Tension Hand Grip Market — 2026 Strategic Outlook: A PW Consulting Intelligence Brief

PW Consulting today issues its strategic intelligence brief drawn from the forthcoming Tension Hand Grip Market report (base year: 2025; historical coverage: 2020–2025; forecast: 2026–2032). This release is designed as a high-fidelity preview for executives who must translate market dynamics into investment, product, and go-to-market decisions for 2026. The analysis that follows conveys the report’s core implications and operational playbooks while preserving the report’s proprietary segment-level outputs — intentionally withheld to preserve the commercial value of the full study.

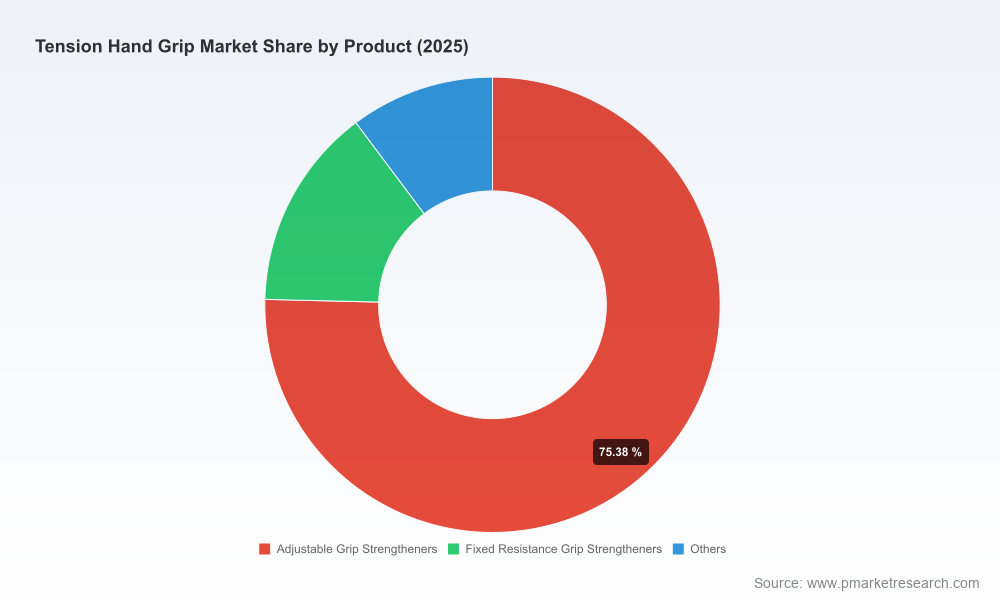

Tension Hand Grip Market

Executive snapshot

Our top-line view: the global tension hand grip market has demonstrated steady expansion through the first half of the decade, rising from approximately USD 163 million in 2020 to roughly USD 215 million in 2025. Under the central forecast, the market is expected to maintain healthy momentum across the 2026–2032 horizon, expanding at a compound annual growth rate of roughly 6.98% and moving toward an estimated market size in the mid-300 millions by 2032.

Tension Hand Grip Market

For corporate strategists, the message is clear: this is a growth market large enough to support differentiated product strategies and adjacent-service monetization, yet compact enough that well-timed strategic moves (innovation, channel optimization, selective consolidation) can materially change competitive positioning within a few quarters.

Tension Hand Grip Market

Why this report matters for 2026 decision-making

- Timing of investment: With sustained mid-single-digit CAGR through 2032, capital allocation decisions should prioritize scalable initiatives that can capitalize on steady demand rather than one-off volume plays.

- Product architecture and innovation cadence: Our research identifies durable demand for adjustable, high-durability designs and finger-isolation products. Companies that commit to iterative product roadmaps and rapid prototyping will capture outsized share of premium segments.

- Channel economics: E-commerce and direct-to-consumer models continue to reshape price discovery and branding. Tactical investments in owned digital channels and marketplace optimization yield faster payback than undifferentiated mass retail approaches.

- Service adjacencies: Rehabilitation clinics, competitive athletes, and remote coaching platforms are creating recurring revenue pathways (training programs, certified-device bundles) that turn a one-time device sale into multi-year customer relationships.

Competitive landscape: strategic positions and implications

The PW Consulting report includes a deep qualitative and tactical review of incumbent and challenger brands. Among the firms we analyzed are long-established specialist manufacturers, emerging high-intensity training brands, and niche ergonomic innovators. Each archetype embodies distinct competitive advantages and vulnerabilities:

- Heritage specialty manufacturers: Firms with long product lineage and heritage branding hold credibility with strength athletes and collectors. Their advantage lies in brand equity and product provenance, but they face pressures to modernize manufacturing and expand digital reach.

- Precision-engineering entrants: Companies that emphasize patented mechanical systems and all-metal constructions compete on durability and measurable resistance. These players can command premium pricing but must sustain R&D to avoid rapid imitation.

- Fitness-tech and high-intensity brands: Operators focused on CrossFit, functional fitness, and endurance training leverage community marketing and athlete endorsements. Their strengths are rapid trend-capture and high-velocity online sales; their risk is shorter product lifecycles and higher return rates.

- Dexterity and rehabilitation specialists: Producers of finger-specific trainers and clinical-grade devices can access institutional buyers and reimbursement channels, creating higher average order values and longer adoption cycles.

For each profile we evaluate go-to-market vectors, margin sensitivities, and the operational investments required to scale from niche to national penetration. The full report maps competitor roadmaps and provides playbooks for counter-positioning — while preserving the proprietary numeric breakdowns that underpin those recommendations.

Actionable strategic levers identified

- Modular product platforms: Develop a core mechanical chassis that supports accessory upgrades (e.g., advanced grips, digital sensors). This reduces SKU proliferation costs and generates a platform climb for existing customers.

- Data-enabled differentiation: Add simple, validated sensors and companion coaching content to convert a commodity device into a subscription-capable product with measurable outcomes.

- Channel orchestration: Combine direct-to-consumer channels with selective retail partnerships and institutional sales to optimize acquisition cost and margin mix. Prioritize regions and partners based on a staged market-entry playbook in the full report.

- Manufacturing and supplier resilience: Reshore or dual-source high-reliability components to reduce lead-time risk for premium SKUs and to protect margins against commodity swings.

- Community and athlete ecosystems: Activate athlete ambassadors, clinical champions, and digital coaching frameworks to build trust and increase attach rates for training programs and accessories.

- M&A and partnership criteria: Target small innovators and component specialists with defensible IP or channel relationships — not merely revenue multiples. The report provides a due-diligence checklist tailored to this market.

Operational playbooks included in the full report

The PW Consulting deliverable goes beyond high-level strategy. It contains operationally focused tools ready for immediate deployment, including:

- Scenario-modeled P&L and working capital templates keyed to conservative, base, and aggressive demand curves for 2026–2028;

- Market-entry checklists and 90/180/365-day rollouts for product launches across e-commerce, wholesale, and institutional channels;

- Supplier scorecards and cost-down roadmaps to reduce COGS without compromising perceived quality;

- Competitive response playbooks (price, feature, and channel moves) calibrated for different competitor archetypes;

- Customer cohort analyses and lifecycle playbooks to lift repeat purchase and attachment rates for consumables and accessories;

- Risk heatmaps and mitigation playbooks addressing quality events, inventory shocks, and regulatory exposures relevant to rehabilitation and clinical channels.

How to read the competitive field in 2026

Two critical structural observations emerge from our analysis. First, while a number of strong brands command customer trust, the market’s overall structure favors targeted specialization and premium differentiation rather than winner-takes-all consolidation. Second, digital distribution continues to compress time-to-customer and amplify brand narratives, meaning that even technically superior devices can struggle without a cohesive content and community strategy.

For decision-makers this implies a balanced approach: protect margin and brand in core premium offerings, while allocating a defined innovation budget to test lower-cost digital products and service bundles that can scale through online channels.

Practical next steps for 2026 planning

- Run a rapid portfolio audit focusing on modularization potential and product margin; set a six-month pilot for one modular SKU.

- Build a digital coaching MVP paired with a premium device to test subscription willingness-to-pay among core customer cohorts.

- Execute a supplier stress-test and prepare a dual-sourcing roadmap for critical mechanical components.

- Prioritize one institutional vertical (e.g., sports medicine clinics or professional teams) for deeper penetration, using a pilot partnership to create case studies and procurement templates.

- Establish an M&A watchlist informed by IP defensibility, channel access, and product fit — and allocate a small strategic war chest for bolt-on acquisitions.

Methodology and confidence

PW Consulting’s estimate and forecast framework synthesizes primary interviews, supply-chain price tracking, e-commerce channel scraping, retailer audits, patent landscaping, and client-validated demand modeling. We calibrate scenarios with sensitivity analyses across demand, price, and margin drivers to provide executives with realistic upside and downside pathways. The statistical confidence in the headline growth trajectory is high given consistent historical expansion and durable end-user demand drivers.

Accessing the full report

This briefing intentionally omits the report’s granular regional, product, and channel splits as well as the detailed company-level revenue estimates that form the basis for tactical scorecards. PW Consulting’s full Tension Hand Grip Market report contains those proprietary tables, the complete financial model, supplier shortlists, and executable marketing and M&A playbooks that 2026 planning cycles require. To obtain the full study, executive briefings, or tailored workshops, please visit PW Consulting’s reports portal or contact your PW Consulting representative.

PW Consulting remains available to brief leadership teams and investment committees on the implications of this market outlook and to co-develop go-to-market and M&A strategies that convert the projected market growth into sustainable competitive advantage.

For detailed analysis of this topic, please visit the official page:Tension Hand Grip Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com