PM2.5 Monitors Market — 2026 Strategic Outlook and Executive Briefing (PW Consulting)

Executive snapshot

PW Consulting today releases an authoritative executive briefing derived from its full PM2.5 Monitors Market research report (base year: 2025, forecast period: 2026–2032). The study synthesizes regulatory shifts, technology evolution, procurement cycles, and vendor dynamics into an actionable roadmap for executives planning capital allocations, product strategies, and go‑to‑market moves in 2026.

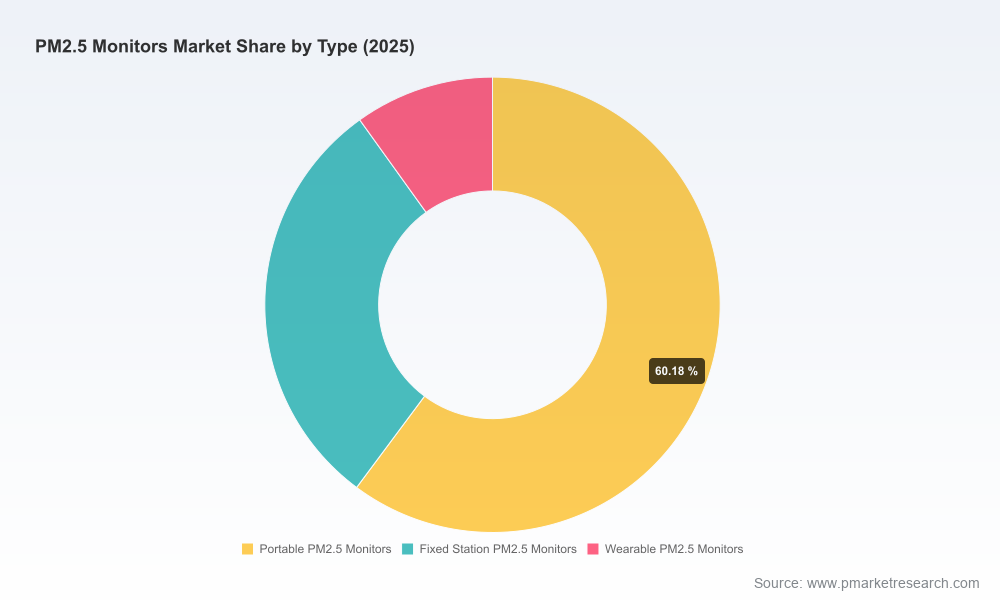

PM2.5 Monitors Market

Key macro takeaways: the global PM2.5 monitors market has grown from approximately USD 350 Million in 2020 to USD 500 Million in 2025, and is projected to expand to roughly USD 770 Million by 2032, reflecting a compound annual growth rate (CAGR) of 6.98% across the forecast period. These headline figures encapsulate demand driven by regulatory tightening, network modernization, and the convergence of sensor networks with cloud analytics and services.

PM2.5 Monitors Market

Why 2026 is a strategic inflection point

Several converging forces make 2026 a pivotal year for buyers, manufacturers, and investors in the PM2.5 monitoring ecosystem:

PM2.5 Monitors Market

- Regulatory acceleration: The tightening of primary air quality standards (e.g., a lowered annual PM2.5 standard) and the completion of formal designation cycles have compressed procurement timelines for environmental agencies and large private operators.

- Reference-method availability: Recent formal designations and certifications for several reference- and equivalent-method instruments have reshaped procurement criteria, increasing demand for FEM/FRM‑rated monitors where regulatory compliance is required.

- Network modernization: Many jurisdictions are transitioning from filter‑based manual sampling toward continuous analyzers and automated networks, creating simultaneous demand for instruments, integration services, and long‑term calibration support.

- Data quality scrutiny: High‑profile corrections and method comparisons in recent years have raised buyer expectations around traceability, bias correction, and documented performance under local conditions.

For decision‑makers this means procurement windows are both urgent and opportunistic: agencies and large corporates will balance the speed of network upgrades against the need for certified, defensible data. That trade‑off is central to 2026 strategic planning.

Competitive landscape — what matters to buyers and partners

The market exhibits moderate concentration: the top three vendors account for roughly a quarter of market value, while the top five approach just under a third. That structure creates a competitive climate in which regulatory acceptance and proven field performance carry outsized commercial value, even as innovative entrants and low‑cost sensor suppliers pursue volume and services plays.

From our vendor analysis, the following vendor archetypes are shaping the market:

- Established reference‑method vendors with regulatory pedigree: Firms producing beta‑attenuation and gravimetric samplers maintain strong footholds where national and state monitoring networks prioritize FEM/FRM‑class performance. Their strengths lie in certification history, service networks, and accepted method status.

- Real‑time continuous analyzer specialists: Vendors offering FEM‑designated continuous mass monitors (real‑time mass sensors with regulatory approvals) are driving replacement of legacy filter systems and enabling regulatory networks to meet tighter standard timelines.

- Portable and IoT‑oriented players: Manufacturers of portable, wearable, and low‑power fixed monitors are expanding uptake in citizen science, corporate health & safety, and indoor air quality segments. Their value proposition centers on cost, ease of deployment, and data platforms rather than regulatory equivalence.

- Systems and integration providers: Large industrial and instrumentation companies leverage cross‑portfolio strength (e.g., gas analyzers, environmental networks) to sell bundled solutions and long‑term service contracts.

Notable vendor developments that inform 2026 strategy include recent EPA designations and independent certifications that have altered procurement preferences and competitive advantage. Vendors holding formal designations or widely accepted FEM/FRM status enjoy preferential positioning in regulatory tenders; conversely, new certifications for emerging instruments create immediate consideration windows for agencies planning network refreshes.

What the full report contains — operational depth for decision-makers

The PW Consulting market study is built to be executable by procurement heads, product leaders, and corporate strategists. The full deliverable contains:

- Detailed market sizing and growth modelling (2020–2032) with scenario runs reflecting regulatory timelines and technology adoption curves.

- Buyer decision frameworks and procurement playbooks tailored for municipal networks, industrial operators, and corporate real‑estate portfolios.

- Technology roadmaps comparing reference‑grade, FEM/FRM‑equivalent, continuous analyzers, and low‑cost sensor ecosystems—quantifying tradeoffs in accuracy, TCO, and time‑to‑deployment.

- Regulatory heatmaps that map designation statuses, timeline risk, and likely procurement triggers across major jurisdictions.

- Competitive benchmarking and vendor shortlists for different buyer objectives (regulatory compliance vs. network density vs. occupational monitoring), including criteria for interoperability, service coverage, and certification evidence.

- Commercial templates: RFP wording, SLA clauses for calibration and data quality, CAPEX/OPEX modelling tools, and an M&A target screening framework for strategic acquirers.

- Case studies and field validation appendices that document real‑world bias correction, co‑location results, and maintenance regimes—essential for defensible network rollouts.

To honor the briefing role of this release we present these capabilities at a summary level; the granular vendor and regional splits, line‑item pricing, and model spreadsheets are available in the full report.

Strategic recommendations for 2026 decision-makers

Based on our analysis, leaders should prioritize the following actions this year:

- Align procurement windows with regulatory designation cycles: Map replacement or expansion projects against finalized standard designations to ensure purchased equipment meets the expected method requirements at the time of deployment.

- Diversify instrument portfolios by use‑case: Deploy certified FEM/FRM instruments where regulatory defensibility is required, while using lower‑cost, high‑density sensors for spatial coverage and early detection—paired with robust co‑location and bias correction programs.

- Invest in calibration and data governance as a product differentiator: Offerings that bundle hardware with long‑term calibration, certification support, and analytics subscriptions will win incremental share and create recurring revenue streams.

- Establish strategic supplier partnerships: For vendors, securing approvals and establishing long‑term service partnerships with government networks accelerates adoption; for buyers, multi‑vendor strategies reduce single‑supplier risk while preserving access to best‑in‑class technologies.

- Monitor method equivalency updates vigilantly: Recent formalizations and corrections in method performance underscore the need for continuous validation. Procurement specifications should include clauses for demonstrated field performance under local conditions.

- Evaluate M&A and investment opportunities in adjacent service providers: Entities offering field services, data analytics, and managed monitoring networks are logical targets to capture service margin as hardware commoditizes.

Implications for investors and buyers

Investors: The market’s steady CAGR and regulatory tailwinds create attractive opportunities in both hardware (certified instruments, continuous analyzers) and scaling services (calibration networks, analytics subscriptions). However, return profiles will diverge between reference‑grade equipment and commoditized sensor platforms—investors should favor companies with regulatory acceptance, strong service economics, or defensible data platforms.

Procurement officers and city planners: Plan for staggered investments—immediate priority for compliance‑critical sites where certified instruments are required, and phased rollouts for dense sensor coverage to improve exposure mapping and public health decision support. Ensure procurement language mandates field validation and clearly defined SLAs for data quality.

Risks and monitoring indicators

- Regulatory volatility: Changes to standard thresholds or designation processes can accelerate or delay purchases—maintain scenario models tied to public consultation timelines.

- Method performance revelations: Future method comparisons or data corrections can shift demand between vendors; continuous validation programs are essential risk mitigation.

- Supply chain and service network constraints: Lead times for certified analyzers and the availability of local calibration services materially affect deployment schedules.

- Market fragmentation pressures: While large vendors benefit from certification, specialized entrants and platform providers can win niche segments—monitor pricing compression in portable and IoT categories.

Conclusion — why this report matters for 2026 planning

The PW Consulting PM2.5 Monitors Market report translates regulatory momentum, vendor certification developments, and technology economics into a decision‑ready framework for 2026. With a clear growth trajectory from USD 500 Million in 2025 to an estimated USD 770 Million by 2032 (CAGR ~6.98%), stakeholders face both a narrowing compliance window and an expanding set of strategic choices. The competitive landscape rewards demonstrable, certifiable performance and integrated service offerings; at the same time, new sensor‑based models create opportunities for broader coverage and value‑added analytics.

For procurement leads, product strategists, and investors aiming to convert momentum into measurable outcomes in 2026, the full report provides the granular segmentation, vendor scoring, and executable playbooks required to act with confidence. Visit our report page to access the full dataset, vendor matrices, and the downloadable procurement toolset.

For detailed analysis of this topic, please visit the official page:PM2.5 Monitors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com