How a Crypto Marketing Agency Delivers Measurable Results for Web3 Brands?

Other |

2026-04-10 11:15:49

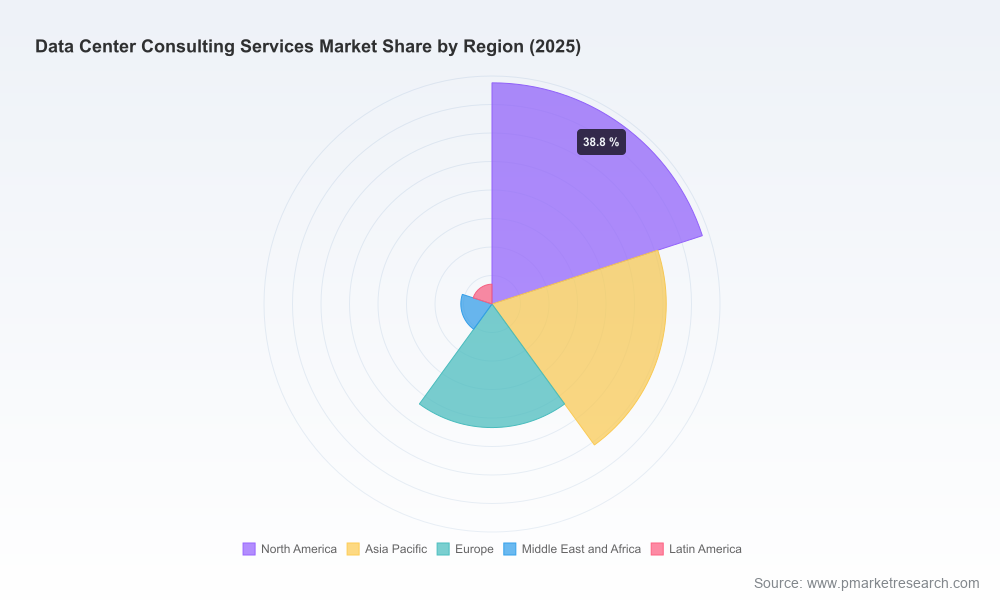

As enterprises finalize capital allocations and operational strategies for 2026, the data center consulting services market stands out as one of the most consequential and fastest-growing service domains across the infrastructure stack. Our latest PW Consulting market study shows the sector expanding at a robust compound annual growth rate (CAGR) of 13.45%, with global market value moving from a mid‑double‑digit billion base in 2025 to a projected market size that more than doubles by the end of the forecast window. This growth reflects simultaneous, structural forces: surging compute demand driven by AI and cloud workloads, heightened regulatory and sustainability obligations, and an evolution in how organizations source lifecycle consulting—from greenfield site selection to ongoing operations optimization.

Data Center Consulting Services Market

Decision clarity under uncertainty: The market’s strong growth masks important qualitative shifts—buyer expectations have moved from tactical engineering support to integrated, outcomes-oriented advisory that ties data center investments directly to business KPIs such as time‑to‑market, carbon reduction, and risk exposure. Our report distills where advisory dollars should be allocated to maximize these outcomes.

Data Center Consulting Services Market

Capital and operating trade-offs: With significant capex being deployed into new capacity and existing campus upgrades, boards demand transparent frameworks to compare scenarios (e.g., modular builds vs. large-scale campus, on-premises vs. colocation hybrid models). The study provides practicable decision frameworks to evaluate these trade-offs.

Data Center Consulting Services Market

Vendor selection as a strategic lever: Consulting partners are no longer interchangeable. Our analysis equips procurement and technical leaders to map consulting capabilities to specific program phases—planning, design, construction, migration, and operations—so vendor selection becomes a performance differentiator, not just a cost exercise.

The market’s current momentum—captured by a 13.45% CAGR—translates into a material uplift in advisory demand across the lifecycle. From a pragmatic standpoint, this creates three immediate implications for 2026 strategy:

Scale and specialization coexist. While the overall market is growing rapidly, competitive concentration remains modest, underscoring opportunities for both large multidisciplinary consultancies and niche engineering houses to win work. This fragmentation means buyers can drive favorable engagement models but must be disciplined in how they assess delivery risk.

Project complexity is increasing. Capital projects are integrating sustainability, biodiversity, local labor strategies, and more sophisticated resilience measures—each adding program risk and execution complexity that requires advisory teams with cross‑domain capabilities.

Timing and sequencing matter. As new regulatory requirements and privacy rules take effect in 2026, organizations that front-load compliance and cyber‑risk design work into early planning phases materially reduce downstream remediation costs and project delays.

We designed the report to be an operational manual for C‑suite and delivery teams—not just a descriptive market narrative. Highlights include:

Decision frameworks and stage‑gated playbooks: Actionable templates for site selection, build vs. buy economic modeling, and migration roadmaps tuned for high‑availability and AI workloads.

TCO and scenario models: Parametric calculators that translate design choices (power density, cooling architecture, redundancy levels) into multi‑year capex/opex profiles and risk-adjusted ROI estimates.

Procurement and contracting guidance: Standardized RFP/RFI language, scoring rubrics for consulting partners, and contract clauses to align incentives across capital project delivery and long‑term operations.

Regulatory and compliance playbook: Practical checklists for anticipating emissions, generator, and privacy-related obligations that surfaced in 2025–2026 legislative cycles, with suggested mitigation steps to harden program timelines.

Sustainability & ESG integration: Measurement frameworks for embodied carbon, operational emissions, and biodiversity considerations—translated into procurement KPIs and capex prioritization recommendations.

Vendor evaluation toolkit: A repeatable methodology for scoring consulting firms across capability clusters (design & engineering, strategy, migration support, operations) and delivery modalities (in‑house vs. outsourced managed services).

Executive briefing decks and stakeholder templates: Ready‑to‑use materials for board updates, financial committees, and local permitting authorities to accelerate approvals and secure funding windows.

Our competitive analysis synthesizes capability mapping, recent strategic moves, and likely trajectories for incumbent consultancies and engineering firms. Key takeaways for 2026:

Global engineering and program management firms (examples include established names known for site selection, design, and project delivery) remain indispensable for mission‑critical, high‑complexity projects. Their strengths lie in integrated project controls, site engineering, and large‑scale construction management.

Professional services and IT consultancies (firms recognized for strategic advisory, cloud migration, and digital transformation) are rapidly expanding their data center advisory footprint. Strategic acquisitions and capability builds—particularly in capital project delivery tools and AI‑driven optimization—are enabling them to propose end‑to‑end modernization programs that couple infrastructure with enterprise IT roadmaps.

Specialist engineering consultancies and sustainability‑focused firms are winning work where environmental integration, ESG due diligence, and local permitting complexity dominate requirements. Partnerships between developers and these specialists are increasingly common for greenfield campus programs.

Market moves to watch: Recent industry activity demonstrates playbooks firms are adopting. Strategic acquisitions that enhance capital project delivery capabilities, partnerships to integrate biodiversity and sustainability into campus design, and market outlooks from real estate advisors projecting large capacity additions all signal how advisory demand will polarize by capability.

For procurement teams, the practical implication is to build multi‑vendor delivery models that combine global program management, localized engineering, and digital operations capabilities—contracted with clear performance metrics and escalation paths.

The operating environment in 2026 is materially different from five years prior. Notable dynamics that informed our risk and opportunity frameworks include:

Labor and skills constraints: Large employers and hyperscalers are funding substantial training programs to grow the skilled labor pool for electrical and data center trades. These initiatives reduce long‑term labor premium risk but require early engagement in workforce planning to secure qualified crews for early project phases.

Emissions and generator standards: New emissions rules in certain jurisdictions are changing equipment selection and backup power strategies. Projects must now assess local generator compliance early in design to avoid mid‑cycle redesigns and budget overruns.

Privacy and cyber compliance: Fresh federal and state‑level privacy regimes and rules on sensitive data transfers are elevating cyber and data governance requirements for facility contracts and operational playbooks. Advisory teams should fold privacy impact assessments into vendor evaluations and operations handover processes.

Start with outcome‑based requirements: Translate business outcomes (e.g., latency targets for AI workloads, sustainability commitments, or disaster recovery RTOs) into technical and contractual specifications before engaging vendors.

Adopt modular procurement: Use a phased procurement approach that separates early‑stage advisory (strategy and site selection) from detailed design and construction, enabling competitive tension and better value capture.

Mandate integrated sustainability KPIs: Tie a portion of consulting fees and contractor payouts to measurable energy and biodiversity outcomes to align incentives across the delivery chain.

Lock in compliance pathways early: Use our regulatory checklists and compliance gating to avoid last‑minute scope creep driven by evolving emissions and privacy rules.

Invest in capability uplift: Where in‑house teams are strategic, prioritize skills development in program controls, digital twins, and cyber‑operational convergence to reduce long‑term reliance on external advisors.

The PW Consulting Data Center Consulting Services Market report is structured to support three core use cases: immediate procurement and RFP design; mid‑cycle program governance and risk mitigation; and long‑term capability planning tied to corporate sustainability and digital transformation goals. It includes models, templates, and a vendor evaluation toolkit designed to be operational on day one of a planning cycle.

We intentionally refrain from publishing every granular split and vendor score in this press release. The full report contains the detailed datasets, regional and service‑type splits, vendor rankings, and downloadable economic models you will need to accelerate decision‑making in 2026.

For boards, CIOs, real estate directors, and program managers preparing budgets and vendor strategies for 2026, this study is a tactical asset. Visit our official report page to access the full dataset, interactive scenario models, and our vendor scoring matrix—tools that will help you convert market momentum into measurable business outcomes.

For detailed analysis of this topic, please visit the official page:Data Center Consulting Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com