Social Media Analytics Market Is Becoming the Decision Engine Behind Digital Marketing

Networking |

2026-05-26 11:21:09

As demand for naturally derived actives tightens across cosmetics, nutraceuticals and specialized food formulations, the Natural Ferulic Acid market has entered a phase of measured acceleration. PW Consulting’s newly published market study — anchored on a 2025 base year with a 2026–2032 forecast horizon — provides the strategic view senior executives need to translate macro growth into defensible commercial moves in 2026. This briefing summarizes the report’s most consequential insights while intentionally reserving granular segmentation data to encourage direct engagement with the full study.

Natural Ferulic Acid (CAS 1135-24-6) Market

Over the 2020–2025 historical window the Natural Ferulic Acid market demonstrated steady expansion, reflecting both recovery dynamics after global supply shocks and expanding end‑use adoption. Our base‑year estimate (2025) places the market at approximately USD 57.3 Million (revenue unit: Million). Under a mid‑case scenario, the market is projected to grow at a compound annual growth rate (CAGR) of 6.7% through 2032, reaching roughly USD 90.2 Million by 2032. That pace signals a market that is neither a fast‑moving commodity sprint nor a slow, mature decline, but rather a stable, innovation‑driven specialty ingredient market with attractive margins for upstream and differentiated downstream players.

Natural Ferulic Acid (CAS 1135-24-6) Market

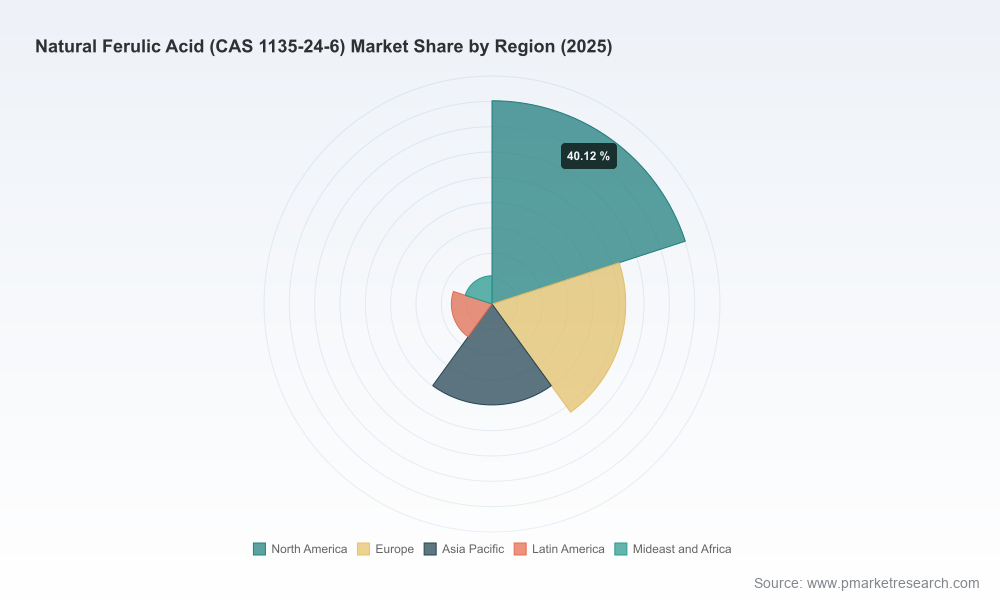

Concentration metrics reveal an industry with moderate fragmentation: the three‑player concentration (CR3) is in the mid‑30s percent range while the top five (CR5) cluster near the low‑40s percent range. In practice, this means there is room for scale advantages, but also meaningful opportunities for niche and regional specialists to succeed by optimizing feedstock, purity and formulation synergies.

Natural Ferulic Acid (CAS 1135-24-6) Market

The market is meaningfully defined by three practical levers: feedstock efficiency, purity and application tailoring. Natural ferulic acid is predominantly derived from agricultural byproducts; rice bran and wheat bran are the most common sources. Differences in extraction technology — enzymatic hydrolysis, solvent‑based extraction, and increasingly proprietary biomass conversion techniques — drive unit economics and environmental footprint. Across the supply chain, manufacturers that combine stable feedstock access with high extraction yields and robust quality controls command stronger margin profiles.

From a demand perspective, cosmetics (topical antioxidants and UV‑stabilizing systems), pharmaceuticals (formulation stabilizers and intermediates) and functional food/beverage applications remain the primary end‑use domains. Each use case requires distinct technical documentation, dose justification and, in some jurisdictions, additional regulatory dossiers — creating an ecosystem in which technical service capability matters as much as price.

Our competitive review identifies a mix of established specialty manufacturers and agile regional suppliers. Below are high‑level strategic characterizations of the most commercially consequential players, followed by recent notable moves.

Recent company activity warrants close watching. TSUNO Group’s 2026 exhibition and product launches underscore a strategic pivot: leveraging domestic rice‑bran sourcing to create consumer‑facing “eating beauty” portfolios that blur the line between ingredient supplier and branded product maker. For incumbents and new entrants alike, this highlights two practical takeaways: (1) intellectual property and branding in downstream applications can command higher margins, and (2) trade‑show and launch activity are leading indicators of mid‑term channel disruption.

For decision makers planning 2026 budgets and strategic moves, our full report goes beyond narrative to provide pragmatic toolkits that can be deployed immediately. Highlights include:

These modules are designed to move executives from awareness to execution within 90–180 days.

Natural ferulic acid offers an attractive combination of stable mid‑single digit growth and premiuming potential when paired with application innovation and robust sourcing strategies. Firms that treat feedstock risk as a strategic variable — not just an input cost — and that couple procurement sophistication with formulation R&D will be best positioned to capture disproportionate value as the industry scales toward the forecasted market size in 2032.

PW Consulting’s full Natural Ferulic Acid (CAS 1135-24-6) Market report contains the granular segmentation, regional and application maps, supplier scorecards and financial models that underpin the strategic recommendations summarized above. For executives preparing capital plans and product roadmaps in 2026, the report offers the economic and competitive intelligence required to convert market growth into commercial advantage.

To access the complete dataset, scenario models and supplier benchmarking modules, contact PW Consulting or visit our report page for subscription options and bespoke advisory support.

For detailed analysis of this topic, please visit the official page:Natural Ferulic Acid (CAS 1135-24-6) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com