Plant Protein Ingredients Market Revenue Growth Driven by Rising Consumer Preference for Plant-Based Foods

Food |

2026-06-05 17:00:30

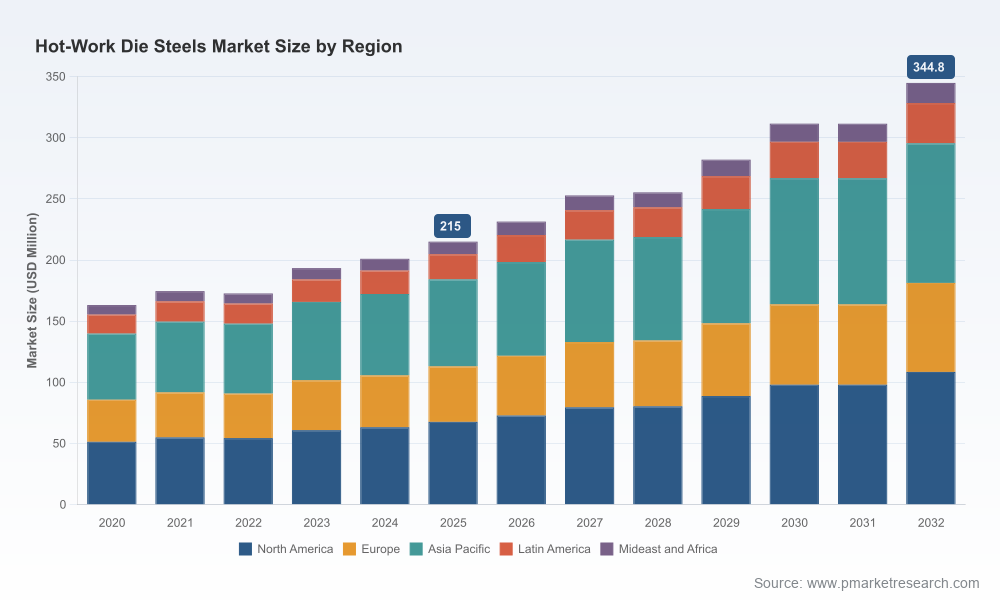

PW Consulting’s Hot-Work Die Steels Market study (base year 2025; historical 2020–2025; forecast 2026–2032) highlights a market transitioning from steady post‑pandemic recovery into structurally higher demand driven by industrial reshoring, advanced materials uptake and regulatory realignment. Measured in USD Million, the total market expanded from USD 163.15 in 2020 to USD 215.0 in 2025, and our forward model projects a rise to USD 344.8 by 2032 at a compound annual growth rate (CAGR) of 6.98% across the 2026–2032 forecast window. For executives preparing capital allocation, sourcing shifts or product roadmap decisions in 2026, this report functions as an operational playbook: it connects macro trends to near‑term tactical moves while preserving the competitive intelligence that is only released in full through the report package.

Hot-Work Die Steels Market

Regulatory inflection points: New European import alignment measures and tightened emissions limits for specialty-steel melting raise the cost and complexity of cross‑border sourcing starting in 2026.

Hot-Work Die Steels Market

Technology and labor dynamics: Advanced vacuum hardening and other high‑temperature processing technologies are accelerating product performance expectations, and specialized heat‑treatment skills have risen materially in cost and scarcity.

Hot-Work Die Steels Market

Product and supplier consolidation: Recent grade introductions and corporate transactions are accelerating consolidation among high‑quality tool‑steel producers, changing supplier selection calculus for die makers and OEMs.

The dataset underlying PW Consulting’s forecast shows a clear recovery and acceleration pattern: five years of historical behavior (2020–2025) provide the calibration layer; the model then incorporates regulatory, raw‑material and technology shocks to output the 2026–2032 trajectory. Practically, the market’s rise from USD 215.0 (base year 2025) to USD 344.8 by 2032 reflects more than cyclical demand — it indicates structural volume and value expansion driven by higher grade penetration, longer service‑life product specifications and increased demand for specialty grades in high‑performance die applications. The forecast CAGR of 6.98% is therefore not a passive estimate; it is the result of scenario‑weighted drivers embedded in the model.

Supply‑chain repositioning under carbon and border measures: Starting in 2026, import parity and carbon‑adjusted tariffs are creating an incentive to localize higher‑value specialty‑steel supply or to secure long‑term contracts with aligned suppliers. For procurement teams this means re‑pricing scenarios, renegotiation clauses tied to CO2 intensity, and preemptive qualification of alternate producers.

Raw‑material quality premium: Hot‑work die steels rely on high‑purity chrome‑molybdenum‑vanadium alloy inputs to meet elevated‑temperature strength and wear resistance targets. Buyers and R&D functions should budget for tighter input specs and accelerated testing cycles in 2026 as premium feedstock availability tightens.

Standards and specification evolution: ISO 4957:2018 (and related national adoptions) now imposes stricter impact and toughness expectations for hot‑work steels. Engineering teams must integrate these minimums into die design standards and QA protocols to avoid field failures and warranty exposure.

Procurement: Implement a two‑track sourcing strategy — secure continuity through existing relationships while onboarding 1–2 lower‑risk regional suppliers to mitigate CBAM exposure. Negotiate CO2‑indexed pricing or off‑take agreements to stabilize cost. Build a short list of capability‑verified mills with vacuum‑furnace heat‑treatment partners.

Manufacturing and CapEx: Prioritize investments in vacuum‑hardening and thermal‑management equipment that improve die life and reduce cycle time. Small, targeted investments in in‑house heat‑treatment capability can be highly accretive for mid‑sized die makers facing rising external heat‑treatment rates.

Product strategy and R&D: Accelerate trials of higher‑conductivity and high‑temperature‑strength grades to reduce cycle cooling time and stamping/deformation defects. Design for maintainability: specify modular inserts or surface treatments that allow service without full die replacement.

M&A and partnerships: The sector remains fragmented (market concentration measures indicate that the top participants control well under a third of overall market revenues), creating pockets of consolidation value. Targeted acquisitions, joint ventures or toll‑manufacturing agreements can accelerate access to premium grades and local heat‑treatment capacity.

Our company coverage includes global producers and regional specialists that together form the supply backbone for hot‑work die steels. Key players profiled in the report include Daido Steel Co., Ltd., Kind & Co. / Edelstahlwerk, Schmiede Werke Gröditz GmbH, Nippon Koshuha Steel, Sanyo Special Steel, Proterial (YSS), Severstal, Eramet, and a wider universe of producers across Europe, Japan, India, China and North America. Each profile maps product portfolios (e.g., H13 variants, specialized grades for extrusion and die casting), capability nodes (ESR/VAR, vacuum heat treatment, large‑scale forging) and commercial positioning.

Notable recent developments underline accelerating product and corporate moves: Swiss Steel Group launched an optimized high‑performance die grade in November 2025 aimed at extending die life for high‑pressure die casting; and GMH Gruppe consolidated several German tool‑steel assets into an integrated open‑die forging group in January 2026, including a multi‑million euro investment in Gröditz to increase throughput. These dynamics reinforce the need to monitor new‑grade introductions and regional consolidation for supplier risk and opportunity mapping.

Environmental regulation: European emission standards for electric‑arc furnace specialty‑steel production are tightening allowable CO2 per ton metrics, with direct implications for production cost and export competitiveness. Expect upstream decarbonization investments to translate into price premia for lower‑carbon steels.

Border measures: The EU Carbon Border Adjustment Mechanism (CBAM) imposes a new regime beginning in 2026 that changes relative cost dynamics for imported specialty steels. Corporates should model CBAM impact on landed cost and supplier scorecards.

Talent and skills: Advanced heat‑treatment technologies have driven a ~12% increase in specialized labor cost since 2024. This tightness affects throughput and recovery rates post‑repair and increases the ROI threshold for automation and training investments.

Proprietary market model (2020–2032) with scenario toggles for policy, raw‑material shocks and technology adoption — base year 2025, USD Million reporting.

Supplier capability matrix and vetted shortlists by capability (heat treatment, ESR/VAR, large forging) with audit checklists for rapid supplier qualification.

Procurement playbook with contract templates for CO2‑indexed pricing, quality acceptance criteria tied to ISO 4957 benchmarks, and sample risk‑sharing terms.

Capital allocation guide for in‑house heat‑treatment and furnace upgrades, including payback curves under three demand scenarios.

Competitive profiles and a forward watchlist of 25+ producers, detailing new‑grade launches, capacity investments and M&A catalysts.

Actionable risk matrix and mitigation roadmap for 18 discrete threats (raw‑material shortages, tariff shocks, talent gaps, regulatory changes).

As a preview, the executive release intentionally omits granular regional and application split tables and confidential supplier scorecards — these are available only in the full report and supporting Excel deliverables.

90 days: Rebase supplier scorecards to include CO2 intensity and heat‑treatment capability; initiate contractual amendments with top two suppliers to include price‑and‑carbon adjustment clauses.

180 days: Pilot a premium grade trial on a high‑value die family; evaluate short‑list partners for toll‑heat‑treatment or localized billet supply to mitigate CBAM exposure.

360 days: Decide on CapEx for vacuum hardening or forge investments based on pilot outcomes; consider merger or minority investment to secure long‑term access to high‑purity alloy feedstock.

For 2026 corporate planning cycles, the Hot‑Work Die Steels Market is no longer a commodity tale of volume alone. The interaction of higher‑performance material requirements, localized regulatory costs and skill scarcity is creating a bifurcated market: premium, lower‑carbon, technically advanced grades versus commodity replacement steels. Winning in 2026 will require cross‑functional coordination between procurement, engineering and corporate development informed by robust scenario analysis.

PW Consulting’s full Hot‑Work Die Steels Market report provides the depth, tools and supplier intelligence to convert these insights into executable programs. This release is a strategic trailer — it demonstrates the analytical rigor and operational frameworks we deploy while intentionally withholding the full subsegment tables and confidential appendices that unlock tactical advantage. For access to the complete dataset, supplier scorecards and the downloadable model, please contact PW Consulting or visit our website to obtain the full report package.

For detailed analysis of this topic, please visit the official page:Hot-Work Die Steels Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com