Mattress Ticking Fabric Market: Insights and Competitive Analysis

Other |

2026-02-26 05:30:55

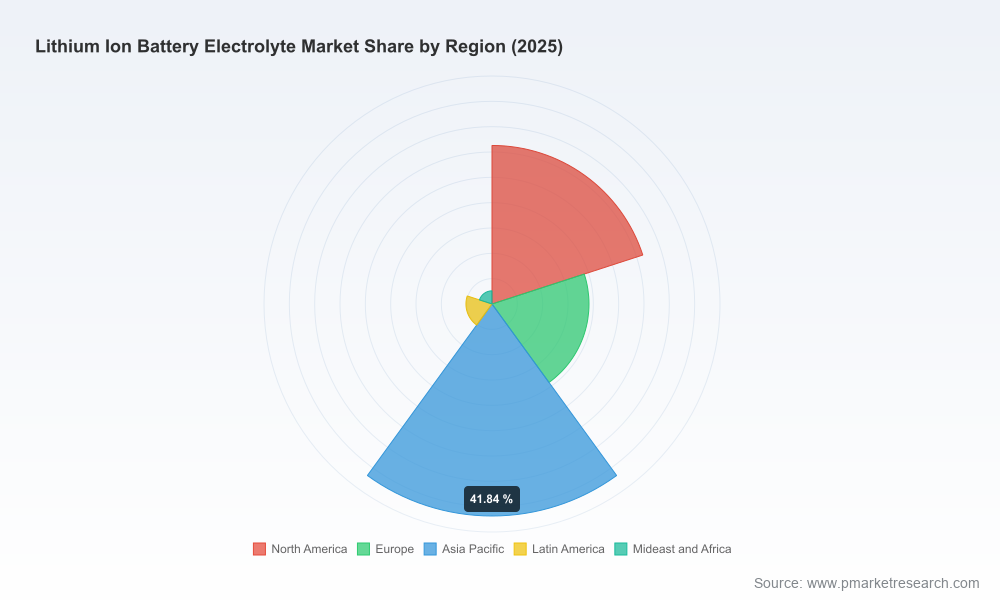

PW Consulting’s forthcoming market research brief on the Lithium‑Ion Battery Electrolyte Market synthesizes a multi‑year quantitative backbone with practitioner‑grade strategic frameworks tailored for 2026 decision cycles. Our base year for detailed benchmarking is 2025; the market we track has expanded rapidly since 2020 and, under our central forecast, is expected to grow at a compound annual growth rate (CAGR) of 12.94% through the 2026–2032 horizon. By 2025 the global lithium‑ion electrolyte market reached a sizable multi‑billion dollar scale, and our scenario envelopes project continuing expansion to material levels by 2032. This preview highlights the actionable insights, the competitive anatomy, and the decision frameworks that make the full report an operational asset for executives, corporate development teams, and procurement leaders preparing for 2026.

Lithium Ion Battery Electrolyte Market

Electrolyte purchasing is now a strategic lever, not a commodity buy. The shift from intermittent supply constraints to structured capacity investments means purchasing decisions influence product roadmaps, qualification timelines, and vehicle/program eligibility—especially for automotive OEMs and energy storage system (ESS) integrators.

Lithium Ion Battery Electrolyte Market

Policy and regionalization dynamics are re‑ranking supplier choice. Incentives and content rules in major markets are accelerating on‑shore and near‑shore manufacturing investments, altering total delivered cost calculations and qualification risk profiles for cell makers and OEMs.

Lithium Ion Battery Electrolyte Market

Raw‑material volatility is amplifying margin and supply risk. Salt and precursor price dynamics have shown marked volatility across 2025–26, increasing the premium on hedging strategies, vertical integration options, and substitute salt research.

Technology inflection points — from liquid to gel to solid chemistries — have elevated the value of flexible supply chains and modular qualification strategies. Pragmatic roadmaps are required to manage concurrent programs across multiple electrolyte technology classes.

High‑fidelity market sizing and trend tracing: historical reconstruction for 2020–2025 plus a transparent forecasting model for 2026–2032, including sensitivity to demand, raw‑material scenarios, and policy shocks.

Commercial playbooks: supplier selection matrices, contractual terms to mitigate supply and specification risk, and commercial scorecards to evaluate OEM/ESS supplier alignment.

Operational due diligence templates: factory capability checklists, technology readiness roadmaps, and sample KPI templates for qualification and ramp‑up phases.

M&A and JV screening: an actionable checklist that translates market concentration and competitive positioning into prioritized targets and red‑flag items for transactional teams.

Raw‑material risk toolkit: scenario tables, hedging playbooks, and a model that links salt and solvent price feeds to EBITDA impact by product mix (delivered in an editable spreadsheet).

Regulatory and compliance impact analysis: coverage of emerging rules that affect plant siting, waste streams, and program eligibility in priority markets.

The market demonstrates moderate concentration: the top three suppliers account for a majority share of the market’s active commercial capacity, and the top five increase that concentration materially. For strategy teams this concentration profile creates both risk (single‑source dependencies for critical chemistries) and opportunity (clear leaders to engage for strategic supply partnerships).

Key industry players we analyze in depth include, among others:

Mitsubishi Chemical Corporation (Tokyo) — notable for high‑purity liquid electrolyte lines and recent capacity moves oriented to serve North American cell manufacturers aligning with regional policy requirements.

Green Energy Origin (GEO) (Weinheim) — an upstream‑to‑electrolyte integrator with cross‑border manufacturing and recent strategic asset acquisitions that extend its footprint in North America and Europe.

Guangzhou Tinci Materials Technology (Guangzhou) — a vertically broad supplier that spans liquid electrolytes, lithium salts and additives, and is active in long‑term commercial agreements with major battery makers.

Shenzhen Capchem (Shenzhen) and Shanshan Technology (Dongguan) — incumbent high‑purity electrolyte and additive specialists supporting automotive and ESS programs.

Soulbrain (Seoul) and Panax Etec (Seoul) — technology‑focused suppliers emphasizing proprietary purification and additive technologies for premium applications.

Zhangjiagang Guotai‑Huarong, Shandong Shida Shenghua, UBE Industries and BASF — regional and global players with capabilities across electrolytes and battery chemical portfolios.

Recent strategic moves point to consolidation and capacity re‑balancing: selected incumbents have divested or sold assets to regional integrators, new plant announcements target policy‑sensitive markets, and a number of long‑term offtake arrangements between electrolyte makers and cell manufacturers have been publicized. Simultaneously, a significant proposed project in the industry was terminated, underscoring that capital discipline and execution risk remain central to strategy formation.

Base case (policy‑driven growth): continued strong EV and ESS demand, regional incentive alignment, and manageable raw‑material cycles. Actions: secure multiyear offtake, accelerate qualification pipelines, and invest in regional fill‑and‑finishing capacity where it shortens lead time.

High‑cost raw materials: persistent elevated salt and solvent costs. Actions: hedge via long‑dated supply agreements, accelerate Li‑salt diversification programs, and model pass‑through mechanisms into customer contracts.

Technology shift (accelerated solid‑state adoption): a faster-than‑expected conversion to non‑liquid electrolytes for select applications. Actions: prioritize R&D partnerships, create hybrid supply strategies, and de‑risk legacy liquid demand through convertible contracts.

Consolidation pressure: strategic asset consolidation by larger chemical players or private equity. Actions: prepare integration playbooks, use competition maps to identify bolt‑on targets, and secure conditional supply protections in customer contracts.

Procurement & commercial: move from annual spot buys to a laddered contracting mix—short‑term caps, medium‑term indexed offtake, and select capacity reservation agreements with contractual quality gates. Insist on supplier transparency on raw‑material sourcing and change‑control governance.

Operations & manufacturing: prioritize modular investments enabling rapid scale or pivot between electrolyte chemistries. Evaluate co‑location options with cell manufacturers to reduce logistics friction and support fast qualification cycles.

R&D & technology strategy: maintain a balanced portfolio: continue near‑term optimization of liquid and gel chemistries while accelerating selective partnerships on next‑generation solid platforms. Protect IP through joint development agreements with clear commercialization milestones.

M&A and partnerships: use the concentration map to identify strategic suppliers for minority investments, JVs, or exclusivity arrangements. Prioritize targets that offer proprietary additives, purification technologies, or advantaged feedstock access.

Risk management: stress test P&Ls against double‑digit input price swings and build scenario triggers into supplier contracts. For critical salts and precursors, establish contingency panels of secondary suppliers and a staged inventory policy.

Policy and compliance: embed regulatory horizon scanning into site selection and commercial contracts. For auto OEMs and cell suppliers seeking program eligibility, document end‑to‑end provenance from salt through to cell qualification.

Executives face a compressed timeline: qualification decisions, capacity commitments, and contract negotiations that will determine 2027–2030 program economics are being formed in 2026. Our full report marries a transparent, auditable market model (2020–2025 historical + 2026–2032 forecast) with executable toolkits—contract templates, supplier due‑diligence checklists, and an editable raw‑material impact model—so that strategy teams can convert insight into executable plans within governance windows.

The report does not merely estimate where demand will be; it diagnoses how supply structure, policy, and technology choices interact to produce winners and losers in the next procurement cycle. It also flags execution risk with prioritized mitigation levers—critical for CFOs and corporate development teams assessing capital allocation in a market where execution and qualification are as important as scale.

This release is a strategic preview. For teams preparing capital plans, negotiating supply, or evaluating M&A and JV opportunities in 2026, the full PW Consulting report provides the models, playbooks and competitive dossiers necessary to act with conviction. Access the complete report and our downloadable decision toolkits on our website to unlock the detailed segmentation, supplier scorecards, and editable scenario models referenced in this preview.

For detailed analysis of this topic, please visit the official page:Lithium Ion Battery Electrolyte Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com