Schistosomiasis Market Technological Advancements and Forecast Analysis

Health |

2026-05-22 11:36:28

PW Consulting’s Mortar Market report (base year 2025) synthesizes five years of historical performance (2020–2025) and a seven‑year forecast (2026–2032) into a concise decisioning toolkit for corporate leaders, investors, and category managers. The global mortar market reached an estimated USD 3,380.0 Million in 2025 and, under a central‑case projection, is set to expand at a compound annual growth rate (CAGR) of 5.6% through 2032, moving towards roughly USD 4,845.4 Million by the end of the forecast window. This trajectory reflects an inflection driven by infrastructure programmes in growth markets, increased renovation activity in mature markets, and accelerating adoption of polymer‑modified and preblended systems.

Mortar Market

Actionable horizon: The 2026 planning cycle requires companies to balance near‑term margin pressure with medium‑term capacity investments. Our modelling translates macro drivers into investment triggers and ROI timelines calibrated to the 2026–2032 outlook.

Mortar Market

Scenario readiness: We provide quantified base, upside and downside scenarios that explicitly map how raw material shocks, regulatory tightening, and automation adoption alter return profiles across product types and channels.

Mortar Market

Commercial playbooks: The report identifies high‑probability commercial interventions (pricing cadence, product premiuming, channel segmentation) that leaders can deploy in H2 2026 to protect margins and capture share without waiting for full market recovery.

The mortar market’s recent trendline — from approximately USD 2,580.0 Million in 2020 to USD 3,380.0 Million in 2025 — illustrates a steady recovery and structural expansion beyond mere cyclical rebound. Key drivers sustaining the forecasted 5.6% CAGR include: continued urbanization and retrofit demand, greater use of factory‑produced and polymer‑modified mortars for consistency and speed, and infrastructure stimulus in several large markets. At the same time, the sector is being reshaped by input cost volatility and standardisation pressures that both constrain and create opportunities for differentiated, higher‑value formulations.

Product types: Traditional masonry mortars remain the backbone of volume demand, while tile adhesives and repair mortars are growing faster on a value basis owing to trending interior upgrades and renovation cycles.

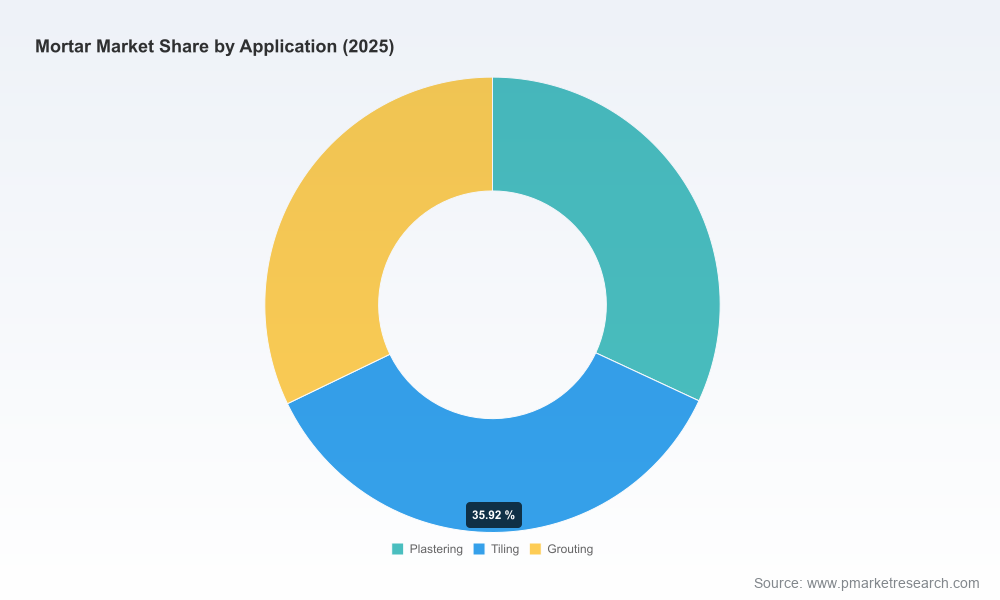

Applications: Plastering, tiling and grouting continue to define end‑use demand patterns; however, accelerated adoption of ready‑mix and silo solutions is supporting productivity gains on larger projects.

Regional dynamics: Market maturity, labour cost dynamics, and infrastructure policy drive divergent growth dynamics across geographies. The report maps where volume and value growth decouple and where premiumisation is feasible without compromising competitiveness.

The sector exhibits a measured concentration: the top three firms account for roughly one‑third of market revenue, while the top five account for under half. This structure creates a landscape in which scale matters for procurement and logistics, but regional specialists and product innovators retain outsized commercial influence.

Large integrators and chemical majors (examples: Sika, BASF, Henkel) are pushing product innovation and channel expansion. Sika’s recent moves — the acquisition of a Denmark‑based mortar manufacturer and the opening of a sustainable, automated facility in Singapore — exemplify a two‑track strategy of buy‑and‑build combined with greenfield capacity to capture premium margins in high‑growth corridors.

Established mortar brands and regional champions (examples include major U.S. preblended suppliers and traditional European building‑materials firms) remain critical to distribution networks and contractor relationships, leveraging branded formulations and service models such as silo systems and on‑site batching support.

Consolidation activity will likely continue in 2026 across select European and Asia‑Pacific markets where automation and sustainability credentials grant acquirers improved unit economics and faster route‑to‑market for higher‑value products.

Raw material volatility is one of the highest‑probability disruptors over the next 18–36 months. The cement market experienced a material spike in 2024 — with coal‑linked price moves forcing many manufacturers to reprice contracts and compress margins. Cement and sand price volatility, together with logistics cost inflation, are recurring themes in our downside scenarios.

Pricing strategies: Quarterly or index‑linked pricing mechanisms, selective pass‑through clauses, and differentiated pricing for premium polymer‑modified products are practical levers detailed in the report.

Sourcing and vertical options: We model the economics of strategic vertical integration (captive additives sourcing, co‑located silo systems) versus flexible procurement (index hedging, supplier consortiums) to show breakeven points for CAPEX decisions.

Standards such as ASTM and CEN test methods remain central to buyer specification and public procurement. ASTM C270 and related specifications set performance expectations for water retention, air content and compressive strength in masonry mortars. EN testing protocols continue to govern flexural and compressive performance for molded specimens. For companies operating across multiple regulatory regimes, early alignment with evolving standards reduces go‑to‑market friction and creates premiumisation opportunities.

A calibrated market model (2020–2032) with downloadable time series for revenue, growth rates, and scenario outputs to feed company-level planning models.

Three scenario sets (base, upside, downside) that quantify revenue, margin, and cash‑flow implications for common commercial actions (price, mix, channel) and CAPEX choices.

Go‑to‑market playbooks tailored to: (a) multinational chemical manufacturers seeking scale, (b) regional producers aiming for premiumisation, and (c) distributors looking to digitize ordering and delivery.

Supplier and raw‑material stress tests that link input price shocks to contract clauses, inventory strategies, and hedging alternatives.

A competitive heatmap and M&A tracker that highlights likely targets, strategic fit criteria, and integration risk factors (lab, logistics, channel overlap).

Regulatory matrix and compliance checklist that translates ASTM/CEN obligations into product development and documentation requirements.

Prioritise quick wins: Implement index‑linked pricing for commodity lines and concentrate promotional investments on higher‑margin polymer‑modified products where buyers accept premium pricing.

Right‑size capacity investments: Use our scenario outputs to stage CAPEX — commit to modular expansions with automation triggers tied to sustained demand thresholds rather than single‑point forecasts.

Operationalise sustainability: Greenfield or retrofitting investments in lower‑carbon mortar production should be matched with channel incentives and co‑marketing to secure payback in premium channels.

Prepare M&A playbooks: For acquirers, prioritise targets that offer immediate cost synergies in procurement or unique distribution access; for targets, ensure integration playbooks focus on lab harmonisation and regulatory alignment.

Monitoring the strategic moves of major players provides early warning of shifting competition dynamics. Recent high‑impact developments include a strategic acquisition by a large polymer‑specialist that expands automated capacity in the Nordics, and the inauguration of a sustainable mortar facility in Southeast Asia to capture Asia‑Pacific infrastructure demand. At the same time, leading regional producers continue to invest in customer engagement and event sponsorships to defend brand position in mature markets. These signals underline the dual trajectory of consolidation plus premiumisation across the value chain.

In keeping with our “trailer” approach, this press release surfaces the strategic takeaways, high‑level sizing and primary competitive dynamics, while withholding detailed segment tables, regional shares and channel economics that are proprietary to the report. These granular datasets and downloadable models are included in the full Mortar Market report to ensure clients have a defensible basis for pricing, capex and M&A decisions.

Download the full report to access: the detailed market model (including time‑series downloads), sensitivity analyses, and supplier scorecards needed for board‑level investment decisions.

Book a strategy workshop with PW Consulting to align the report’s scenarios to your P&L and to develop a 90–180 day action plan focused on margin protection and selective growth capture.

Subscribe to our quarterly Mortar Market tracker to receive alerts on raw material shocks, regulatory updates, and M&A activity that could alter your strategic assumptions.

For 2026 planning cycles, the mortar sector presents a classic combination of predictable, structural growth and elevated tactical risk from input volatility and regulatory pressures. PW Consulting’s Mortar Market report equips leaders with the scenario‑based foresight, commercial playbooks, and operational checklists necessary to protect margins, prioritise targeted investments, and seize higher‑value growth pockets. For the full dataset, segment breakdowns, and executable models, access the complete report and engage our team for a tailored implementation session.

For detailed analysis of this topic, please visit the official page:Mortar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com