What Is Fueling Growth in the Unmanned Marine Vehicles Market?

Networking |

2026-04-06 07:16:31

PW Consulting’s latest market study on the Ultra White Rolled Solar Glass industry delivers a focused, operational playbook for executives planning capital allocation, manufacturing strategy, and procurement choices in 2026. Our analysis documents a multi-year expansion of the total market—from roughly USD 8.4 billion in 2020 to USD 16.4 billion in 2025—and models a continuation of strong growth across the forecast window 2026–2032, with a compound annual growth rate of 12.84% and an end‑period market approaching USD 38.2 billion. This release is designed as a strategic “trailer”: it demonstrates the empirical depth and practical frameworks that informed our conclusions while reserving the granular segment tables and plant-level economics for the full report.

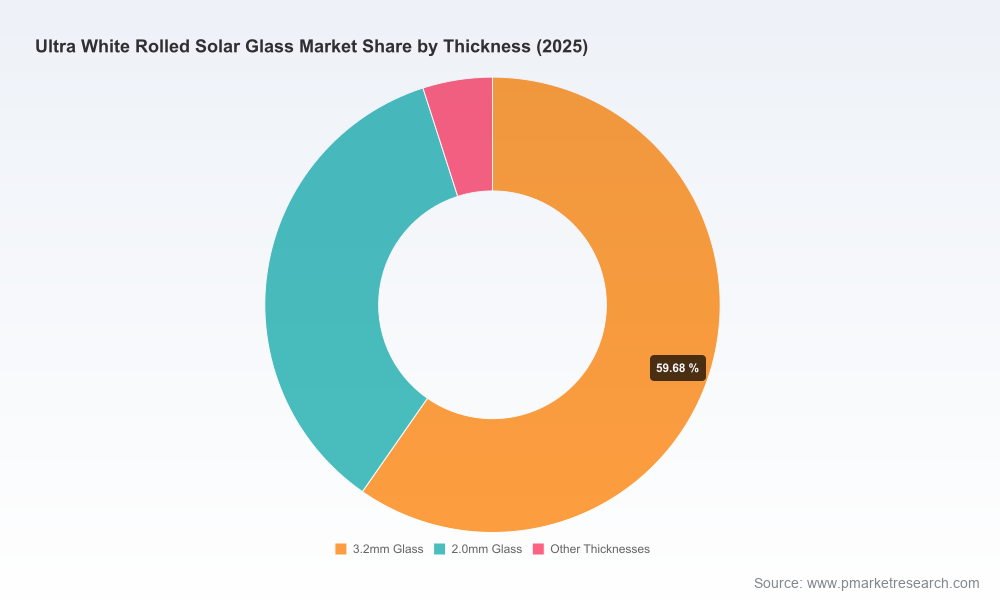

Ultra White Rolled Solar Glass Market

Timing and scale. The industry is in a second phase of structural expansion driven by accelerating solar deployments, evolving module architectures (including higher transparency and bifacial designs), and policy-driven reshoring incentives. The market size milestones observed through 2025 and our 2026–2032 CAGR projection create a narrow window in 2026 to secure advantaged positions in raw material sourcing, production capacity, and technology partnerships.

Ultra White Rolled Solar Glass Market

Capital allocation. Project returns in glass production are highly sensitive to timing. Our financial models quantify how a 12–18 month shift in commissioning can materially affect IRR under current pricing and feedstock scenarios—making 2026 a decisive year for go/no‑go decisions.

Ultra White Rolled Solar Glass Market

Risk consolidation. Supply chain stresses—particularly around ultra‑low‑iron silica sand, energy inputs, and logistics—mean that strategies based on simple capacity growth are insufficient. The report lays out mitigations that preserve margin and delivery reliability.

Where to locate new capacity to maximize access to feedstock and incentive regimes while minimizing delivery lead times to module manufacturers?

Which technology pathways (rolled/cold‑calendered vs float-based tempered glass, anti‑reflective coatings, embossing patterns) create the most durable product premiums?

How should buyers hedge feedstock exposure to ultra‑low‑iron silica sand as raw‑material markets tighten?

What are the realistic timeframes and capex profiles for ramping 150–1,200+ tons/day furnaces, and what breakpoint economics justify greenfield vs brownfield expansion?

Supply–demand model and scenario suite: granular demand pathways by product architecture and a sensitivity framework that quantifies the impact of module technology adoption, tariff scenarios, and incentive shifts on revenue curves through 2032.

Plant-level economics: capex/opex benchmarking, heat‑and‑power integrations, melt‑line throughput assumptions, and commissioning timetables built from primary plant surveys and operator interviews.

Raw material chain analysis: mapped sources of ultra‑low‑iron silica sand, concentration points, pricing dynamics, and a 10‑year procurement playbook driven by market liquidity and contestable supply.

Policy & incentive impact model: quantified overlays for tax credits, grant programs, and content requirements that affect domestic sourcing decisions (including a focused assessment of recent US policy changes and allocation decisions).

Competitive and consolidation playbook: CR3/CR5 concentration analysis, relative cost curves, M&A targets, and JV structuring templates for rapid capacity access.

Commercial go‑to‑market tools: customer segmentation, pricing capture strategies for AR‑coated and patterned lites, and recommended long‑term offtake contract structures.

The industry exhibits meaningful concentration at the top, with the three largest suppliers accounting for a majority share and the top five suppliers commanding a substantial portion of market supply. This structure shapes competitive dynamics: large incumbents with vertical integration and global production footprints remain the price leaders, while agile regional players exploit local incentives and faster time‑to‑market.

Xinyi Solar Holdings Limited — A global leader with large-scale calendered production, Xinyi’s technology and scale advantages (including multi‑tens of thousands of tonnes daily melting capacity at mid‑2025 levels) make it a structural supplier to major module manufacturers. Recent commissioning of advanced lines in strategic SEZs underlines its dual strategy: expand throughput while shortening logistics to regional module hubs.

Ancai Hi‑Tech (ACHT) & IRICO Group — These established Chinese producers bring decades of process know‑how in rolled ultra‑clear glass and patterned embossing. Their product portfolios emphasize versatile thickness ranges and modular furnace architectures that can be matched to customer specifications.

Şişecam Group & AGC Inc. — Regional champions in Turkey and Japan respectively, these companies combine patterned/templated offerings and premium float technology. AGC’s extra‑clear glass positions it for higher‑efficiency module manufacturers that prize purity and coating compatibility.

Stewart Glass LLC & Vitro Architectural Glass — These US entrants illustrate the onshoring dynamic. Stewart’s new Ohio facility is notable as the first fully operational US plant producing 3.2‑mm rolled low‑iron glass at commercial tempo, while Vitro’s Texas expansion (supported by a significant IRS investment tax credit) signals robust domestic demand and downstream verticalization.

Other regional players — Several Chinese producers and specialist manufacturers in Qingdao and Jiaxing continue to supply high‑quality lites and surface treatments, supplying both domestic and export markets with competitive lead times.

Facility activations and expansions in 2025–2026 have reshaped supply dynamics—examples include a newly ignited furnace in an Indonesian SEZ and start‑up of strategic US production lines—altering near‑term availability and logistics cost curves.

Policy moves in the US (including allocation of significant investment tax credits and targeted loan guarantees) have materially improved the economics of domestic manufacturing and changed sourcing calculus for US module makers and glass suppliers.

Raw material market signals—most notably the ultra‑low‑iron silica sand market sizing and anticipated doubling over the next decade—necessitate an immediate procurement response from both producers and converters.

Two system‑level risks dominate the next 18–36 months. First, the ultra‑low‑iron silica sand supply chain is tightening: market value estimates and capacity forecasts indicate a rapidly scaling sector that will experience price discovery as new demand competes with legacy industrial users. Second, regulatory shifts are re‑rating domestic manufacturing economics through targeted credits and content rules. Notably, recent legislation has introduced new restrictions and phase‑out timelines for certain tax incentives that will affect project economics—our models quantify how those rule changes alter break‑even timelines for greenfield projects.

Defer or accelerate capacity based on access to long‑term feedstock: secure multi‑year direct silica sand contracts or equity stakes in supply to protect margins.

Prioritize modular furnace strategies that permit staged ramping; avoid single large‑capacity bets unless paired with offtake commitments from tier‑1 module customers.

Leverage policy arbitrage: evaluate investment tax credits and loan guarantee programs as part of project IRR rather than one‑off benefits; structure financing to capture available incentives while minimizing counterparty exposure.

Adopt a differentiated product strategy: reserve premium capacity for AR‑coated and patterned lites while using higher‑throughput lines for standard ultra‑clear products.

Use M&A selectively to gain rapid access to capabilities—targeted acquisitions of patterned glass lines or regional converters can shorten time to revenue materially versus greenfield builds.

This article presents the strategic contours and evidentiary signals we believe will shape 2026 decisions in the ultra white rolled solar glass market. It highlights the growth trajectory, concentration dynamics, material supply risks, and the competitive plays that matter. For teams executing capital projects, procurement agreements, or merger strategies, the full PW Consulting report provides the missing detailed tables, manufacturer‑level capacities, plant economics, regional demand matrices, and ready‑to‑use financial models that translate our qualitative conclusions into executable project plans.

To access the full intelligence suite—complete with downloadable Excel models, primary interview transcripts, and the full segmentation dataset—visit our report landing page or contact PW Consulting’s Solar Materials Practice. The window to lock in advantaged positions is narrow; 2026 will separate strategic winners from reactive followers.

— PW Consulting, Advanced Strategy & Industry Analysis

For detailed analysis of this topic, please visit the official page:Ultra White Rolled Solar Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com