Laboratory Equipment Market Dynamics and Competitive Landscape

Other |

2026-03-24 04:44:22

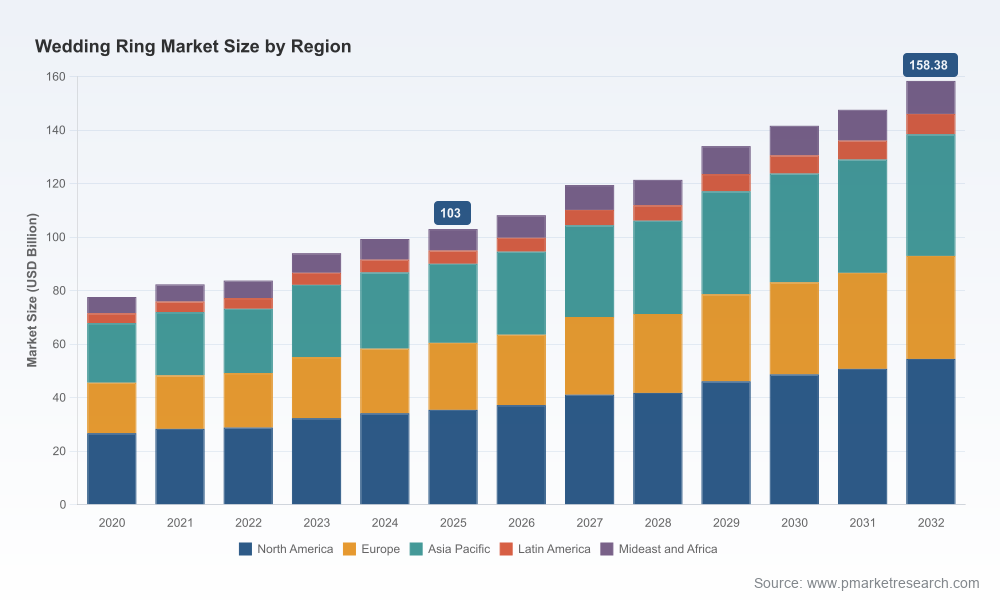

As wedding markets rebound and consumer preferences fragment, the global wedding ring market is entering a phase of structural evolution that will define winners and losers through 2026 and beyond. PW Consulting’s newly released market study — grounded in a 2020–2025 historical review and a 2026–2032 forecast horizon — delivers a pragmatic road map for executives seeking to convert market transition into profitable growth. The market, which expanded materially through 2020–2025 and reached an estimated USD 103.0 Billion in 2025, is projected to grow at a compound annual growth rate (CAGR) of 6.5% across our forecast window, reaching roughly USD 158.4 Billion by 2032. This brief outlines the strategic value of the full report for 2026 decision cycles and highlights the near-term plays that matter most.

Wedding Ring Market

Actionable foresight: We translate macro growth (CAGR and top-line sizing) into targeted operational and commercial initiatives that can be executed within typical corporate planning cycles.

Wedding Ring Market

Risk-adjusted scenarios: The study includes alternative scenarios reflecting raw-material shocks, ethical-sourcing premiums, and accelerated digital adoption — enabling finance and strategy teams to stress-test budgets and capex plans.

Wedding Ring Market

Competitive positioning: A non-linear competitor canvas and capability assessment help firms identify realistic pathways to defend margins or scale quickly via M&A and partnerships.

Practical toolkits: From channel-playbooks to SKU rationalization templates, the report emphasizes executable workstreams over academic charts.

Comprehensive market sizing — base-year granularity (2020–2025) and a 2026–2032 forecast model with downloadable scenario drivers and sensitivity tables.

Demand segmentation framework — consumer archetypes, purchasing triggers, and lifecycle cohorts that determine spend and product preferences.

Channel success playbooks — digital-first strategies, omnichannel conversion levers, and retail footprint optimization templates designed for rapid pilot and scale.

Raw-material and supply-chain stress-tests — modeled impacts of precious metal price shocks, supplier concentration, and lead-time disruption on gross margins and working capital.

Product and price architecture — elasticity matrices, SKU rationalization blueprints, and margin-improvement levers organized by product family.

Competitive benchmarking — capability heat-maps, go-to-market archetypes, and a prioritized list of acquisition or alliance targets based on strategic fit.

Investment and M&A playbook — valuation sensitivities, integration risks, and transaction checklists tailored to jewelry and luxury consumer assets.

Executive dashboards and 90-day implementation plans — ready-to-use decision aids for boards and operating committees.

Raw-material volatility: Precious metal markets experienced significant turbulence in 2025, with headline gold prices moving to record territory. That volatility directly compresses gross margins for non-hedged sellers and elevates the value of procurement sophistication. Our report models multiple price-paths and their P&L consequences.

Ethical sourcing as a commercial lever: Demand for responsibly sourced metals and diamonds has moved beyond compliance into a measurable willingness-to-pay among specific consumer cohorts. Brands that can credibly demonstrate provenance — and operationalize traceability — convert ethics into differentiation rather than cost.

Design personalization and modularity: Customizable, stackable, and comfort-fit designs are not fleeting trends. They represent a structural shift toward modular product architectures, enabling higher attachment rates and repeat purchases if supported by production agility and digital configurators.

Channel friction and opportunity: Digital channels continue to accelerate discovery and pre-purchase research, while physical retail remains a conversion and service anchor for higher-ticket commitments. Winning omnichannel approaches integrate virtual try-ons, transparent policies, and seamless fulfillment to preserve margin.

Consolidation pressure: Market concentration metrics reveal a sector where top incumbents control meaningful shares of demand. This concentration both stabilizes certain market segments and creates windows for strategic M&A, private-label manufacturing scale-ups, and specialty entrants to capture niche value pools.

Artcarved (New York, USA) — A heritage manufacturer with a strong product identity in carved and comfort-fit bands. Strategic implication: leverage craftsmanship story while pairing with modern e-commerce UX to unlock younger segments seeking legacy aesthetics in a contemporary purchase journey. Consider limited-edition collaborations and a comfort-fit subscription/upgrade program.

Brilliant Earth (San Francisco, USA) — Positioned as an ethical-sourcing and provenance leader. Strategic implication: accelerate monetization of traceability through premium provenance tiers, certification services, and B2B white-label offerings for retail partners seeking ethical credentials.

Tacori (California, USA) — Known for American-made, customizable engagement models. Strategic implication: scale personalization via configurable online builders and localized manufacturing to shorten lead times; explore premium warranty and lifetime servicing bundles as additional margin drivers.

Whiteflash (New York, USA) — Differentiates on gem-performance and cut quality. Strategic implication: productize technical superiority for informed buyers through immersive content and performance guarantees; pursue partnerships with labs and certification bodies to institutionalize the quality signal.

Shane Co. (Minneapolis, USA) — Family-owned omnichannel retailer with integrated inventory. Strategic implication: optimize inventory velocity through micro-location analytics, implement dynamic pricing experiments, and deepen CRM-driven lifetime-value programs to defend local markets.

JewelPin (USA) — Global manufacturer and wholesaler focused on ready-to-ship models. Strategic implication: scale B2B fulfillment, offer private-label tooling, and bundle digital catalog APIs to retailers seeking rapid assortment expansion without inventory strain.

The market concentration profile indicates substantive influence by leading firms, but also meaningful adjacency opportunities for mid-market players. Firms focused on vertical integration (from sourcing through retail), proprietary design IP, and digital experience can capture disproportionate share gains. Our report identifies sweet spots for bolt-on acquisitions — such as regional retail chains, artisanal workshops with IP, and tech-enabled personalization platforms — and outlines integration priorities that preserve brand equity while driving margin uplift.

30 days — Rapid diagnostic: run a margin sensitivity exercise using report-provided price and cost shock scenarios; identify three SKU lines most at risk from raw-material moves.

60 days — Pilot & partnerships: select one channel experiment (virtual try-on, provenance tag, or configurator) and one supply-side pilot (procurement hedge or contract with traceable source). Use our playbook to scope KPIs and budgets.

90 days — Scale decision: deploy the winner from pilots with defined ROI thresholds; consider targeted M&A or strategic alliances described in the M&A playbook to accelerate capability build.

Rather than offering only descriptive analysis, our study is structured around decision-quality outputs: scenario-ready financial models, prioritized implementation roadmaps, and vendor-neutral playbooks that counsel executives on "what to do next" rather than "what happened." We combine granular commercial insights with practical operating levers — from SKU rationalization matrices to distributor negotiation scripts — enabling leadership teams to move from insight to action in a single planning cycle.

This article is intended as a strategic preview. The full PW Consulting Wedding Ring Market Report includes complete segmented data tables, regional dashboards, channel-specific forecasts, supplier concentration maps, price-elasticity matrices, and company-level benchmarking. To access the granular segmentation, downloadable models, and ready-to-run operational templates that underpin the recommendations summarized here, visit our report page and download the executive pack. For bespoke briefings, scenario runs, or integration support, PW Consulting’s strategy team is available to partner on rapid deployment projects tailored to your organizational priorities for 2026.

For detailed analysis of this topic, please visit the official page:Wedding Ring Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com