ผู้นำนวัตกรรมความบันเทิงยุคดิจิทัลสู่ศูนย์รวมเกมออนไลน์มาตรฐานสากล

Games |

2026-05-16 13:58:54

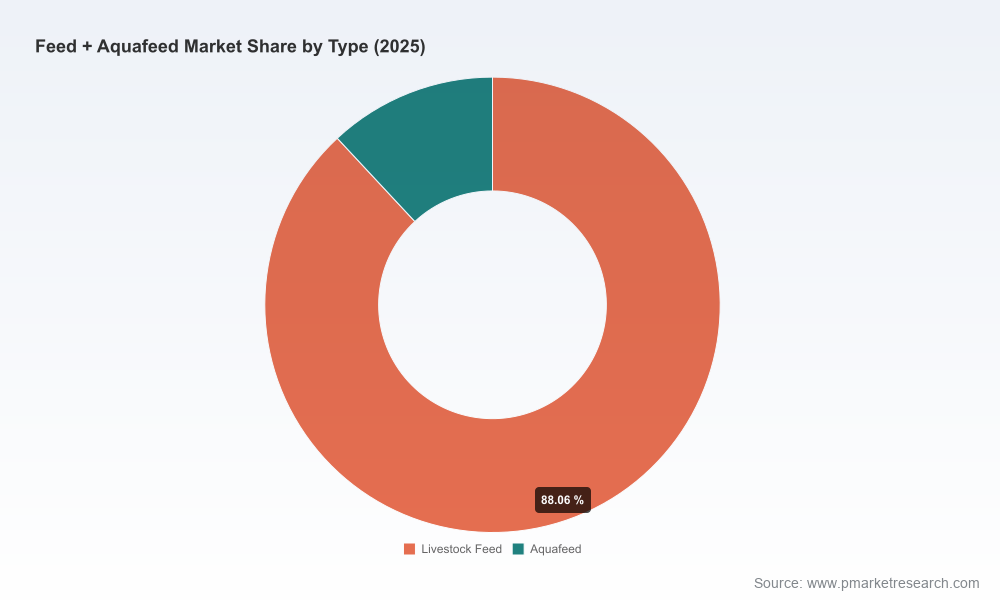

PW Consulting’s new Feed + Aquafeed Market report (base year 2025; forecast 2026–2032) crystallizes the strategic choices facing producers, ingredient suppliers, investors and policy-makers as the sector enters a new phase of growth and consolidation. The market has expanded steadily from the early 2020s and reached an inflection point in 2025. Our modelling shows the market accelerating through the forecast window at a compound annual growth rate (CAGR) of approximately 6.0%, progressing from the USD 500 million reference in 2025 toward an anticipated market scale in the low seven hundreds by 2032. For decision-makers planning calendars, capital allocations and product roadmaps in 2026, this report converts headline growth into actionable priorities, de-risked scenarios and execution-ready playbooks.

Feed + Aquafeed Market

Certification and sustainability are moving from differentiator to table stakes. Major feed producers are rapidly upgrading certification footprints and supply chains; buyers will increasingly require proof of chain-of-custody and environmental performance as a prerequisite for offtake and premium pricing.

Feed + Aquafeed Market

Raw-material innovation is changing margins. New co-products and protein concentrates that have undergone recent trials are beginning to appear in commercial formulations, creating opportunities to lower feed cost-per-unit-of-production while preserving animal performance.

Feed + Aquafeed Market

Market structure is consolidating but remains contestable. The top-tier players hold meaningful share but not absolute dominance; niches for species-specific, high-value feeds and localized service-oriented providers remain attractive.

The report combines a granular historical series (2020–2025) with a robust scenario framework for 2026–2032. We translate headline CAGR and market-scale projections into decision-grade inputs: portfolio IRR drivers, inventory-turn thresholds for feed mills, procurement hedging bands and willing-to-pay curves for sustainability-labelled products. Importantly, the modelling layers in sensitivity to commodity price shocks, regulatory tightening and variable adoption rates of alternative proteins—so your 2026 strategy can be stress-tested against plausible downside and upside paths.

Executive dashboards that map growth corridors to strategic options—M&A, JV, organic expansion, specialty product launches.

Supplier scorecards and manufacturing footprints with decision triggers for capacity investment or rationalization (includes facility-level KPIs and a resilience index).

Feed formulation playbooks: profitability-by-formulation matrices, raw-material substitution scenarios, and proof points from recent co-product trials and protein-concentrate pilots.

Regulatory readiness checklists and certification timelines—designed to shorten time-to-market for ASC/other certification-driven product lines.

M&A and partnership playbooks: target prioritization frameworks, valuation multiplexers for strategic vs. financial buyers, and integration risk heatmaps.

Commercial go-to-market templates for premium species and regional channels, including farmer-outreach protocols, offtake contract structures and pricing-performance guarantees.

Primary research and validation: interviews with leading feed producers, ingredient suppliers, large-scale aquafarmers and certification bodies to ground assumptions in on-the-ground reality.

The report profiles the strategic positioning and capability sets of global leaders and fast-followers, assessing them across production capacity, species coverage, sustainability credentials, R&D intensity and commercial reach.

Cargill, Incorporated — A global ingredient and feed powerhouse with a diversified production footprint. Cargill’s scale provides bargaining power on raw-material sourcing and the ability to commercialize new formulations rapidly. For clients this means Cargill is most likely to compete on integrated supply solutions and multi-market contracts.

Skretting — A market-leading specialist in aquaculture feeds with deep species expertise and a recent track-record of certification expansion. Skretting’s upgraded strategic agreements with large producers underscore its playbook: deepen producer partnerships to co-develop sustainable, lower-risk value chains.

BioMar Group — Focused on value-added, species-specific feeds; recent product launches for disease resilience in seabass demonstrate an emphasis on functional feeds that reduce downstream mortality and antibiotic reliance. BioMar’s approach highlights an attractive premium niche for players that can prove performance uplift.

Alltech — A provider of nutrition solutions and additives that can lift feed-conversion efficiency and animal health. Alltech’s value proposition is centered on margin improvement through biological performance rather than commodity displacement.

Aller Aqua Group — A manufacturer that combines feed programmes with hands-on technical support, catering to producers needing end-to-end feeding systems. The model underscores the commercial value of service-led differentiation.

Thai Union Feedmill — Expanding its footprint through strategic MOUs and regional partnerships, with an explicit focus on shrimp and fish feeds. This directional push illustrates how regional scale-ups are a key vector for market share gain.

Purina Animal Nutrition — Leverages brand and formulation expertise to serve recreational and commercial pond markets, underscoring an adjacent pathway for growth through diversified channel strategies.

Ridley Corporation — Demonstrates how localized extrusion capabilities and growth-enhancer products can secure leadership in specialty prawn and regional aquaculture segments.

New functional feed solutions launched by specialist producers point to accelerating product innovation aimed at reducing mortality and improving robustness—important for producers seeking to protect unit economics against disease shocks.

Strategic partnerships and MOUs across Asia signal that regional expansion and co-investment in local value chains will be an important route to secure supply and demand, particularly for shrimp and high-value species.

Certification milestones achieved by several global players are tightening the competitive field: buyers and brands increasingly expect certified inputs, elevating certification timelines to a strategic priority in 2026.

Ingredient innovators are bringing high-protein co-products and concentrated corn-protein solutions into trials. These inputs have been shown to integrate into commercial rations without compromising growth in trials, offering an alternative to traditional feedstocks and a lever to manage cost pressure.

Prioritize certification and traceability investments now. The cost of late certification is not just fees—it is forgone access to premium channels and longer sales cycles.

Deploy a two-track procurement strategy: secure long-term contracts for core commodities while piloting alternative proteins and co-products to reduce margin volatility.

Pursue bolt-on acquisitions and JVs that add species-specific know-how or local market access rather than broad-capacity buys; the market structure favors focused capabilities that command price premiums.

Invest in formulation R&D and field validation with commercial partners. Demonstrable improvements in FCR, survival and resilience translate directly into commercial premiums and contract leverage.

Adopt a data-first commercial model—feed-as-a-service propositions, performance guarantees and digital traceability can lock customers in and support margin recovery even as ingredient costs fluctuate.

CEOs, Heads of Strategy, Procurement Leads, Product and R&D executives, and investors should use the report as the single reference for aligning capital allocation with operational change. It converts macro growth trends, competitive moves and regulatory inflection points into tactical initiatives (capex prioritization, target lists for M&A, pilot programs for alternative proteins, and time-bound certification roadmaps). For private-equity and corporate development teams, our valuation-adjusted target scorecards and integration risk matrices provide a fast route to shortlist opportunities and structure offers.

PW Consulting’s Feed + Aquafeed Market report blends market-scale forecasting, competitor strategy, ingredient innovation analysis and ready-to-execute playbooks. The preview above highlights directional insights and strategic options; the full report contains the data tables, scenario outputs and supplier scorecards necessary to operationalize your 2026 plan. Visit PW Consulting to access the full report and to schedule a bespoke briefing where we will align our modelling to your portfolio and stress-test your strategic moves under multiple 2026 scenarios.

For detailed analysis of this topic, please visit the official page:Feed + Aquafeed Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com