, Novartis and Merck remain influential for regulated markets and branded generics. Their advantages are regulatory experience, global distribution, and portfolio breadth. These firms will focus on defending premium tender lines, selective innovation, and vertical integration where it reduces risk.

Regional manufacturing specialists: Major Chinese API producers and European high‑purity API suppliers play complementary roles. China-based manufacturers supply large volumes of intermediates, while select European and Japanese firms focus on higher‑value intermediates and tailor-made batches for regulated markets.

Notable recent developments: In 2026 Wockhardt secured U.S. regulatory approval for a cefepime–zidebactam combination for complicated urinary tract infections — a clear example of premiumised product strategy leveraging antimicrobial resistance priority pathways. Earlier moves such as new injectable plants and approvals in regional markets illustrate ongoing capacity rebalancing across the ecosystem.

This is not a descriptive survey; the study is constructed as an operational toolkit for 2026 execution. Key deliverables include:

Proprietary market model (historic 2020–2025; forecast 2026–2032) with scenario toggles for price erosion, tariff shocks and accelerated adoption of advanced therapies.

Supplier & API dependency heatmaps highlighting single‑source exposures and concentration clusters, enabling procurement teams to quantify re‑sourcing cost versus business‑continuity risk.

Regulatory tracker across major jurisdictions with timelines, approval success indicators and an AMR-priority pathway dashboard for combination products.

Commercial playbooks for unit managers and tender teams: pricing architecture, hospital segmentation, and negotiation tactics tailored to oral vs injectable formats.

Manufacturing and capex decision matrix that maps ROI against regulatory readiness, SKU rationalisation and local content constraints.

M&A and partnership screening: a ranked universe of mid‑market API and formulation targets, with strategic fit scores and integration risk profiles.

Quarterly watchlist of industry events and supplier signals (plant start‑ups, regulatory approvals, tariff changes) crucial to rolling forecasts in 2026.

Procurement: Implement a two‑track purchasing strategy that secures immediate volume through existing low‑cost suppliers while establishing validated secondary sources to mitigate tariff and geopolitical risk.

Manufacturing & Operations: Prioritise GMP upgrades for injectable lines, and adopt modular investment to scale sterile capacity. Consider toll‑manufacturing partnerships to accelerate time‑to‑market without heavy upfront capex.

Commercial & Marketing: Recalibrate portfolio focus toward premium sterile injectables and novel combinations that benefit from regulatory priority reviews; rework tender playbooks to capture value beyond headline price (e.g., supply reliability, delivery lead time, patient outcome data).

M&A & Corporate Development: Identify API and small‑scale injectable plants that provide rapid capacity expansion or de‑risked access to intermediates. Valuation discipline is critical in a market where consolidation yields but elevated capex requirements temper returns.

R&D & Regulatory Affairs: Align pipeline investments to AMR priority areas where regulatory agencies provide accelerated pathways, but ensure trial designs and CMC packages meet GMP expectations for seamless approvals.

Managers and investors face a market that is steady but structurally challenged by supply concentration, tariffs and generics pricing pressure. The PW Consulting Cephalosporin Market report turns those challenges into actionable choices: quantify supply‑chain exposure, prioritise small‑ticket capex that materially improves margin, exploit differentiated regulatory pathways for novel combinations, and pursue targeted M&A to close strategic gaps. The report’s combination of scenario modeling, supplier scoring and regulatory intelligence is designed to shorten decision cycles and reduce execution risk during 2026.

Our competitive profiles draw on primary and secondary research across leading manufacturers — from integrated API-to-dose players in India and China to global generics leaders and specialised European suppliers. Market concentration metrics and company capability assessments are included in the full report; while this release outlines directional strengths and risks, core segment-level tables and proprietary forecasts are intentionally withheld here to preserve the actionable value of the paid research.

Executives and investors seeking the complete dataset, segment-level forecasts, supplier heatmaps and bespoke advisory support for 2026 planning can request the full report and model via the PW Consulting website. Our analysts are available for confidential briefings and custom scenario builds to align the research directly with corporate planning cycles.

PW Consulting — deep sector expertise, actionable intelligence, and pragmatic recommendations to convert cephalosporin market complexity into strategic advantage in 2026.

For detailed analysis of this topic, please visit the official page:Cephalosporin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com