Smart Legal & Business Solutions for Modern Enterprises in the UK

Other |

2026-05-21 11:33:27

PW Consulting’s latest market study on Cell Isolation/Cell Separation synthesizes seven years of historical data (2020–2025) and a forward-looking forecast for 2026–2032 to deliver a decision-grade view of one of the fastest-growing niches in life sciences infrastructure. The global market has moved from a sub‑hundred‑million USD sector in 2020 to a robust mid‑hundred‑million USD industry by 2025, and is projected to more than double by 2032. Our base‑case forecast shows the market expanding at a compound annual growth rate (CAGR) of approximately 13.6% during the 2026–2032 period. Market concentration is material — the top three vendors account for roughly half of global revenues and the top five capture close to seven in ten dollars — a structure that creates both stability and strategic entry barriers for challengers.

Cell Isolation/Cell Separation Market

Investors and corporate strategists need forward-looking, executable intelligence rather than descriptive summaries. The rapid adoption of cell therapies, scale-up of GMP processing, and the proliferation of automated platforms mean that supplier selection, capacity planning, and M&A timing are now determinative for value creation.

Cell Isolation/Cell Separation Market

Reimbursement and regulatory shifts are altering the economics of cell processing. Structural changes in payment policy and regulatory designations are creating winners and losers across OEMs, service providers, and contract manufacturers.

Cell Isolation/Cell Separation Market

Adoption is no longer about a single technology; it is about integrated workflows. Buyers evaluate portfolios on throughput, regulatory readiness, closed‑system compatibility, and service models. Our report grades companies and platform archetypes on these procurement criteria.

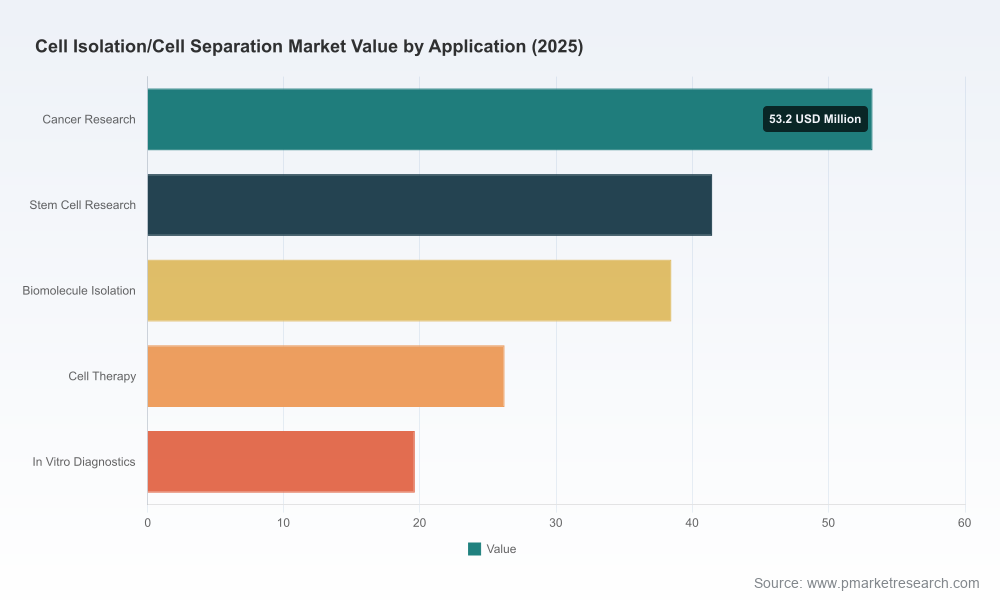

Historical growth from 2020 through 2025 demonstrates durable, demand‑driven expansion as research intensity and clinical translation accelerated in parallel. By our accounting, the market reached approximately USD 178.9 Million in 2025. Under conservative adoption assumptions, the market expands to roughly USD 201 Million in 2026 and, with sustained momentum and technology maturation, reaches an estimated USD 436 Million in 2032. This trajectory—driven by a ~13.6% CAGR across the forecast window—entails predictable near‑term growth with optionality for upside from regulatory approvals, reimbursement recognition, and manufacturing breakthroughs.

The market is anchored by a group of large, well‑capitalized life sciences companies and specialized technology providers whose offerings span consumables, instrumentation, and end‑to‑end automated systems. Our competitive analysis synthesizes product architectures, go‑to‑market models, and recent strategic moves into a pragmatic matrix that buyers and deal teams can use to prioritize partners.

STEMCELL Technologies (Vancouver): Strengths in immunomagnetic selection kits and automated sorting. Recent M&A (June 2025) expanded their high‑throughput sorter capabilities — a move that accelerates their penetration into cell therapy manufacturing.

Miltenyi Biotec (Bergisch Gladbach): Leader in clinical‑grade magnetic‑activated cell sorting and closed automated platforms; strong GMP positioning for translational programs and advanced therapies.

Thermo Fisher Scientific (Waltham): Scale and breadth across reagents, beads and complementary consumables; attractive for organizations seeking end‑to‑end supplier consolidation.

Becton, Dickinson and Company (BD): Flow cytometry and cell sorting systems with deep diagnostic channel relationships — relevant where analytic and process platforms converge.

Danaher/Cytiva, Merck KGaA, Agilent, Beckman Coulter, Terumo BCT, Lonza, and Bio‑Rad: Each brings specific strengths across automation, filtration, closed processing, and cell therapy manufacturing support that make them critical partners for scale‑up and GMP translation.

Two recent developments illustrate how quickly the competitive map can change: STEMCELL’s acquisition to broaden automated sorting for manufacturing, and the commercialization of FACS services by a major testing provider in Germany (January 2025). Both moves signal a maturing ecosystem in which product OEMs, service providers, and contract labs reconfigure to capture higher‑margin manufacturing and clinical translation work.

Reimbursement posture: As of 2026, some payer frameworks have begun to fold autologous cell‑processing steps into bundled payment calculations. This shift compresses the opportunity to separately bill for cell separation services in certain jurisdictions and makes per‑procedure cost profiles and throughput efficiency commercially critical.

Regulatory designations: Select systems and reagents have received targeted regulatory authorizations that create differentiated pathways to clinic. For example, a humanitarian device exemption has been granted for a specific CD34 reagent system — an important precedent that will shape investigational and off‑label usage patterns.

Quality standards: Major platforms are produced under ISO 13485 quality systems and buyers increasingly require validated GMP compatibility and evidence of lot‑to‑lot consistency. Certification and documentation are now procurement gates rather than optional credentials.

Technology approvals: Regulatory designations for processing aids and transient cell line technologies (e.g., recent AMT designations) can materially reduce downstream purification burdens and influence supplier selection for manufacturing stages.

Our full report goes beyond narrative to provide action‑oriented tools and templates that senior executives, product leaders, and M&A teams can apply immediately. Highlights include:

Proprietary market model with historical reconstructions and scenario‑based forecasts to stress test investment cases under alternative adoption and regulatory scenarios.

Vendor benchmarks that score offerings across throughput, purity, automation, regulatory readiness, and total cost of ownership — built from primary interviews, technical datasheets, and lab validations.

Procurement playbooks for large biotech and contract manufacturing organizations outlining RFP templates, KPI scorecards, and supplier risk matrices.

M&A and partnership heatmaps identifying pockets of consolidative value (e.g., high‑throughput sorting, closed‑system GMP processing, consumables consumptivity) and candidate profiles for bolt‑on acquisitions.

Operational checklists for scale‑up, including facility layouts, batch tracking implications, and harmonization requirements when integrating different separation platforms.

For OEMs: Prioritize plug‑and‑play automation and regulatory‑ready kits. Differentiation will come from integrated workflows, validated consumables, and service models that lower downstream validation burden for customers.

For CMOs/CROs: Accelerate investments in closed, GMP‑compatible processing capacity and certify multi‑platform capabilities to capture a growing share of clinical and commercial manufacturing.

For investors: Look for companies with defensible consumables franchises or unique automation IP; the combination of recurring reagent revenue and scalable instrument placements remains the most reliable path to predictable returns.

For hospital systems and diagnostic labs: Reassess billing workflows and form clinical partnerships that offset bundled reimbursement pressures through volume and integrated care pathways.

We designed this study for decision-makers who must translate market momentum into executable plans this year. The report blends quantitative rigor — a transparent market model and sensitivity runs based on regulatory and reimbursement scenarios — with qualitative intelligence (vendor due diligence, primary laboratory validations, and buyer interviews). Rather than a static PDF, subscribers receive an interactive dataset and a modular slide library to adapt material for board briefings, due diligence, and procurement negotiations.

This release intentionally presents an executive preview. The full report contains detailed segmentations, regional breakdowns, downloadable financial models, and vendor scorecards referenced above. If your 2026 strategy depends on supplier selection, capacity expansion, or M&A in cell isolation and separation, we recommend engaging with the full dataset and expert briefing to align timing and execution.

Contact PW Consulting to schedule a live briefing with our life‑sciences practice and obtain the interactive model and vendor benchmarking toolkit.

Subscribe for updates: our research includes rolling intelligence as regulatory decisions and platform approvals occur through 2026–2032.

PW Consulting’s Cell Isolation/Cell Separation Market report converts market momentum into operational plans. The preview above furnishes the strategic context; the full package provides the decision levers. For executives mapping 2026 investments, timing an acquisition, or standing up manufacturing capability, the difference between acting now and waiting could be measured in lost placements and foregone revenue capture.

For detailed analysis of this topic, please visit the official page:Cell Isolation/Cell Separation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com