Copper Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-17 10:42:47

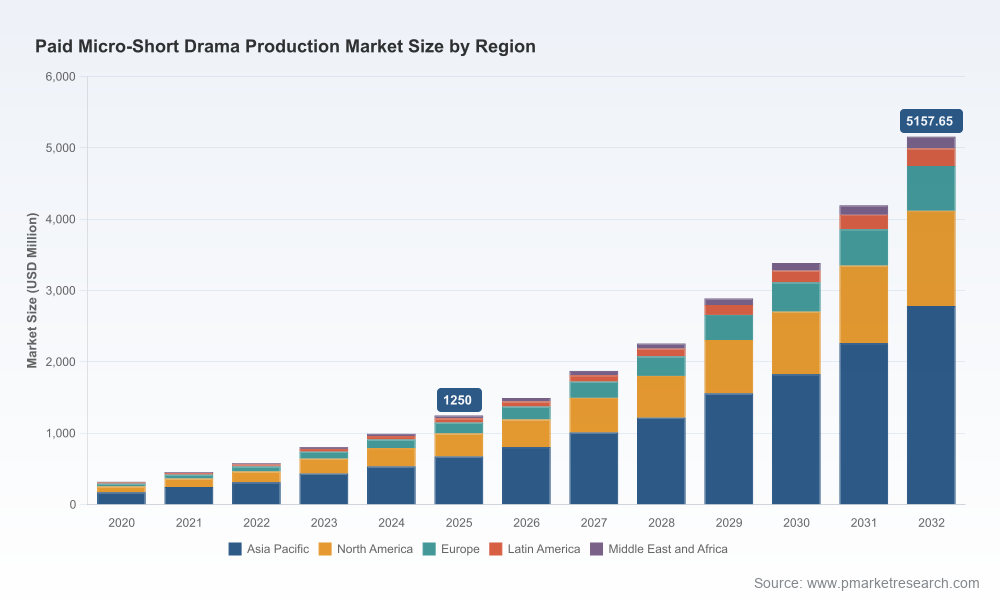

PW Consulting’s latest market study — base year 2025, historical coverage 2020–2025 and a forecast horizon through 2026–2032 — frames paid micro short drama as one of the fastest-growing creative segments globally. Our macro model shows a compound annual growth rate of 22.45% across the forecast window. Measured against the 2020 baseline, the market expanded rapidly into a billion-dollar-plus category by 2025 and, under our central scenario, continues toward multi‑billion scale by the early 2030s.

Paid Micro Short Drama Production Market

This release is written as a practical briefing for boards, corporate strategy teams, investors, platform operators and studio executives preparing 2026 budgets and strategic roadmaps. It surfaces the growth drivers, unit economics inflection points, competitive playbooks and regulatory dynamics that will determine who captures disproportionate value as the segment professionalizes and consolidates.

Paid Micro Short Drama Production Market

Investment prioritization: Capital allocation choices in 2026 will be binary for many companies — either invest to scale production and platform capabilities now or face steeper costs to catch up when consumer willingness to pay matures further. Our modelling translates market growth into actionable sizing buckets for greenfield entry, measured expansion and consolidation strategies.

Paid Micro Short Drama Production Market

Production economics and technology adoption: Short-form paid dramas are moving from artisanal shoots to industrialized pipelines. We quantify the tipping points at which AI-assisted production, compact crews and vertical-first workflows materially compress per-episode costs and shorten time-to-market — and show how those savings alter breakeven thresholds for different monetization mixes.

Distribution & monetization design: The market is being monetized through a mix of micropayments, subscriptions and platform bundles. Our frameworks help product and commercial teams test optimal bundles and revenue-share structures and align content investment with lifetime value (LTV) thresholds for target cohorts.

Talent, legal and regulatory planning: New guild agreements for microdramatic productions and AI-labelling regimes in major markets have immediate implications for casting, IP clearances and budget allocations. Our playbooks map talent contracting options against expected per-title economics and compliance requirements.

Proprietary market sizing and scenario analysis: methodology, model sensitivities and three demand scenarios (central, upside, downside) covering 2026–2032 so executives can stress-test strategic choices against macro and product-level shocks.

Unit-economics templates: per-episode cost stacks, post-production and localization overlays, LTV/CAC benchmarks and a set of standardized KPIs to be embedded in PMOs and investment committees.

Production playbooks: end-to-end blueprints for vertical video shoots (pre-production, 1–2 week shoot cycles, compact crew compositions), AI-assisted tooling integration and a gated checklist for transitioning from live-action to hybrid/AI workflows while preserving brand and regulatory integrity.

Distribution & monetization playbooks: coin-based unlocks, episodic subscription mixes, app‑bundle partnerships and social-engineered funnel designs, accompanied by A/B test matrices and recommended cohort targets.

Talent & legal operating model: contract templates and negotiation levers reflecting new media guild clauses, talent incentives calibrated for sub-$300k productions, and IP licensing playbooks for original vs. adapted content.

M&A and partnership scorecards: acquisition target archetypes, valuation heuristics for bolt-on studios or tech stacks, and a five-step diligence checklist focused on content library utility, retention KPIs and localization readiness.

Regulatory & risk heatmaps: country-level overlays highlighting content review mechanisms, AI disclosure requirements and likely policy trajectories that materially affect distribution strategies.

The competitive map today mixes specialized platform-studios, export-oriented producers, and vertically integrated media groups. Market concentration metrics indicate moderate leader dominance: the top three firms account for a meaningful share of industry revenue, and the top five approach half of the market, signaling both opportunity for niche entrants and an accelerating M&A runway for scale players.

Crazy Maple Studio (ReelShort) — a California-headquartered studio operating the ReelShort app — exemplifies the platform-studio hybrid. Its vertical, episodic model and coin-based episodic unlocks show how platform design can maximize per-engaged-user monetization across international markets. Strategic takeaway: invest in UX funnels that convert high-frequency micro-engagers into stable subscribers.

Beijing Dianzhong Technology (DramaBox) — operating a sizable paid micro-drama platform with strong overseas traction — highlights localization as a core competitive moat. Its success underscores the commercial value of translated and culturally adapted vertical series. Strategic takeaway: prioritize localization engineering and regional editorial pipelines when targeting cross-border markets.

Linmon Media and AR Asia Productions have demonstrated that slates and telco/platform partnerships materially accelerate distribution reach in Asian markets. Their approaches offer a playbook for local-first content strategies that can be scaled via white-label platform deals.

Vigloo (SpoonLabs) from Seoul has pushed the frontier on AI-native productions, releasing fully AI-produced titles in compressed production cycles. This validates a low-cost, high-velocity content thesis for English-speaking and global markets. Strategic takeaway: test AI-assisted pilots to shortcut time-to-market while instituting quality and compliance controls.

Holywater demonstrates that Hollywood‑grade production values can be repurposed for vertical paid formats — a reminder that premium narratives still command price premiums when matched to platform economics.

Recent industry moves — slate launches, fully AI-produced titles and rapid scale-ups of AI-assisted production hubs — confirm three immediate dynamics: (1) supply-side scaling through tech and hubs; (2) product experimentation across monetization architectures; and (3) regulatory formalization around AI and talent protections. Companies that synchronize editorial, production and legal ops will capture disproportionate upside as the market consolidates.

AI disclosure and content-review regimes: Several major markets now require labeling of AI-generated content and have strengthened content-review tiers. Compliance costs are non-trivial and must be factored into go-to-market timelines and platform moderation stacks.

Guild negotiations and labor protections: New media agreements for microdramatic productions influence per-episode payroll budgeting and residuals. Producers must build flexible contracting vehicles to work with union talent while preserving unit economics.

Cross-border distribution frictions: Data localization, licensing windows and censorship regimes create operational complexity for export-led strategies. Our mitigation playbook shows how to structure geo‑segmented legal wrappers and distribution joint ventures to limit exposure.

Prioritize platform partnerships that guarantee user acquisition economics. Short-term promotional deals with telcos and social platforms can shorten payback periods for paid titles.

Invest selectively in AI tooling and production hubs: a modest, staged investment in production automation yields large marginal returns on episode throughput, but must be paired with creative controls and disclosure workflows.

Look for bolt-on acquisitions that close distribution or localization gaps. Targets should be scored on retention metrics, localization capability and integration ease rather than purely on content library size.

Design experimental budgets for hybrid monetization tests (episodic micropayments + bundled subscriptions) and bake the learnings into 2027 content slates.

Think of this study as both a strategic map and an operational toolkit. The full report includes downloadable financial models, playbook checklists, a competitor scorecard and a deal‑sourcing matrix that let you model investment outcomes under alternative growth and policy scenarios. To preserve the report’s role as a decisioning platform, we intentionally summarized high-level findings here and withheld granular subsegment revenue breakdowns and localized opportunity matrices. Those discrete data tables and market splits are available in the full deliverable and are designed to be embedded into your investment committee pack or M&A diligence workflow.

Immediate recommended next steps for 2026:

Run a 90‑day pilot: pair a content studio with an AI‑assisted production hub and one distribution partner to validate unit economics against the report’s LTV/CAC thresholds.

Execute a talent‑contracting audit: align upcoming slates with guild clauses and set aside contingency for incremental residuals or disclosure compliance.

Establish an acquisition watchlist: prioritize targets that close either localization capability gaps or platform distribution reach, and apply the report’s valuation heuristics.

PW Consulting’s Paid Micro Short Drama Production Market report is designed to be operational: downloadable financial models, granular subsegment tables, country-level opportunity matrices, and the competitor database are all included in the full package. We deliberately omitted detailed subsegment figures in this briefing to encourage strategic usage of the full data set within governance and investment processes. For access to the complete report and consulting engagement options, visit our report page or contact the PW Consulting engagement team.

In a market growing at an annualized rate north of 20%, the 2026 execution window will determine who builds enduring franchises and who becomes an acquisition target. This report equips you to make those calls with confidence.

For detailed analysis of this topic, please visit the official page:Paid Micro Short Drama Production Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com