Inside Residential Boiler Market Analysis Demand Surges

Other |

2026-06-10 09:04:51

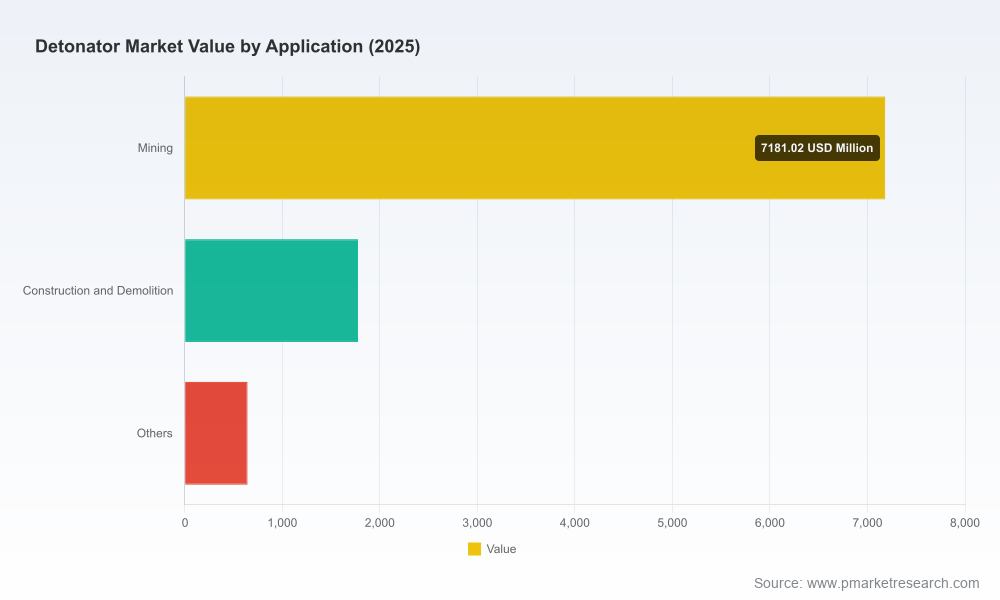

As companies plan capital allocation, procurement strategies, and technology roadmaps for 2026, detonator market choices will materially affect operational safety, project economics, and regulatory compliance across mining, infrastructure and defense applications. PW Consulting’s latest Detonator Market report (base year 2025; historical window 2020–2025; forecast 2026–2032) synthesizes market-scale modeling, supplier capability assessments, supply‑chain stress tests and tactical playbooks designed for senior executives. The market shows steady expansion from 2020 to 2025 and continues to grow into the forecast window: our modeled baseline places the global market at USD 9,600 Million in 2025 and projects continued growth to just over USD 12,000 Million by the end of the 2026–2032 forecast horizon, reflecting a compound annual growth rate (CAGR) near 3.42% under base assumptions.

Detonator Market

Investment timing. Modest but persistent growth and a measured level of supplier concentration mean that marginal investments in manufacturing capacity or digital initiation systems can yield differentiated operational advantages without requiring market‑leading scale.

Detonator Market

Regulatory momentum. Lead-free and defense‑qualification trends are shifting product acceptance criteria across jurisdictions; early adoption avoids retrofit costs and shortens permit cycles.

Detonator Market

Supply resilience. Recent greenfield plant openings and localized manufacturing initiatives indicate that supply risk mitigation is now executable at pragmatic capex levels — a critical consideration for projects with long lead times.

Between 2020 and 2025 the detonator market expanded steadily, reflecting stable demand from mining and construction sectors and incremental adoption of electronic and programmable initiation systems. Our base‑case projection for 2026 anticipates continued expansion, with growth across product categories and geographies driven by automation, safety upgrades, and regulatory-driven product switches (notably lead-free initiatives). The market’s mid‑single-digit CAGR over the forecast period captures maturation dynamics: replacement cycles and conversion to electronic systems sustain volume, while unit value increases reflect premium functionality (programmability, timing precision, and integration with digital blast design tools).

Comprehensive market model (USD Million basis): historical series (2020–2025) and annual forecasts (2026–2032) with sensitivity scenarios (low demand, base, and high digital adoption).

Demand drivers and elasticity matrices: how commodity cycles, construction starts and defense procurement link to detonator demand under different macro scenarios.

Supply‑chain resilience maps: supplier footprints, single‑source risk nodes, and logistics chokepoints with mitigation options (nearshoring, dual sourcing, contract manufacturing).

Regulatory and standards tracker: jurisdictional adoption timelines for lead‑free and defense qualification regimes, and an action checklist for product certification.

Technology and cost curves: unit economics for electric, non‑electric and electronic systems including labor specialization requirements, raw‑material inputs, and automation break‑even models.

Vendor scorecards and commercial playbooks: qualitative and quantitative assessments of leading suppliers, partnership archetypes, procurement negotiation levers, and M&A/ JV decision frameworks.

Implementation roadmaps: six‑ to 36‑month tactical plans to operationalize supplier transitions, pilot programmable detonator systems, or site‑level manufacturing investments.

The detonator market presents a moderate level of concentration: the top three firms account for a meaningful portion of industry revenues while the leading five expand that share further. This concentration level implies that strategic alliances and supplier selection materially influence cost, innovation access and delivery risk. PW Consulting’s report includes vendor profiles and qualitative SWOTs; below is a distilled synthesis of the competitive positioning of core OEMs and system providers.

Dyno Nobel (Salt Lake City, USA) — Positioned as a scale manufacturer with investments in automation and sustainability. Recent deployments of fully automated electronic detonator assembly and renewable energy at manufacturing sites highlight a dual focus on throughput and operating‑cost resilience. Dyno Nobel’s portfolio spans automated electronic detonator plants, non‑electric shock tube systems and established electronic systems, making them a common partner for large mining customers seeking integrated supply and logistics.

Orica Limited (Melbourne, Australia) — Market leader in programmable and lead‑free electronic systems. Orica’s certification activities for lead‑free electronic products and extension of lead‑free NPED technologies demonstrate a proactive regulatory and sustainability posture. This reduces transition friction for European and other regulated markets and supports clients executing multi‑jurisdiction rollouts.

Austin Powder Company (Cleveland, USA) — Offers a diversified initiation portfolio with a mix of electronic, electric and non‑electric detonators. Their product breadth is attractive for industrial blasting projects that require flexibility across timing systems without vendor lock‑in.

MAXAM (Madrid, Spain) & Enaex (Santiago, Chile) — Regional leaders with deep product engineering capability; both bring tailored solutions and local service models that appeal to customers prioritizing responsiveness and lifecycle support.

Chemring, Excelitas & Teledyne — Specialized players serving defense and aerospace niches with qualified detonators meeting stringent standards. Excelitas’ MIL‑DTL qualifications and Teledyne’s EFI/EBW expertise make them strategic partners where government specifications dominate procurement decisions.

Regional and specialty players (BME Mining Canada, Nelson Brothers, Kırlıoğlu, Ideal Mining Services) — Growing local manufacturing footprints and product ranges signal a broader decentralization trend. Recent new‑plant investments and product certifications by regional suppliers reduce single‑supplier exposure for large projects and present options for localized sourcing strategies.

Plant modernizations and new facilities (automation and local manufacturing) reflect a capital cycle focused on resilience and lower operating costs; companies investing in solar arrays and automated lines are reducing both energy cost exposure and workforce dependency.

Lead‑free certification and product expansion are moving from R&D to commercial availability. This regulatory‑driven product shift has direct operational implications: swapping to certified lead‑free systems can eliminate regulatory friction and lower environmental liabilities, but requires coordinated testing and training.

Defense‑grade qualifications remain a differentiator for suppliers seeking to serve government customers; compliance with specifications such as MIL‑DTL supports premium pricing but entails rigorous validation timelines.

Adopt a two‑track procurement strategy: secure short‑term supply via incumbent contracts while piloting programmable/lead‑free systems in low‑risk operations. This balances continuity with future‑proofing.

Prioritize supplier capabilities, not just price: evaluate suppliers on automation maturity, local manufacturing options, certification timelines and spare‑parts logistics. The cost of a month‑long supply disruption often dwarfs procurement savings.

Integrate regulatory change into project economics: model lead‑free adoption and defense qualification requirements in NPV calculations for multi‑year projects. Include certification timelines and pilot costs as explicit project risks.

Invest selectively in vertical resilience: where projects are remote or strategic, nearshoring small‑scale assembly or partnering with regional manufacturers (post‑evaluation) creates both cost and schedule advantages.

Plan for labor and skills: electronic detonator lines require specialized technicians and digital integration expertise. Workforce plans should include training, attrition buffers and partnerships with OEMs for on‑site support.

Use the report’s tactical playbooks: the included supplier scorecards and negotiation levers are designed to reduce procurement lead times and capture commercial protections (inventory consignment, price collars, qualification guarantees).

Week 1–2: Run the market model against your project portfolio to quantify exposure to detonator cost and supply risks.

Week 3–6: Execute supplier capability assessments using PW Consulting’s vendor scorecard templates and shortlist two partners for pilot deployment.

Week 7–12: Launch a pilot (lead‑free or programmable system) on a controlled site, and run the included cost and safety KPIs to validate assumptions before scale‑up.

This briefing intentionally highlights strategic implications and actionable recommendations while withholding granular segmentation tables and specific company market shares that are part of the full PW Consulting Detonator Market report. Detailed regional, type and application splits, full vendor market share matrices, pricing curves, and downloadable Excel models are available exclusively in the full report and accompanying data workbook. For procurement teams, project planners and corporate strategists seeking the underlying datasets and step‑by‑step implementation tools that inform the recommendations above, the report provides the empirical foundation to execute decisions in 2026 with confidence.

Contact PW Consulting to access the full report, scenario models, and vendor scorecards — and to schedule a tailored briefing focused on your portfolio’s detonator risk and opportunity profile.

For detailed analysis of this topic, please visit the official page:Detonator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com