Gestational Trophoblastic Disease Market 2026: Strategic Imperatives from PW Consulting

Executive preview — what every executive should know before setting 2026 priorities

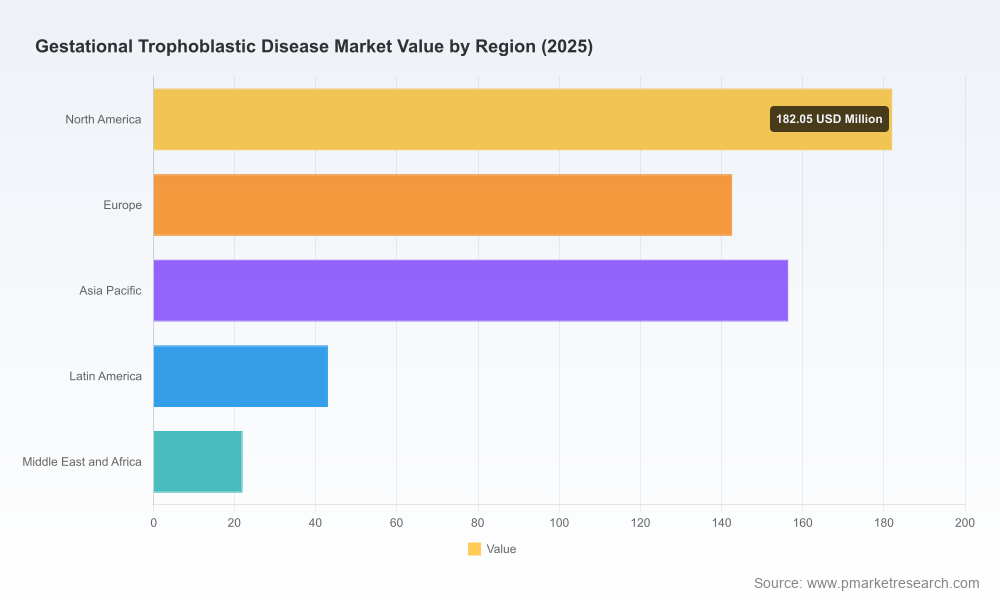

PW Consulting’s latest market intelligence on Gestational Trophoblastic Disease (GTD) synthesises clinical innovation, guideline evolution, and commercial dynamics to provide actionable direction for life‑sciences and health‑care leaders preparing decisions in 2026. Built on a 2020–2025 historical base and a detailed forecast through 2032, our model projects continued expansion of the GTD market from a 2025 base year into a multi‑hundred million USD opportunity by 2032, driven by steady demand for diagnostics and chemotherapy, and an accelerating layer of immunotherapy and repurposed modalities. The forecast period (2026–2032) reflects a compound annual growth rate (CAGR) of approximately 5.81%, highlighting a market that is both mature in core therapies and receptive to incremental innovation.

Gestational Trophoblastic Disease Market

Why this matters now

- Clinical practice is shifting. Recent international guidance and trial readouts are creating new treatment pathways that may reduce escalation to multi‑agent chemotherapy in selected patients, with consequences for product mix and payer negotiations.

- Innovation is converging on immuno‑oncology and repurposing. Checkpoint inhibitors and off‑label immunotherapies are moving from salvage use to earlier lines in protocol designs and national guidance in some systems.

- Market structure is mixed. The GTD market shows moderate concentration — incumbents with strong injectable and oral chemotherapy portfolios coexist with capable generic suppliers; this creates distinct entry vectors for novel agents, diagnostics, and service models.

- Operational resilience and access design are differentiators. Generic chemotherapy supply, reliable hCG monitoring pathways, and evidence generation for reimbursement will be decisive in 2026 commercial plans.

Market trajectory — a summary from our 2020–2032 model

Our top‑level market model captures a clear expansion from 2020 through 2025 and projects continued growth through 2032. The 2026–2032 forecast incorporates scenario sensitivity to guideline adoption rates, reimbursement decisions for immunotherapies in GTD, and the commercialisation timing of new modalities. While core chemotherapy and diagnostic services remain the revenue foundation, the marginal growth is increasingly attributable to immunotherapy uptake in difficult‑to‑treat and high‑risk cohorts, novel delivery and monitoring services, and selective adoption of repurposed agents as clinical evidence accumulates.

Gestational Trophoblastic Disease Market

From a competitive concentration perspective, the market is neither a pure commodity nor a winner‑takes‑all specialty market. Our concentration analysis shows that the top three players account for a meaningful share, and a five‑firm group controls a majority portion of the market, creating an environment where strategic partnerships, supply security, and targeted clinical evidence can materially alter positioning.

Gestational Trophoblastic Disease Market

Clinical and guideline inflection points: what changes the adoption curve

- Guideline evolution: The 2025 international consensus guidance introduced avelumab as an option in certain low‑risk GTN contexts to potentially avoid escalation to multi‑agent chemotherapy. Such endorsements reduce clinical friction for immuno‑oncology in GTD and create an evidence pathway for early‑line combination strategies.

- Practice‑changing trial evidence: Data presented in 2026 from the TROPHAMET analysis showed an improvement in complete response metrics and high rates of hCG normalisation when avelumab was combined with an 8‑day methotrexate schedule versus methotrexate alone in selected low‑risk patients. These results signal both therapeutic opportunity and commercial complexity — payers will require robust health‑economic justification to absorb higher acquisition costs.

- Checkpoint inhibitors and access: Pembrolizumab has been recommended by some national payers for chemo‑refractory high‑risk cases after multiple lines of therapy, reflecting a trend of checkpoint inhibitors moving into rarer oncology niches. Regulatory approval specifically for GTD remains limited, meaning off‑label use, compassionate access and local guideline adoption will determine near‑term market share for these agents.

- Emerging modalities: Research on focused ultrasound and drug repurposing (for example, statins in choriocarcinoma models) remains early but warrants monitoring — these avenues could create new referral patterns and adjunct service revenues if clinical programmes mature.

Competitive landscape — strategic profiles and implications

The competitive set spans global originators with oncology franchises, diversified suppliers of injectables, and large generic manufacturers. Each player type faces unique strategic choices:

- Large originators (example profiles include global pharmaceutical firms with established chemotherapy and immunotherapy portfolios): these firms are positioned to lead combination‑therapy studies, sponsor registrational or label‑expansion trials, and negotiate hospital and national payer contracts. Their challenge is demonstrating cost‑effectiveness versus established low‑cost chemotherapy backbones.

- Speciality oncology partners and alliances (notably alliances exploring immunotherapy combinations): collaborative trial networks and alliance structures can accelerate clinical acceptance but require careful IP and data‑sharing governance to protect market exclusivity in niche indications.

- Generic injectables and contract manufacturers: manufacturers of methotrexate, etoposide, dactinomycin and other backbone agents are critical to treatment continuity. Contract manufacturing scale, quality compliance, and supply‑chain redundancy underpin formulary decisions and hospital purchasing contracts.

- Diagnostic and monitoring providers: companies offering sensitive hCG assays, digital monitoring platforms, and point‑of‑care solutions will find opportunities to bundle diagnostic services with therapeutic pathways, improving adherence and generating real‑world evidence.

For executives assessing their relative position, the immediate questions are: Can you influence guideline adoption through credible trials or real‑world evidence? Do you control upstream supply (injectables) or downstream access (hospital channels and diagnostics)? How will alliances alter your route to the clinician?

Strategic actions for 2026 — a pragmatic checklist

- Prioritise combination and sequencing studies: For immunotherapy sponsors, plan pragmatic, guideline‑aligned trials that demonstrate not only efficacy but measurable reductions in escalation to multi‑agent chemotherapy and total cost of care.

- Design reimbursement evidence early: Engage HTA bodies and major national payers now to agree on endpoints (hCG normalisation, treatment duration, quality of life) and acceptable comparators. Build health‑economic models that reflect the long‑term survival and fertility preservation value propositions.

- Secure injectable supply and contract manufacturing: Generic chemotherapy remains essential; any supply disruption will shift treatment pathways and create windows for competitors. Invest in dual sourcing and quality certifications.

- Develop diagnostics and monitoring bundles: Integrating hCG monitoring services with therapeutic offerings both improves outcomes and creates recurring revenue streams — pursue partnerships with assay providers and digital health platforms.

- Explore non‑traditional innovations cautiously: Track early clinical programmes in focused ultrasound and repurposed agents. Consider small, hypothesis‑driven investments or collaborations rather than large early bets.

- Refine commercial segmentation and access playbooks: Regional differences in guideline uptake and reimbursement will persist; tailor market access strategies to payer archetypes rather than geography alone.

- Prepare M&A and alliance playbooks: Acquisitions of diagnostic capabilities, niche immuno‑oncology assets, or contract manufacturing capacity can accelerate market entry — define clear valuation frameworks for these plays in light of likely reimbursement scenarios.

What PW Consulting’s report delivers — practical content you can act on

The full PW Consulting GTD Market Report is built for executives who must translate clinical data into commercial decisions. Key deliverables include:

- Detailed market model (historical 2020–2025 and scenario‑based forecasts to 2032) with sensitivity toggles for guideline adoption, pricing, and access timing.

- Clinical pathway maps that translate trial outcomes and guideline changes into patient flows, treatment duration, and diagnostic touchpoints.

- Commercial playbooks for originators, generics, diagnostics providers and service innovators — including go‑to‑market templates, value‑dossier outlines, and payer engagement scripts.

- Competitive dossiers on incumbent and emerging players, covering portfolio fit, trial positions, manufacturing footprint, and likely strategic moves.

- Reimbursement and HTA impact assessments across major payer archetypes, with recommended evidence generation plans and pricing levers.

- Supply‑chain risk matrix and procurement strategies to safeguard injectable availability and negotiate hospital formularies.

- Custom advisory options — from focused due diligence to full commercial launch support and payer negotiation assistance.

In keeping with our “trailer” approach, the public summary above highlights the strategic implications and headline forecasts that will matter in 2026. The report contains granular segmentation tables, regional and therapy‑level splits, and proprietary scenario outputs that we do not publish in this press release. These detailed datasets and the underlying assumptions are available through PW Consulting’s report subscription or bespoke advisory engagements.

Concluding recommendation

GTD is a specialised but strategically significant market where incremental clinical gains can disrupt long‑established treatment algorithms and payer arrangements. For 2026, the decisive differentiators will be the ability to translate mechanistic innovation (immuno‑oncology and repurposed agents) into defensible clinical and economic value, while ensuring uninterrupted access to chemotherapy backbones and reliable diagnostic monitoring. Organisations that align clinical programmes, manufacturing security, and payer evidence generation in a coherent, time‑bound plan will secure disproportionate advantage in the coming five years.

PW Consulting is prepared to partner with executive teams to convert these insights into operational plans. For full access to the dataset, segmentation outputs, and bespoke scenario analyses, contact our GTD market team through the PW Consulting website.

For detailed analysis of this topic, please visit the official page:Gestational Trophoblastic Disease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com