Paper Recovery Solutions Market to Reach $196.27 Billion by 2035

Other |

2026-06-18 10:03:29

PW Consulting today releases a focused intelligence brief designed to equip C-suite leaders and commercial teams with the strategic priorities they must act on in 2026. Our Winter Loungewear Market report (base year 2025; forecast period 2026–2032) synthesizes five years of historical performance with forward-looking scenario modeling to deliver a clear growth view: the global winter loungewear market grew from approximately USD 13,850 Million in 2020 to USD 18,500 Million in 2025, and — assuming the central forecasting case — is projected to reach roughly USD 28,280 Million by 2032, reflecting a 6.25% CAGR across the forecast window.

Winter Loungewear Market

Demand resilience, margin opportunity: The winter loungewear category has shown steady, above-inflation growth driven by a structural shift toward home comfort and seasonally influenced gifting cycles. That creates room for margin improvement if companies align assortment, pricing, and channel strategy to capture higher-value consumer segments.

Winter Loungewear Market

Fragmented competitive landscape: The category remains materially fragmented (low CR3/CR5 concentration), which means scale helps but does not guarantee category leadership. Smart specialization — in materials, channel, or community — yields outsized returns versus simply expanding SKU counts.

Winter Loungewear Market

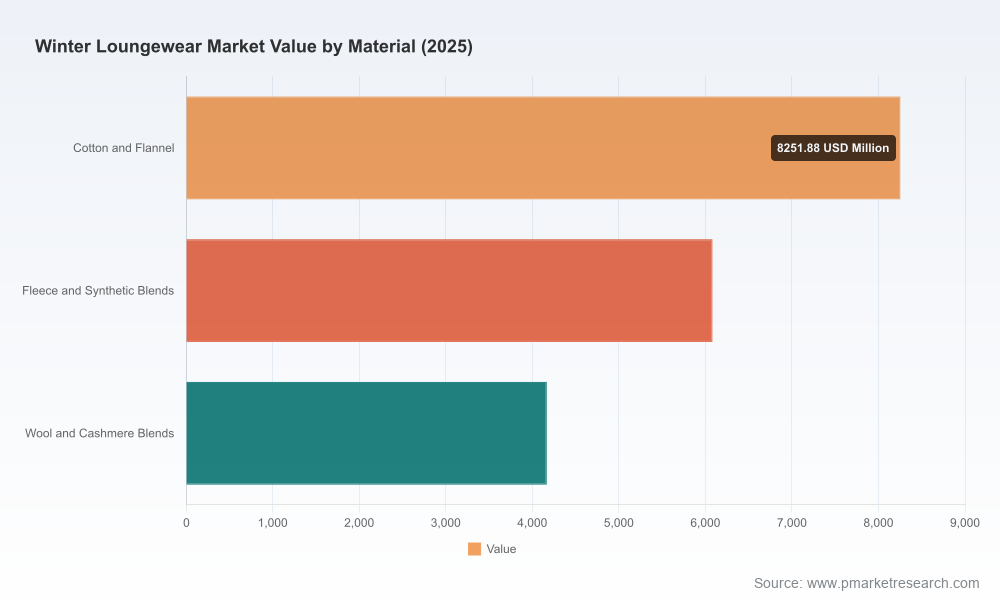

Materials and sustainability are strategic levers: Polyester-based fleeces remain foundational to winter comfort offerings, even as recycled fibers and cotton blends gain prominence among eco-conscious buyers. Managing material sourcing and communication of sustainability credentials will be a competitive differentiator in 2026.

Our report is intentionally operational. Beyond headline market sizing and a forward-looking forecast, subscribers receive a suite of plug-and-play tools and playbooks to execute in 2026:

Demand forecasting model (Excel): scenario-ready forecasting with adjustable assumptions for price elasticity, seasonality, and channel mix to stress-test revenue and inventory outcomes under competing consumer and macro trajectories.

Go-to-market playbooks: 90-day, 6-month, and 18-month tactical roadmaps for (a) DTC acceleration, (b) wholesale/retail partnerships optimization, and (c) rapid holiday-season SKU rationalization and promotional planning.

Product innovation agenda: a prioritized list of material and construction investments (thermal layering blends, recycled fleece, hybrid performance-lounge fabrics) and an ROI template for sampling, testing, and scaling.

Pricing and margin optimization toolkit: a micro-segmentation approach to price points, bundling, and promotional cadence aimed at protecting ASP while improving sell-through in seasonal windows.

Supply chain risk matrix: supplier concentration heatmaps, lead-time sensitivities, and mitigation playbooks to manage raw-material volatility and geographic sourcing risk — critical given polyester and cotton market dynamics.

Consumer persona & creative brief bank: data-backed profiles and messaging blueprints optimized for social, DTC conversion pages, and wholesale merchandising.

The winter loungewear category hosts a mix of legacy mass brands, fast-fashion giants, premium DTC players, and niche sleepwear specialists. PW Consulting’s report analyzes key players and recent moves to highlight pathways for incumbents and challengers alike.

Hanesbrands Inc. (Winston-Salem, USA): Strength lies in scale, breadth of everyday comfort styles, and value-focused thermal offerings. Tactical advantage: operational efficiency and broad retail penetration. Strategic opportunity: prioritize premiumization pockets and expand sustainable fabric mixes without eroding core price-value perception.

Gap Inc. / Old Navy (San Francisco, USA): Proven at translating trends into mass-market hits (recent Bounce Fleece collections illustrate this). Tactical advantage: supply chain scale and promotional muscle. Strategic opportunity: refine channel segmentation—elevate digital exclusives to protect margin while using in-store to drive discovery.

SKIMS (Los Angeles, USA): Premium DTC with powerful brand equity and event-driven merchandising (Team USA Winter Olympics collection, seasonal holiday shops). Tactical advantage: high ASP and strong social-driven demand. Strategic opportunity: convert limited-edition halo drops into staple repeatable revenue streams via tiered product ladders and targeted wholesale relationships.

H&M (Stockholm, Sweden): Scale, speed-to-market, and accessibility. Tactical advantage: market penetration at aggressive price points. Strategic opportunity: invest in circularity programs and verified recycled-fiber sourcing to mitigate reputational risk and support premium limited collections.

Eberjey (Miami, USA): Niche luxury sleep-and-lounge brand focused on softness and design. Tactical advantage: high customer loyalty and premium positioning. Strategic opportunity: scale via partnerships in select wholesale channels and expand core basics to capture higher-frequency purchases.

Aritzia (Vancouver, Canada): Curated premium everyday and loungewear with strong product storytelling and higher ASPs. Tactical advantage: brand curation and retail experience. Strategic opportunity: translate in-store experience into higher-margin digital subscriptions and loyalty-driven pre-season drops.

Athleta (Gap Inc.): Performance-lounge hybrids that bridge warmth and technical comfort. Tactical advantage: category crossover appeal for wellness-minded consumers. Strategic opportunity: deepen cross-category bundles (activewear + loungewear) to increase basket sizes during holiday seasons.

PVH Corp. (Calvin Klein, New York, USA): Heritage premium positioning with strong licensing and global wholesale reach. Tactical advantage: brand recognition and premium essentials. Strategic opportunity: exploit brand partnerships and limited-edition collaboratives to drive traffic and margin during winter peaks.

Several visible product launches and seasonal collections provide clues about where leading players are placing their bets. High-profile initiatives such as SKIMS’ Team USA winter collection and Old Navy’s Bounce Fleece rollouts indicate a continued strategy of combining lifestyle storytelling with technical comfort. These moves confirm two converging themes:

Event-driven partnerships (Olympics, holidays) accelerate brand discovery and justify premium pricing for limited assortments.

Broad-market players continue to use fleece and hybrid constructions to balance cost and perceived value — but the margin upside increasingly comes from premium sub-lines and sustainable-sourcing premiums.

Two raw-material facts are especially relevant for 2026 planning: polyester-based fibers remain the dominant input for fleece constructions globally, and cotton remains a strategic but volatile input. Concurrently, recycled polyester and recycled fleece blends are moving from “nice-to-have” to “expectation” among sustainability-minded consumers. Our supply chain scenarios model the impact of polyester price shifts and cotton availability on lead times and margin, providing prioritized mitigation steps (dual-sourcing, forward contracts, and modular assortment planning).

90-day: Defensive margin protection — Freeze low-performing SKUs, negotiate short-term supplier hedges for key fiber inputs, and reallocate marketing dollars to high-ROI digital channels targeted by persona.

6-month: Revenue acceleration — Launch a premium-limited line tied to a cultural moment (sporting event or holiday), implement dynamic pricing for gift season, and pilot DTC-only bundles to capture higher ASPs with controlled inventory.

18-month: Structural differentiation — Invest in circular product lines with verified recycled content, establish regional sourcing hubs to cut lead times, and build a subscription/renewal program for repeat customers to smooth seasonality.

Key risks include raw-material price shocks, a warmer-than-expected winter season compressing demand, and potential regulatory shifts tied to sustainability claims. PW Consulting’s full report models these downside scenarios with granular regional and channel sensitivity analysis, but to preserve the high strategic value of our primary dataset we intentionally withhold granular region-by-region and channel-by-channel percentage splits in this public summary. Subscribers receive the full segmentation tables, regional demand curves, and retailer-level channel economics in the downloadable report package.

If your 2026 planning cycle includes assortment resets, capital allocation to e-commerce, or supply-chain reconfiguration, PW Consulting’s Winter Loungewear Market report provides both the macro forecast and the tactical toolset to operationalize strategy. Our advisory teams are available to run bespoke demand-scenario workshops, customize the forecast model to your internal KPIs, and co-develop implementation roadmaps for pricing, sourcing, and channel execution.

To preserve the integrity of the dataset while offering a decisive call to action: download the full report to access the complete regional and channel splits, competitor scorecards, the Excel forecasting model, and the proprietary go-to-market playbooks that are essential for high-confidence decision-making in 2026.

For detailed analysis of this topic, please visit the official page:Winter Loungewear Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com