Miniaturization Trends and Precision Patterning Drive Dry Film Photoresist Market Growth

Film |

2026-06-09 07:20:18

PW Consulting’s Colocation Market Report (base year 2025; historical window 2020–2025; forecast period 2026–2032) is designed as a decision-grade intelligence package for CIOs, CPOs, infrastructure investors and corporate strategy teams preparing capital, sourcing and sustainability plans in 2026. The colocation market has moved from an early‑stage growth profile into a structurally expanding industry: total market value rose from USD 47.25 Million in 2020 to USD 104.27 Million in 2025 and is projected to reach USD 265.53 Million by 2032, implying a compound annual growth rate of approximately 14.4% through the forecast window. That macro trajectory masks important tactical inflection points enterprises must act on this year; our report converts those inflections into executable choices.

Colocation Market

Regulatory tightening and transparency: Since 2024–2025, major jurisdictions have introduced more prescriptive energy and reporting obligations for data centers (e.g., mandatory PUE and water‑use metrics for larger facilities and new rules shaping how large loads can interconnect to transmission systems). Enterprises must now bake regulatory evidence and compliance into site selection and contract terms rather than treat them as downstream tasks.

Colocation Market

Energy and construction dynamics: Rising construction costs and constrained skilled labor are stretching build timelines and capex; concurrently, energy procurement has become a primary driver of operating cost volatility (notably in primary North American markets where power pass‑through structures dominate). These twin forces shift the risk frontier from “build vs. buy” calculus to “timing and contracting” strategy.

Colocation Market

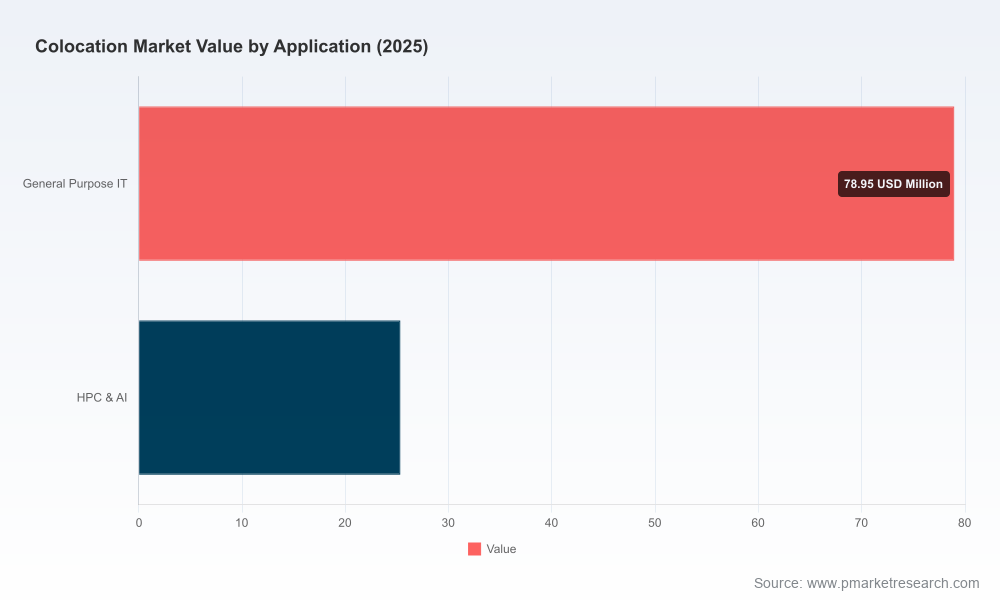

AI and workload density: The surge in high‑density AI and HPC deployments is redefining colocation product design — power density, cooling technology, and interconnection fabric are strategic differentiators. Enterprises planning AI initiatives in 2026 should align procurement cycles with colocation providers’ AI‑ready capacity roadmaps.

Concentration trends: The market exhibits moderate concentration among global providers, with the top tier controlling a notable share of capacity and interconnection capability. That creates differentiated negotiation leverage: hyperscale and global platform providers can deliver scale and cross‑border reach, while regional and specialized operators offer flexibility, speed and tailored compliance solutions.

Our intent is to move beyond forecasting into implementation. The report is organized as a practitioner’s toolkit and includes:

Decision frameworks for site selection that combine latency, data‑sovereignty risk, energy availability, and total cost of ownership (TCO) modelling.

Vendor evaluation scorecards and an enterprise RFP template that prioritize AI‑readiness, interconnection density, sustainability credentials, and contractual flexibility.

CapEx/Opex scenario models and phased build playbooks to compare modular expansion, wholesale‑campus commitments and retail colocation strategies under multiple demand scenarios.

Regulatory and compliance checklists tied to jurisdictional obligations (energy reporting, data‑sovereignty requirements, and transmission interconnection processes), plus recommended contract clauses.

Energy procurement and carbon accounting tools: hedging techniques, renewable PPA structuring options, and practical steps for meeting near‑term Scope 2 goals while preserving operational resilience.

M&A and partnership due‑diligence templates that capture power capacity, interconnection density, build‑ready land, and regulatory encumbrances.

Scenario playbooks for AI/HPC adoption, edge distribution strategies and consolidated regional footprints — each with key KPIs and timing triggers for implementation.

Throughout the report, we preserve granular datasets and interactive dashboards behind the source portal to allow clients to run bespoke analyses while protecting commercially sensitive segment‑level details. The public summary is intentionally selective — deep segment tables, provider scorecards and interactive maps are available on the report landing page.

The colocation provider universe is differentiated along two axes: scale/interconnection reach and product specialization (wholesale, retail, AI/hyperscale, regulated workloads). Our assessment of incumbent and large regional operators frames how enterprises should structure RFPs, risk allocation, and partnership models.

Equinix — global interconnection leader with a strategic focus on enabling hybrid multicloud environments and expanding AI‑ready capacity; recent expansions emphasize data sovereignty controls alongside connectivity breadth.

Digital Realty — a capacity‑centric global operator, strong in wholesale and enterprise colocation; recent site openings and sustainability reporting underline their scale and institutional approach to ESG and campus builds.

Iron Mountain — positioned for regulated and compliance‑sensitive customers, while scaling hyperscale footprints; their certified campuses are attractive for organizations with stringent control requirements.

QTS, CoreSite, Vantage, CyrusOne, Switch, NTT, ST Telemedia — each combines differentiated strengths: high‑density power and interconnection, scalable campus builds for hyperscalers, regional market penetration, or vertical focus. Recent company moves (new campus openings, product reports and regional expansions) indicate a race to lock in AI‑capable capacity and local compliance features.

For enterprises, the practical implication is to treat providers not as commodities but as strategic partners: contract structures should reflect the provider’s strength (e.g., interconnection‑heavy providers for hybrid cloud strategies; wholesale players for large AI deployments; specialized providers for regulated workloads).

Synchronize procurement and capacity timing — If you have planned AI/HPC rollouts, align procurement windows with providers’ announced capacity ramps; early LOIs and staged commitments can secure priority access without full capacity commitment risk.

Embed regulatory compliance into contracts — Mandate reporting rights, audit access, and remediation timelines for PUE and water‑use metrics; insist on data‑sovereignty guarantees where law or policy requires locality.

Hedge energy cost volatility — Negotiate power pass‑through transparency, indexed versus fixed options, and explore aggregated or virtual PPA arrangements with partners to lower scope 2 exposure.

Prioritize interconnection and on‑ramps — For hybrid cloud and multi‑cloud architectures, the value of dense interconnection often exceeds incremental space savings; quantify the operational benefit of on‑ramps to your primary cloud and networking partners when comparing total cost.

Design modular and upgradeable footprints — Favor layouts and mechanical systems that allow for incremental power upgrades and emerging cooling technologies to future‑proof high‑density deployments.

Use M&A selectively — Consolidation can be an effective shortcut to capacity and compliance coverage, but diligence must focus on power entitlements, interconnection contracts and latent liabilities tied to early‑stage campuses.

Distributed Edge + Sovereignty (Latency & Compliance) — Optimal for regulated workloads and latency‑sensitive services; prioritize small regional operators with strong local compliance posture and flexible interconnection.

Hyperscale Partnership (AI & Bulk Capacity) — Suited to enterprises with large, centralized AI/HPC needs; evaluate wholesale campuses and long‑lead commitments with staged expansion clauses and power take‑or‑pay protections.

Hybrid Consolidation (Operational Efficiency) — Combine retail colocation for mission‑critical apps with a centralized wholesale campus for heavy compute; optimize for TCO and minimize replication through robust interconnection strategies.

Leaders should treat the report as an operational playbook rather than a high‑level market brief. Immediate next steps we recommend:

Run the report’s TCO and scenario models against your 3‑ to 5‑year workload roadmap to identify the most cost‑effective mix of retail vs. wholesale colocation.

Use the provider scorecards and RFP templates to short‑list partners and to negotiate clauses that protect against energy and regulatory risk.

Implement the regulatory checklists now — delayed compliance implementations create outsized remediation costs in this cycle.

Engage early with providers on AI capacity roadmap disclosures; secure options and phased rights to avoid being priced out of critical expansion windows.

PW Consulting’s Colocation Market Report combines the macro growth narrative (strong double‑digit CAGR through 2032) with hands‑on tools used by our advisory teams in live transactions. The public summary highlights strategic findings; the full dataset, provider scorecards and interactive planning tools are available on the report landing page for subscribers and corporate clients. For boards and executive teams drafting 2026 capital and sourcing plans, the report is designed to reduce execution risk and convert market growth into durable advantage.

For detailed analysis of this topic, please visit the official page:Colocation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com