Floating Storage Regasification Unit Market Size Forecast by Capacity and Deployment

Other |

2026-02-06 11:46:25

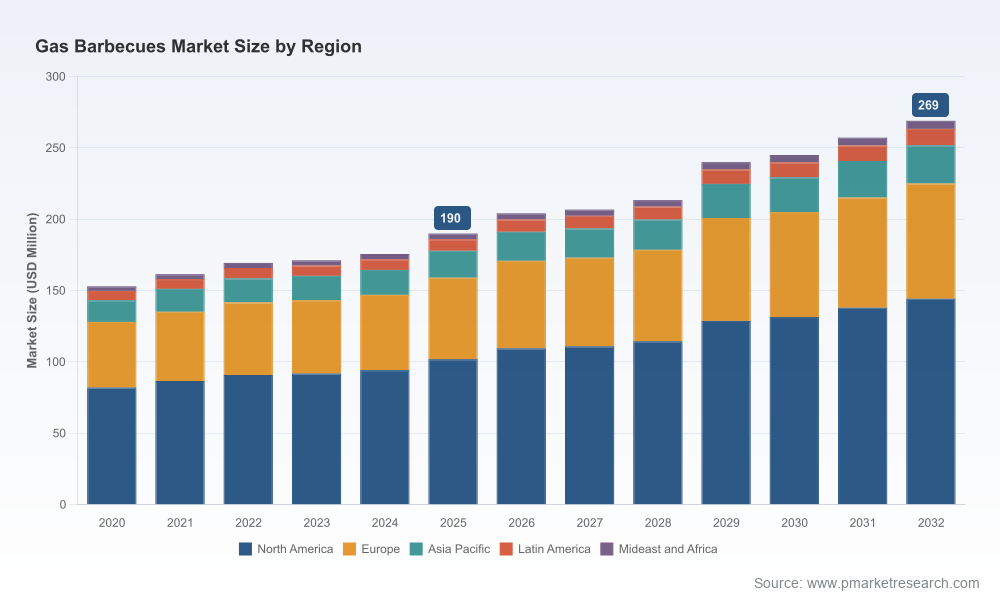

As organizations prepare investment and product roadmaps for 2026, the Gas Barbecues Market presents a clear, investable growth story anchored by steady demand, concentrated competition, and accelerating product innovation. Our PW Consulting analysis uses 2025 as the base year and examines historical activity from 2020–2025, then forecasts the market through 2026–2032. The market expanded from roughly USD 153 million in 2020 to USD 190 million in 2025, and we project continued expansion at a compound annual growth rate of 5.1% over the forecast period, reaching approximately USD 269 million by 2032. Crucially, the market is meaningfully concentrated: the top three firms command roughly two‑thirds of market share, and the top five account for about 80% — a structure that creates both defensive barriers and specific opportunity windows for challengers and adjacencies.

Gas Barbecues Market

Technology convergence: Smart connectivity and hybrid-cooking concepts are moving from premium niche to mainstream consideration. Companies that integrate reliable IoT features and meaningful user experiences — rather than superficial connectivity — will capture outsized wallet share.

Gas Barbecues Market

Regulatory and standards tightening: Adoption of fire-safety provisions aligned with NFPA guidance, local permitting for externally connected gas appliances, and heightened inspection regimes are re-shaping compliance costs and channel requirements for installers and retailers.

Gas Barbecues Market

Input-cost and material dynamics: The industry’s reliance on 304 stainless steel has implications for sourcing, lead-times, and cost pass-through strategies. Manufacturers that lock predictable supply or redesign for resilience will protect margins.

Consolidation and channel shifts: High concentration raises the prospect of portfolio optimization through M&A, private-label partnerships, and strategic distribution agreements — particularly for international players targeting established markets.

The macro trajectory — a progression from ~USD 153 million in 2020 to USD 190 million in 2025 and toward roughly USD 269 million by 2032 — signals predictable, above-inflation expansion rather than volatile boom-bust cycles. Year-on-year growth in the immediate post‑pivot years shows moderate resilience, while mid- to late‑forecast years reflect acceleration as product upgrades, outdoor-living investments, and replacement cycles converge.

For corporate strategy, this translates into three practical implications for 2026 planning: (1) capacity and capex should be rightsized to a stable-growth environment, (2) premium and technology-led SKUs will justify higher ASPs and margin uplift if supported by service ecosystems, and (3) sales and aftercare investments are as consequential as product innovation for long-term retention.

The market’s competitive structure is dominated by a small group of established manufacturers and a number of specialist players. Leading firms have distinct strategic postures:

Weber Inc. (Chicago) continues to lead through scale, manufacturing presence in the U.S., and an expanding product stack — including iterative launches that emphasize ignition reliability and, most recently, integrated Wi‑Fi/Bluetooth capabilities aimed at ecosystem lock-in.

Coleman leverages portability and brand familiarity to defend share in the on-the-go segment, while Bull Outdoor Products and Lynx Grills double down on premium positioning and outdoor-kitchen integration for affluent consumers.

Char‑Broil and Masterbuilt focus on broad retail distribution and aggressive value propositions; Char‑Broil’s proprietary cooking systems continue to be a differentiator in mass channels.

Traeger’s hybrid and pellet-oriented technology is pushing adjacent category expectations, provoking incumbents to experiment with hybridization and smarter thermal control.

Regional manufacturers and specialists (e.g., Onward Manufacturing) remain important partners for B2B and commercial channels, often providing customization, OEM supply, and regional compliance expertise.

Notable recent moves underscore the tempo of innovation: Weber’s 2025 Spirit lineup introduced improved ignition and thermal control, and its 2026 rollout includes smart models compatible with a vendor app; Napoleon has pushed promotional activity around new Prestige PRO models in 2026. These tactical plays demonstrate a two-track competitive approach across players: continuous product improvement for the mid-market and periodic smart-feature introductions aimed at value capture.

Safety and inspection regimes: State-level adoptions of NFPA‑aligned fire-safety standards and local agency requirements for permitting and inspection (including specific rules for outside gas appliances) increase the importance of compliance-ready installation services and certified dealer networks.

Materials and supply-chain pressure: Industry norms around 304 stainless steel for grates and housings imply exposure to commodity cycles. Manufacturers should model multi-supplier contracts, forward buys, and design-for-cost alternatives to maintain gross-margin stability.

Channel and installation risk: Where permits and inspections are required, manufacturers that provide retailer/installer certification programs, digital documentation, and integrated service bundles reduce abandonment and returns while improving end-user trust.

Prioritize smart features that add operational value: Focus R&D on connectivity that meaningfully assists cooking outcomes (e.g., closed‑loop temperature control, recipe guidance, service diagnostics) rather than one-off app toggles.

De-risk supply of key materials: Lock multi-year agreements for 304 stainless steel where economics permit, and invest in design modularity that allows controlled substitution without compromising durability.

Build compliance-forward go‑to‑market channels: Develop certified installer networks, digital permit support, and bundled warranty/service offers to reduce friction in jurisdictions with strict inspection policies.

Segment pricing and SKU depth: Allocate premium SKUs to channels where service and installation are tightly managed, and keep value-driven configurations in mass retail with lean service commitments.

Use M&A and partnerships tactically: With top-five players accounting for a large portion of the market, bolt-on acquisitions and licensing deals are attractive routes for scale and capability acquisition—particularly for technology, distribution, and outdoor-kitchen integration.

Stress-test scenarios for 2026 capital allocation: Run downside scenarios that include raw-material cost spikes and permit-related sales frictions; ensure new product investments achieve payback under conservative assumptions.

Our full report is designed as an executable kit for 2026 decision-making. Deliverables include a concise executive playbook, scenario-based financial models you can drop into your planning, go-to-market templates for channel segmentation and installer certification, supplier scorecards for materials sourcing, product roadmaps aligned to consumer willingness-to-pay bands, and a competitor playbook that synthesizes public filings, product launches, and promotional calendars.

Importantly, this release is a strategic preview: we surface the underlying dynamics, competitive moves, and recommended actions to build confidence for immediate planning. To preserve commercial value and encourage direct engagement, we intentionally withhold granular regional and application-level split datasets in this summary. These detailed segmentations, price-band matrices, and market-share tables are included in the full report and online data portal.

Immediate (0–90 days): Run a sourcing stress-test for 304 stainless steel, validate the product roadmap against the connectivity playbook, and initiate installer-certification pilots in high-inspection states.

Near-term (90–180 days): Finalize SKU rationalization, commit to targeted promotional calendars for summer windows, and evaluate opportunistic M&A targets identified in our competitive benchmarking.

Parallel: Integrate compliance documentation and digital permit workflows into your dealer portals to reduce friction and speed point-of-sale conversions where inspection regimes apply.

The Gas Barbecues Market in 2026 offers a durable growth runway driven by product innovation, outdoor living investment, and replacement cycles. Success will accrue to firms that combine disciplined supply-chain management, compliance-enabled distribution, and technology that genuinely enhances the consumer cooking experience. PW Consulting’s Gas Barbecues Market report converts these insights into operational tools you can use to shape 2026 budgets, capex allocations, and go‑to‑market plays.

For access to the full dataset — including detailed regional, type, and application segmentations, price-band analytics, and the downloadable financial models — please visit our report page to download the complete study and associated spreadsheets. PW Consulting’s team is also available for bespoke briefings to translate the findings directly into your 2026 strategic plan.

For detailed analysis of this topic, please visit the official page:Gas Barbecues Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com