Polyimide Tape (Kapton) Market 2026: Strategic Playbook for Resilient Growth

Executive summary

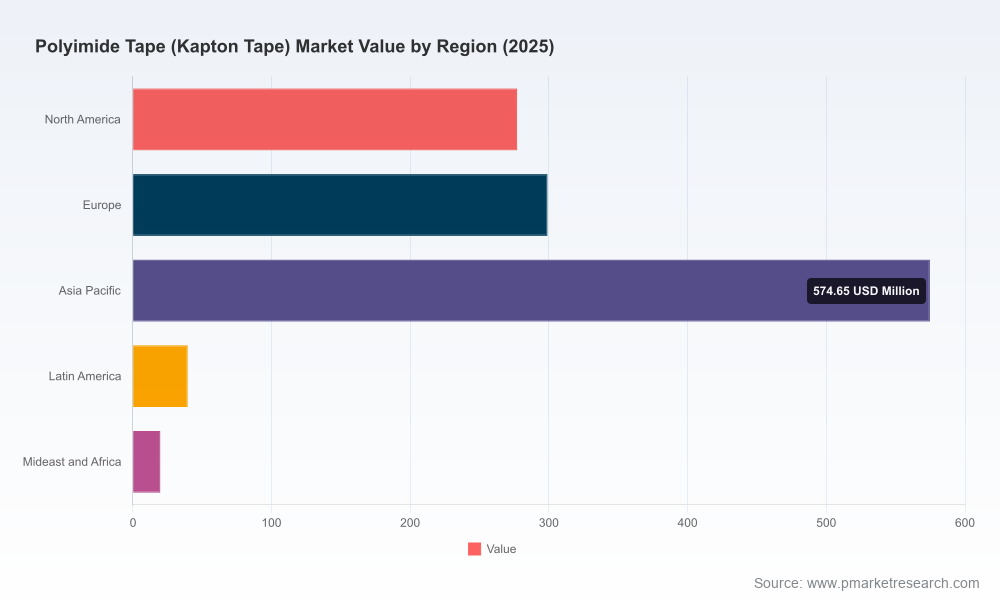

PW Consulting’s latest market research on Polyimide Tape (Kapton Tape) positions the material as a strategic component in high-growth industrial ecosystems. From a market that expanded from under USD 800 million in 2020 to roughly USD 1.21 billion in 2025, our modelling shows a continuation of robust expansion: the market is projected to exceed USD 2.23 billion by 2032, implying a compound annual growth rate of 9.2% across the 2026–2032 forecast horizon. This trajectory is being driven by cross-sector demand in semiconductors, electric vehicles (power electronics), aerospace and defence, and advanced manufacturing.

Polyimide Tape (Kapton Tape) Market

Why this research matters for 2026 decision-makers

In an era of accelerating technology cycles and tighter trade controls, polyimide tape is no longer a commodity item for procurement teams — it is a strategic input whose availability, specification and compliance profile can materially affect product development cadence, manufacturing yields and final product performance. Our report translates market-level growth into practical levers: where to prioritise near-term supplier qualification, how to stress-test your supply chain under export-control scenarios, and what product innovations will protect margin and reduce downstream risk.

Polyimide Tape (Kapton Tape) Market

What PW Consulting’s report delivers (practical, transaction-ready content)

- Actionable demand scenarios: forward-looking models built on primary interviews and supply-side constraints that quantify inventory, lead-time and price sensitivity under different demand shocks.

- Supplier benchmarking and procurement playbooks: templates and scorecards for qualifying producers across performance, financial strength, regulatory coverage and capacity flexibility.

- Regulatory and trade-control matrix: a concise, country-level map of export-control developments and implications for sourcing, cross-border manufacturing and contract clauses.

- Product roadmaps and application briefs: technical filters and decision trees for selecting tape type and adhesive systems for critical use-cases (e.g., semiconductor masking, high-voltage insulation and thermal shielding in EV inverters).

- M&A and partnership checklist: valuation drivers, integration risks and deal structures tailored to acquiring capacity, technology or market access in a moderately concentrated supplier base.

- Capex and capacity planning tools: build-versus-buy calculators tuned to lead times, capex intensity and ramp profiles specific to polyimide film and tape manufacturing.

Market structure and competitive positioning (what executives need to know)

The polyimide tape market exhibits moderate concentration: three leading suppliers account for a meaningful portion of the market, while the top five capture roughly two-thirds of global supply. This structure creates strategic opportunities as well as supply-risk vectors. Key global players include established chemical and adhesive giants and specialised tape manufacturers; their footprints span proprietary film production, adhesive formulation and system-level assembly support.

Polyimide Tape (Kapton Tape) Market

- DuPont (Wilmington, Delaware) remains a pivotal industry player with branded polyimide film and tape offerings and recent capacity investments aimed at satisfying rising global demand.

- 3M Company (St. Paul, Minnesota) continues to compete on application-specific tape systems and has recently introduced high-performance variants for extreme-temperature semiconductor processes.

- Nitto Denko (Osaka) has increased production capacity in the Asia-Pacific region focused on EV power-electronics and EMI shielding applications.

- Regional and niche suppliers — from multinational materials firms to specialised distributors — complement the market with custom solutions and aftermarket services that are critical for demanding end-uses.

Understanding these firms’ strategic postures — from capacity expansions to new product launches — is essential for buyers and investors planning 2026 deployments. Our report synthesises corporate activity into a “move-by-move” matrix that links supplier initiatives to potential pricing, availability and qualification outcomes for customers.

Supply-side constraints and regulatory tailwinds

Two supply-side realities deserve operational focus in 2026 planning:

- Raw material cost and technical concentration: polyimide resin monomers remain cost-intensive and are manufactured in limited global facilities. This creates price volatility and long qualification lead times for alternative chemistries.

- Export control and trade policy dynamics: since mid‑2025, multiple jurisdictions have updated export controls and end-use restrictions affecting aromatic polyimides, advanced polymer films and inputs relevant to semiconductor and battery supply chains. These developments complicate cross-border sourcing, increase compliance obligations, and can alter supplier viability for certain end-uses.

Collectively these factors change the calculus for inventory strategies, dual‑sourcing, and supplier localisation. PW Consulting’s regulatory matrix distils the legal changes and prescribes mitigations such as pre-export licenses, controlled‑substance audits and contractual warranties tailored to 2026 procurement cycles.

Near-term signals and recent competitive moves

- Capacity expansion remains the dominant industry response to demand: notable is a major firm’s completed expansion in Ohio to boost polyimide film output, signalling confidence in long-term adoption across electronics and aerospace value chains.

- Specialist production increases in Asia-Pacific target power-electronics and EMI shielding for electric vehicles, reflecting OEMs’ prioritisation of thermal and electrical management at the inverter and battery-level.

- Product innovation continues at pace: new tape variants designed for extreme-temperature masking in semiconductor fabrication indicate suppliers are competing on performance-driven differentiation rather than price alone.

These signals shape where buyers should focus qualification resources: high-performance product lines and regionally proximate capacity are likely to be premium procurement priorities through 2026.

Strategic implications and recommended plays for 2026

For executive teams preparing capital budgets and procurement strategies in 2026, our research points to five priority plays.

- Embed supply-control clauses into long-term contracts. Seek capacity reservations and step-up clauses with key suppliers to hedge against production shocks and export-control disruptions.

- Dual‑source across tiers and geography. Combine investments in qualified tier‑1 suppliers with local distributors that can provide rapid fulfilment and small-batch testing services.

- Invest in upstream optionality. Where product architecture allows, qualify alternative polymer chemistries and adhesive systems to reduce dependence on single monomer streams.

- Pursue targeted M&A or JV activity. For OEMs and component suppliers requiring guaranteed supply, acquiring or partnering with film-capable producers can be faster and more reliable than relying on spot markets.

- Operationalise regulatory intelligence. Make export-control screening a front-line procurement KPI; include regulatory impact scenarios in your 18‑month supply‑planning cycle.

How the report supports commercial execution

PW Consulting designed the report as a hands-on toolkit for teams executing in 2026. Clients receive not only market curves and scenario models but also ready-to-use artifacts: supplier scorecards, contract clause libraries adapted to export constraints, capex payback models, and a decision tree for product selection by end-use. The content is organised to support fast-turn due diligence for procurement, business development and corporate strategy teams.

What we deliberately leave to the full report

Consistent with the “trailer” approach, this release surfaces the strategic signals and practical recommendations executives need to prioritise for 2026. To preserve the actionable competitive intelligence that underpins procurement and M&A playbooks, we have withheld granular segment-level tables, regional share breakdowns and proprietary supplier scoring metrics. These are available in the full report, which includes detailed appendices, primary-interview transcripts and calibrated financial models.

Next steps

For teams preparing 2026 budgets and supplier strategies, PW Consulting recommends a three-step immediate plan:

- Conduct a 60‑day supplier and regulatory risk review using the report’s checklist to identify single‑point failures and export‑control exposures.

- Prioritise qualification projects for high‑risk tape types and adhesive systems mapped to your most critical product lines.

- Engage with potential partners or acquisition targets found in our competitive landscape matrix to secure optionality ahead of 2027 demand inflection points.

To access the complete market intelligence pack — including the full data appendix, supplier scorecards, and scenario models — please refer to PW Consulting’s official report release. The full report is structured to support board-level briefings, procurement RFPs and M&A diligences that will shape resilient, cost-efficient decisions in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Polyimide Tape (Kapton Tape) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com