Subtle Enhancements: The Rise of the "Baby Filler" Trend

Health |

2026-05-15 15:32:17

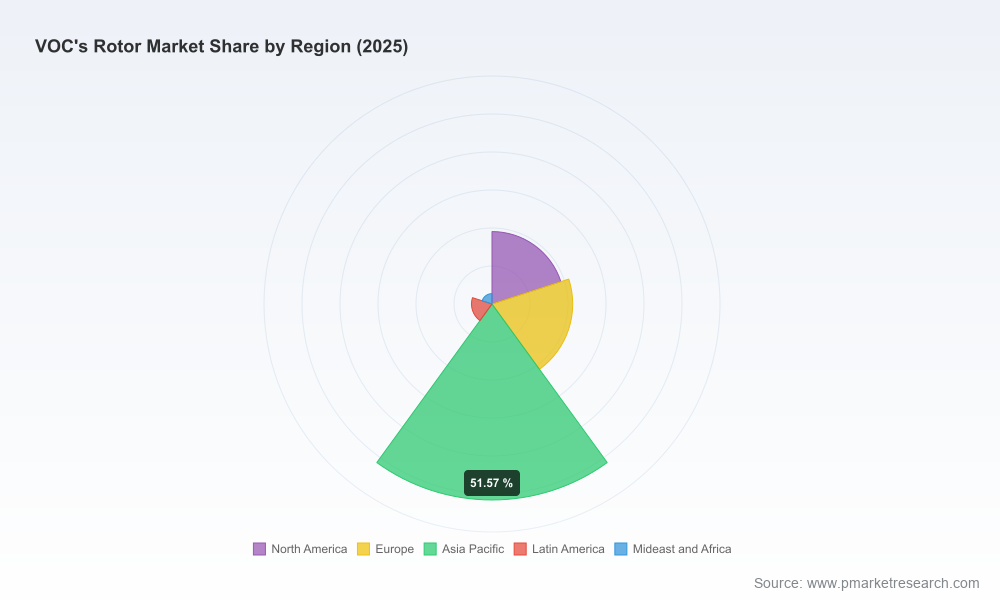

PW Consulting’s latest VOC’s Rotor Market study (base year 2025) provides a focused, actionable intelligence package designed to inform executive decisions throughout 2026. The market for VOC concentrator rotors has expanded materially since 2020, with overall industry revenue rising from USD 135 Million in 2020 to USD 183 Million in 2025 (base year). Our historical analysis shows a compound annual growth rate in the mid-single digits for 2020–2025; the market is then forecast to continue expanding through 2032 at a 4.85% CAGR, reaching an aggregate market size in the high USD hundreds of millions by 2032. This briefing highlights the strategic implications of those trends without disclosing the full segmentation tables — the complete dataset, regional and application-level splits, and vendor scorecards are available in the full report.

VOC's Rotor Market

Regulatory acceleration: Energy-efficiency mandates and tightening emissions rules in semiconductor fabs and heavy manufacturing are driving faster adoption of selective adsorption technologies and higher-performing rotor solutions.

VOC's Rotor Market

Technology differentiation: Innovations in zeolite formulations and honeycomb substrates materially affect lifecycle operating cost and energy consumption — choices that directly influence capex ROI and TCO models.

VOC's Rotor Market

Concentration and consolidation dynamics: Market concentration is meaningful — the top three and top five suppliers collectively command a substantial share of installed capacity — creating both supply-side risks and M&A opportunities.

Operational drivers: Labor automation pressures and the need to secure reliable abatement in high-value production (semiconductor, automotive, chemical) force earlier deployment cycles for high-efficiency rotor systems.

Validated market-size trajectory (2020–2032) with scenario modeling calibrated to energy policy and capex cycles.

Decision frameworks — procurement scorecards and capex sizing templates that convert rotor performance metrics into expected operating-cost delta and payback timelines.

Vendor benchmarking — qualitative and quantitative profiles of leading OEMs, technology integrators and material suppliers, including technology differentiation, service footprint, and partner ecosystems.

Supply-chain heat maps and risk matrices — raw-material exposure assessment (substrate and adsorbent), single-source risks, and mitigation levers.

Regulatory-impact playbooks and compliance checklists aligned to industry standards and ISO requirements for solvent cleaning and VOC concentration devices.

M&A and partnership screening tools — target filters, valuation sensitivity analyses, and integration checklists for bolt-on acquisitions and strategic alliances.

Two sets of forces are shaping vendor and buyer behavior heading into 2026. First, regulatory and standards pressure — from energy-efficiency mandates in semiconductor and industrial manufacturing to ISO-level expectations for rotor performance and maintenance — is pushing buyers toward validated, higher-efficiency rotor assemblies and proven maintenance regimes. Second, supply-side technical choices matter: honeycomb inorganic-paper substrates, high-silica zeolites and activated carbon (molecular sieve variants) remain core inputs. Variations in substrate manufacturing quality or adsorbent formulation yield meaningful differences in cycle life, regeneration energy, and contaminant selectivity. Our field interviews and primary-sourced data show manufacturers are increasingly judged on total lifecycle cost and integration compatibility with regenerative thermal oxidizers (RTOs) and rotary heat-recovery systems.

Operationally, automation-driven labor constraints are creating willingness among OEMs and end-users to adopt solutions that reduce manual maintenance and simplify rotor exchange processes. In short: buyers in 2026 will pay a premium for rotors that demonstrably lower energy use, maintenance hours and risk of unplanned downtime in high-value production environments.

The market exhibits a moderate degree of concentration: the top three players control a significant portion of capacity, with the top five expanding that share further. This configuration produces clear implications for market entrants, suppliers and buyers — incumbent suppliers can influence standards and supply availability, while buyers must weigh strategic dependence versus supplier switching costs.

Key players covered in the report and their strategic positioning:

Seibu Giken Corporation (Japan) — A leader in honeycomb rotor concentrator systems, Seibu Giken’s strength is integration capability for semiconductor and industrial manufacturing environments. Their technology emphasizes energy efficiency and compatibility with concentrator/RTO assemblies.

Huashijie Environment Technology (HSJ) (China) — Focused on molecular sieve adsorption rotors paired with RTOs for industrial fixed-source treatment, HSJ is notable for cost-competitive offerings and a growing footprint in industrial clusters.

Nichias Corporation (Japan) — Nichias pushes performance through proprietary honeycomb and zeolite mixes (HONEYCLE HZ series). Their positioning is high-reliability, low-concentration VOC abatement for solvent-cleaning and precision manufacturing.

Munters (Sweden) — Known for zeolite rotor concentrators engineered for high-volume, low-concentration emissions. Munters competes on material science and global aftermarket service capabilities.

Taikisha Ltd. (Japan) — Brings systems-level expertise, combining rotary RTOs, heat storage and rotor components into turnkey exhaust treatment solutions for large industrial and OEM customers.

ProFlute AB (Sweden) — Specialist in molecular sieve and desiccant rotors; their products support VOC removal in niche dehumidification and abatement contexts, often integrated by systems houses.

Our vendor analysis evaluates each firm on technology defensibility, manufacturing scale, aftermarket service, and channel access. The emergent picture: companies that tightly control adsorbent formulation and substrate quality while offering robust service networks often secure preferred vendor status for capital projects in semiconductor and automotive facilities.

Prioritize total-cost-of-ownership metrics over initial purchase price. Model energy consumption and maintenance cycles across a 5–10 year horizon for rotor replacements.

Lock in strategic raw-material arrangements for key substrates and high-silica zeolite blends to mitigate spot-market volatility.

Deploy pilot installations that measure real-world energy and downtime impacts; require vendors to support measurable KPIs as contract conditions.

In procurement, favor suppliers with strong integration experience with RTO systems and documented ISO-compliant maintenance regimes.

For investors and corporate M&A teams: screen targets for proprietary adsorbent IP, reliable manufacturing processes for honeycomb substrates, and installed-base service contracts that provide recurring revenue.

Build regulatory scenario stress-tests into capital planning to account for accelerated emissions standards or energy-price shocks.

Given the market’s concentration profile and the technology-driven differentiation among suppliers, we anticipate three primary investment themes for 2026:

Bolt-on acquisitions that expand adsorbent formulation capability or substrate manufacturing are attractive to OEMs seeking vertical control and margin improvement.

Service-driven roll-ups that aggregate maintenance networks and spare-parts capabilities can accelerate aftermarket revenue and reduce churn among large industrial customers.

Partnerships between rotor manufacturers and RTO/system integrators that bundle performance guarantees create higher barriers to entry and de-risk adoption for large buyers.

Strategic and commercial teams should treat the report as a playbook: (1) use the scenario models to size near-term investment and procurement budgets; (2) apply the vendor scorecards to shorten supplier selection cycles; (3) deploy the regulatory playbooks to ensure compliance-readiness prior to capital commissioning; and (4) use the M&A filters and valuation templates to accelerate diligence on acquisition targets.

This briefing highlights the report’s strategic value while deliberately omitting our full segmentation and vendor scorecard tables to encourage detailed review of the primary datasets, Excel models and company profiles hosted with the full publication. The full report contains the complete regional, type and application splits, transaction-ready financial models, and an expanded set of vendor profiles and interview transcripts. For procurement teams, investors, and R&D leaders preparing budgets and roadmaps in 2026, the data and tools included in the full publication are purpose-built to reduce decision latency and financial risk.

PW Consulting stands ready to support tailored briefings, model customizations and vendor diligence in Q1–Q3 2026 to align your strategy with evolving regulatory, technological and supply-chain realities.

For detailed analysis of this topic, please visit the official page:VOC's Rotor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com