How to Insulate a Metal Roof?

Home |

2026-03-13 06:07:52

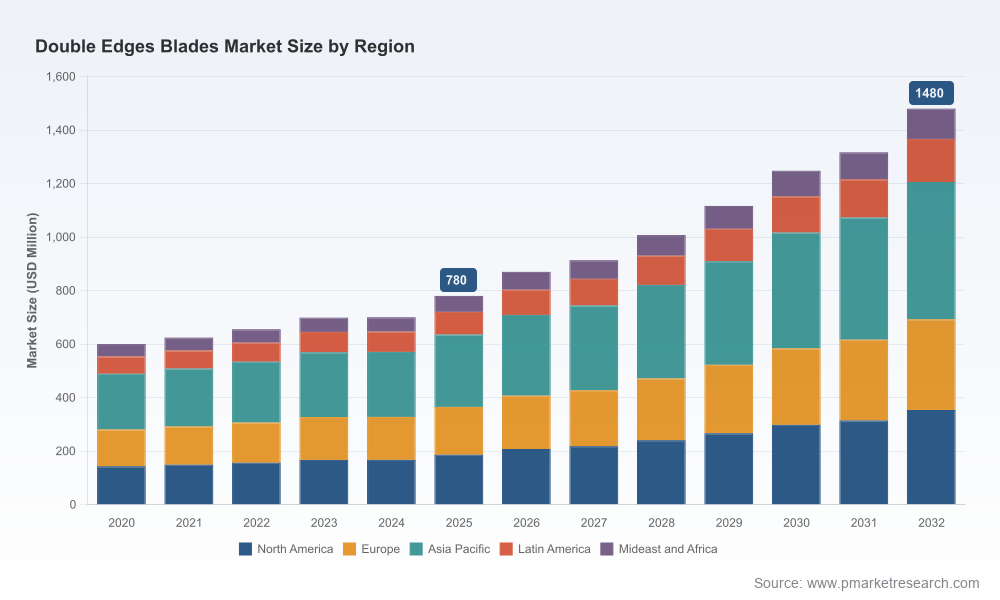

PW Consulting today publishes an executive summary of our new Double Edges Blades Market research — a data-driven, operationally practical study built to inform board-level and commercial decisions in 2026. Anchored on a 2025 base year and projecting through 2032, the report synthesizes historical performance (2020–2025), forward-looking scenarios and executable playbooks for manufacturers, retailers, private-label buyers and investors. At the macro level, the market has expanded from roughly USD 600 million in 2020 to USD 780 million in 2025, and our base forecast projects a continued compound annual growth rate of 9.0% through the forecast period. By 2032 the market is expected to approach the USD 1.48 billion mark, reflecting a combination of premiumization, channel evolution and regulatory-driven packaging changes.

Double Edges Blades Market

Our base-case projection shows the market scaling notably in the immediate post-2025 period — indexing from a 2025 base of USD 780 million, the market is modeled to pass approximately USD 870 million in 2026 and exceed USD 1.00 billion by 2028 under our central demand assumptions. These milestones are useful operational anchors: expected increases in unit demand and ASPs (driven by premium blades and upgraded packaging) create both margin opportunities and supply-chain stresses. For 2026 planning, firms should prioritize capacity flexibility, raw-material contracts with tiered volume options and accelerated compliance investments to capture premium channels without incurring recall or shelf-delisting risk.

Double Edges Blades Market

The Double Edges Blades market remains a mix of global incumbents, specialist premium players and a broad base of regional and OEM producers. The market concentration metrics (CR3 ~24.6%, CR5 ~26.2%) confirm a fragmented landscape, which shapes competitive strategy in three ways:

Double Edges Blades Market

Our competitive profiles dissect firms across capability vectors — metallurgical R&D, coating technologies, brand equity, retail distribution and regulatory compliance programs. We analyze leading names across these vectors and identify where strategic advantage is replicable versus where it is defensible only through investment or consolidation. For executive readers: the report’s company assessments include capability heatmaps and a near-term vulnerability index that triangulates product, channel and regulatory exposure.

Regulatory signals are central to the 2026 playbook. In the United States, razor blades’ classification under FDA’s Class I framework creates registration, labeling and traceability obligations that increase time-to-market friction for new entrants and generics. In the EEA, ISO 3558 safety testing and CE-marking remain prerequisite market-access steps. Simultaneously, the EU’s Packaging and Packaging Waste Regulation — with its mandated recyclability and reductions in plastic content by 2030 — materially changes packaging strategy. Our research shows that early movers who shift to steel-and-cardboard systems and who implement closed-loop packaging pilots gain both shelf differentiation and cost advantages over the medium term.

Stainless steel remains the dominant metallurgical choice for double-edge blades in most commercial assortments and continues to underpin product longevity and corrosion resistance claims. Third-party industry data (noting differences in market definitions) have also highlighted stainless steel’s strong position in the broader blades category; PW Consulting’s own market boundary and revenue definitions are carefully documented in the full report to reconcile variances between datasets. Importantly for procurement teams: stainless steel pricing trajectories, coating chemistry availability, and supplier lead times are the primary drivers of unit-cost variability through 2026–2028.

In keeping with our “trailer” approach, this release emphasizes strategic takeaways while withholding the report’s granular tables, region-by-region and application-level revenue breakdowns, full competitor financials and the proprietary valuation bands that underlie our M&A recommendations. Those granular datasets and model files are available through the full PW Consulting report package and are essential for transaction diligence, SKU-level assortment planning and board-level scenario modeling.

Boards, commercial leaders and procurement executives preparing budgets and capex plans for 2026 should treat this research as a decision-enabler: our macro forecast and practical playbooks convert top-line growth and regulatory shifts into immediate operational priorities. To access the full dataset, detailed company profiles, proprietary segment tables and downloadable scenario models, please visit the PW Consulting report page (full report access is gated for subscribers and clients).

PW Consulting’s Double Edges Blades Market study is designed to be a tactical manual for execution as much as a strategic forecast — delivering the insight and tools necessary to navigate a market that is growing, evolving and being reshaped by regulation and packaging innovation. For those looking to convert industry intelligence into competitive advantage in 2026, this report is the starting blueprint.

For detailed analysis of this topic, please visit the official page:Double Edges Blades Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com