Tattoo Removal in Dubai: Get Rid of Unwanted Ink

Health |

2026-04-07 11:26:02

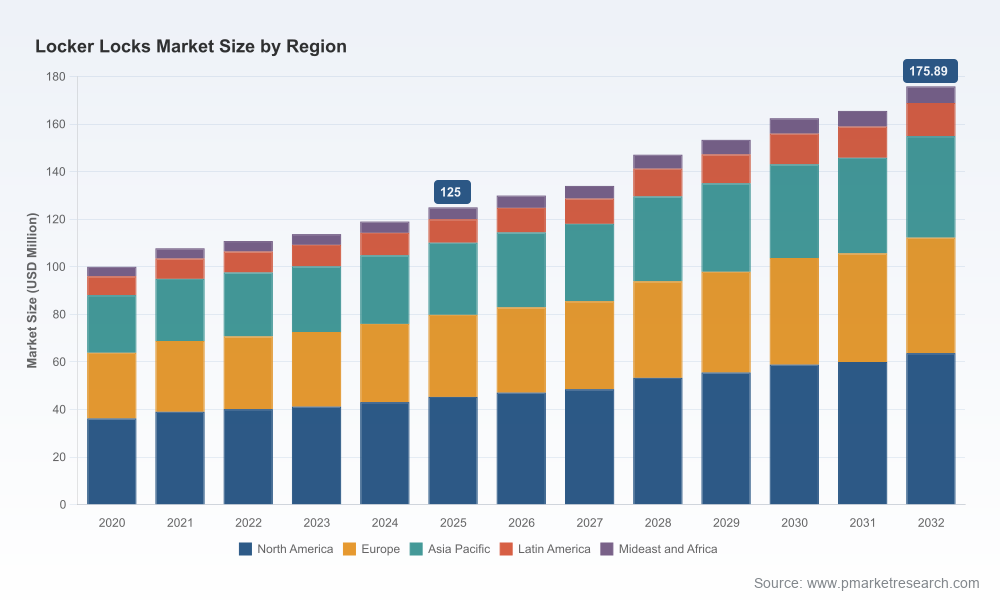

As organizations renew capital plans for 2026, locker security has moved from a procurement line-item to a strategic asset. PW Consulting’s latest Locker Locks Market study (base year: 2025) synthesizes seven years of observed behavior and a seven-year forecast (2026–2032) to equip C-suite and procurement leaders with the evidence they need to take decisive action. The market demonstrates steady, predictable expansion at a compound annual growth rate (CAGR) of 5.0%. After methodological normalization for pandemic and supply-chain anomalies across 2020–2025, the market reached a clear baseline in 2025 and is forecast to continue its disciplined growth through 2032.

Locker Locks Market

Budget timing: With capital and operational budgets being finalized in Q1–Q2 of 2026, organizations that understand multi-year TCO and compliance exposure can achieve both cost savings and risk reduction.

Locker Locks Market

Technology transition: The market’s steady CAGR masks uneven disruption beneath the surface — electronic and smart solutions are advancing rapidly even as mechanical offerings retain relevance in low-cost, high-turnover use cases.

Locker Locks Market

M&A and partnership signals: Market concentration metrics show that incumbent leaders maintain strong market share, creating buy/partner opportunities for mid-market vendors and systems integrators aiming to scale quickly.

Using a consistent revenue unit (USD, Million) and a base-year normalization approach, PW Consulting calibrated historical performance (2020–2025) against macroeconomic factors and channel disruptions to arrive at the 2026–2032 forecast. The result is a robust projection that reflects steady demand growth driven by institutional refits, workplace reconfigurations, and an incremental replacement cycle for legacy hardware.

For strategic planners, the headline is simple: the total market is growing predictably and offers a stable environment for staged investment. That predictability enables scenario-based capital allocation — for example, pilots of connected locker systems in 2026 followed by scaled rollouts in 2027–2028 — without exposing organizations to outsized market timing risk.

Digitalization and data: Electronic and smart locker solutions increasingly emphasize encrypted audit trails, role-based access, and integration with building management and HR systems. Data privacy regimes, notably GDPR-style requirements, are forcing vendors and buyers to bake secure logging and encryption into procurement specifications.

Compliance layering: Safety and occupational standards (for example, standards that govern lockout/tagout and access control for hazardous areas) are constraining product design and procurement checklists. Buyers must reconcile safety regulations with digital feature sets when drafting RFPs.

Deployment trade-offs: Our analysis highlights an important architectural choice that recurs in buyer interviews — whether to deploy PoE (Power over Ethernet) networked systems, which require cabling and enable centralized management, or battery-powered wireless modules, which lower upfront infrastructure cost but increase lifecycle maintenance activity. This trade-off materially affects installation CAPEX, annual OPEX, and refresh cycles.

Supply-chain and materials pressure: Variability in raw material prices and labor costs for specialized assemblies drives SKU-level margin differences. Buyers and private-equity sponsors should model supplier cost pass-through scenarios into multi‑year price indexes.

The Locker Locks market displays moderate-to-high concentration: the top three global vendors control a substantial share of the market, and the top five capture an even larger slice. This structure creates a dual-track competitive dynamic: established firms focus on bundled solutions and channel depth, while agile mid‑market players compete on feature differentiation and vertical specialization.

Master Lock Company (United States) — leveraging brand recognition and wide channel reach to expand smart and commercial offerings for gyms, schools, and facilities. Recent product introductions underscore a push into integrated commercial smart locks.

Abloy Oy (Finland) — positioning on high-security, engineered mechanical and electromechanical systems, serving segments where durability and tamper-resistance are critical.

Codelocks (United Kingdom) — accelerating its digital portfolio with compact, robust electronic locks and perimeter access components; recent launches highlight a product-led approach to incremental innovation.

Lowe & Fletcher Ltd. (United Kingdom) and EMKA Group (Germany) — both pursue industrial and institutional hardware channels, optimizing for retrofit and customization demand.

Digilock (United States), Allegion (United States), Hafele (Germany), and Hettich Group (Germany) — these incumbents combine legacy distribution with systematic upgrades into intelligent solutions, often through strategic OEM relationships.

Fast-followers from China and Spain — including Be‑Tech, MAKE Security Technology, Ningbo Wangtong, and Ojmar — increasingly compete on price/performance in certain global channels, often partnering with regional integrators to bridge compliance gaps.

Late 2025 — Codelocks launched a more compact digital lock variant and introduced an adjustable latch for perimeter gating, signaling investment in both miniaturization and access-layer expansion.

2025–2026 — Major brand collaborations expanded smart lock product lines tailored to multi-family and commercial portfolios, underscoring that property managers remain a meaningful demand pool.

Early 2026 — Incumbent vendors continued to introduce commercial-grade smart locks aimed at SMB and enterprise customers, reflecting a move to translate brand trust into recurring service and retrofit revenue.

Procurement: Add compliance and data-security sweeps to the procurement process. RFPs should require encrypted audit trails, explicit data-retention policies, and supply-chain traceability as pass/fail criteria rather than optional features.

Architecture: Treat the PoE vs. battery decision as a portfolio exercise. Pilot networked systems in high-value, centrally managed sites while deploying wireless battery systems where fast installs and low disruption are the priority.

Vendor selection: Factor lifecycle service economics into vendor scoring. A lower upfront price can be eclipsed by higher annual maintenance and replacement costs — model TCO across a seven-year horizon to align procurement with finance KPIs.

M&A and partnerships: Strategic buyers should look for mid-market vendors with defensible IP in encryption or integration modules, or systems integrators with deep vertical channel relationships. The market’s concentration dynamics create arbitrage opportunities for bolt-on acquisitions that add access to recurring installation and service revenue.

Operational readiness: Facilities teams must plan asset tagging and data integration as part of scheduled refurbishments. Early coordination with IT and compliance reduces costly rework and accelerates ROI.

This preview intentionally showcases strategic takeaways while omitting granular split data to preserve the value of the full study. The complete report provides practical, operational tools and decision support assets designed for immediate use by procurement, facilities, and corporate strategy teams, including:

Validated market-sizing and scenario models — downloadable spreadsheets that allow scenario toggles for adoption rates, technology mix, and regional rollout phasing.

Vendor scorecards and supplier negotiation playbooks — standardized templates that translate technical requirements into contractual clauses and SLAs.

Deployment cost calculators — side-by-side cost comparisons for PoE vs. battery systems, including cabling, commissioning, and ongoing maintenance assumptions.

Compliance and cybersecurity checklist — an executable list mapping regulatory obligations (data privacy, CE marking, lockout/tagout) to product specifications and vendor attestations.

Integration and systems architecture guidance — recommended integration patterns for enterprise identity providers, BMS, and property-management platforms.

Case studies and buyer personas — real-world implementation examples across corporate, residential, and institutional buyers, with quantified lessons on payback intervals and user-experience trade-offs.

CFOs and corporate finance: Use the report’s TCO models to stress-test capital requests and to build service-contract commitments into five-year forecasts.

Procurement leaders: Implement the procurement playbook and vendor scorecards in Q1 sourcing cycles to shave vendor selection time and reduce legal negotiation friction.

CEOs and strategy teams: Evaluate acquisition targets using the concentration and growth context. Identify tuck-in candidates that can expand recurring-service footprints or add complementary access-control modules.

Facilities and IT: Adopt the deployment calculators and integration blueprints before pilot rollouts to avoid common retrofit pitfalls and to align on support models with vendors.

This preview presents the strategic frame and operational implications derived from PW Consulting’s in-depth study. The Locker Locks market is not a commodity category; it sits at the intersection of physical security, IT systems, and regulatory compliance. With a steady market growth profile and a concentrated competitive structure, the category rewards disciplined, data-driven decision-making. For procurement teams aiming to convert 2026 budgets into durable competitive advantage, the full report provides the missing rigor: executable models, vendor playbooks, and compliance-first procurement instruments.

To access the complete dataset, proprietary segmentation, and the full suite of decision-support templates referenced above, please visit our report landing page. The full report includes the detailed splits, downloadable tools, and the exhaustive vendor benchmarking that we intentionally withhold from this preview to preserve its commercial value.

For detailed analysis of this topic, please visit the official page:Locker Locks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com